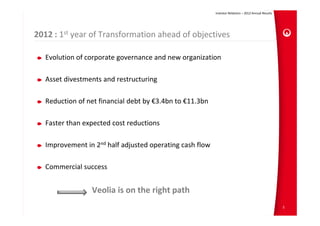

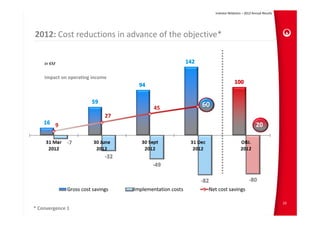

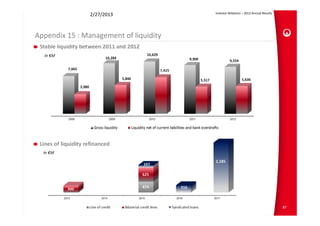

1. Veolia achieved its objectives for the first year of its transformation plan ahead of schedule, with debt reduction of €3.4 billion and cost reductions exceeding targets.

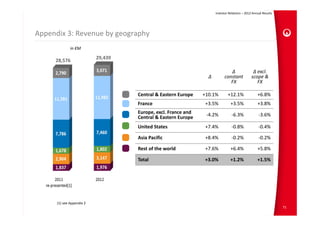

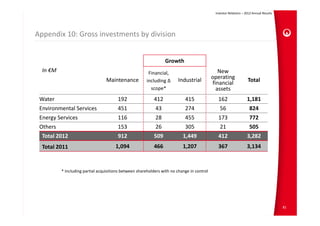

2. The company divested €3.7 billion in assets, reducing net financial debt and focusing geographically and by business.

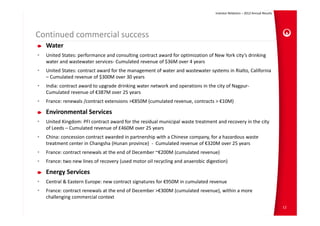

3. Veolia continued to win major contracts globally in water, waste, and energy services totaling billions in revenues over several decades.