Download to read offline

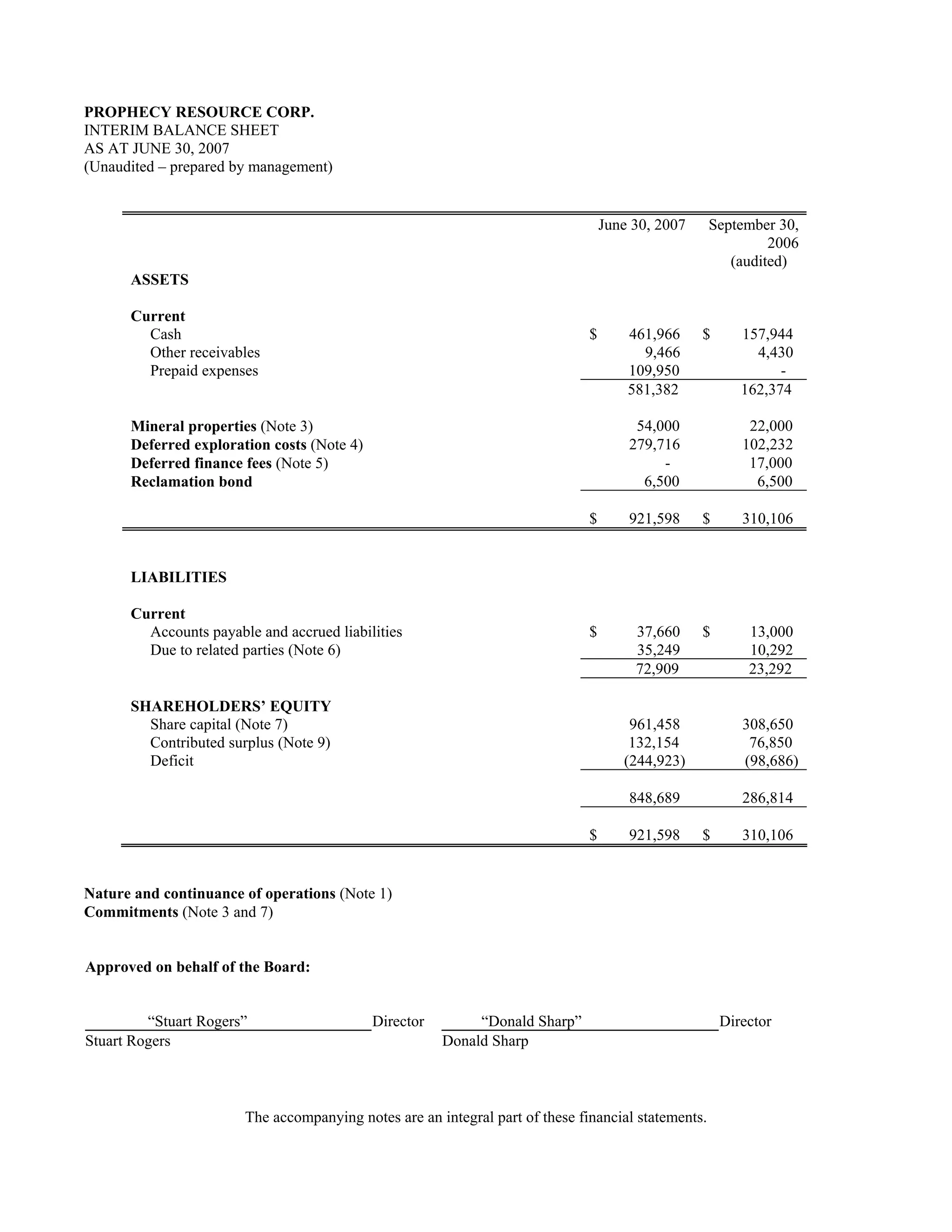

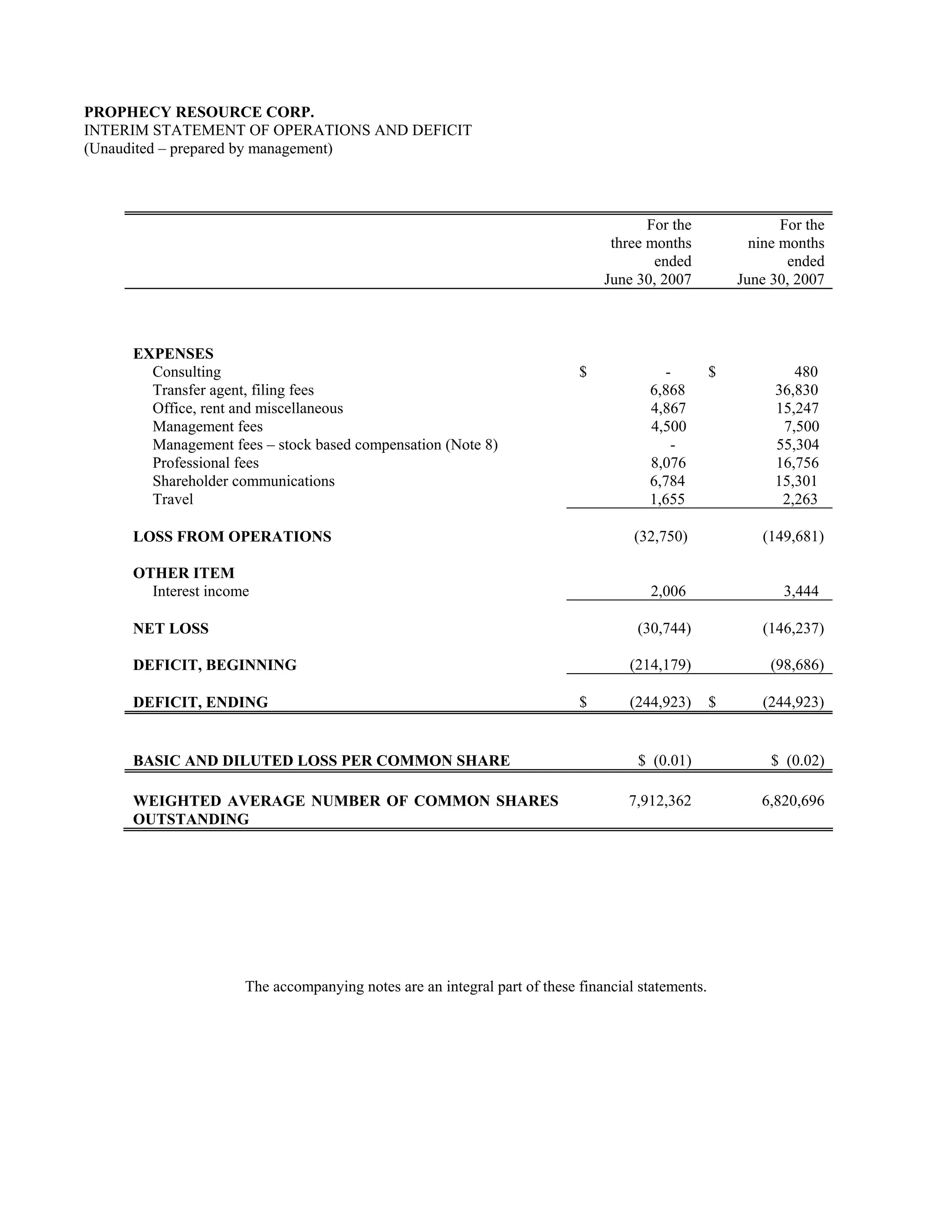

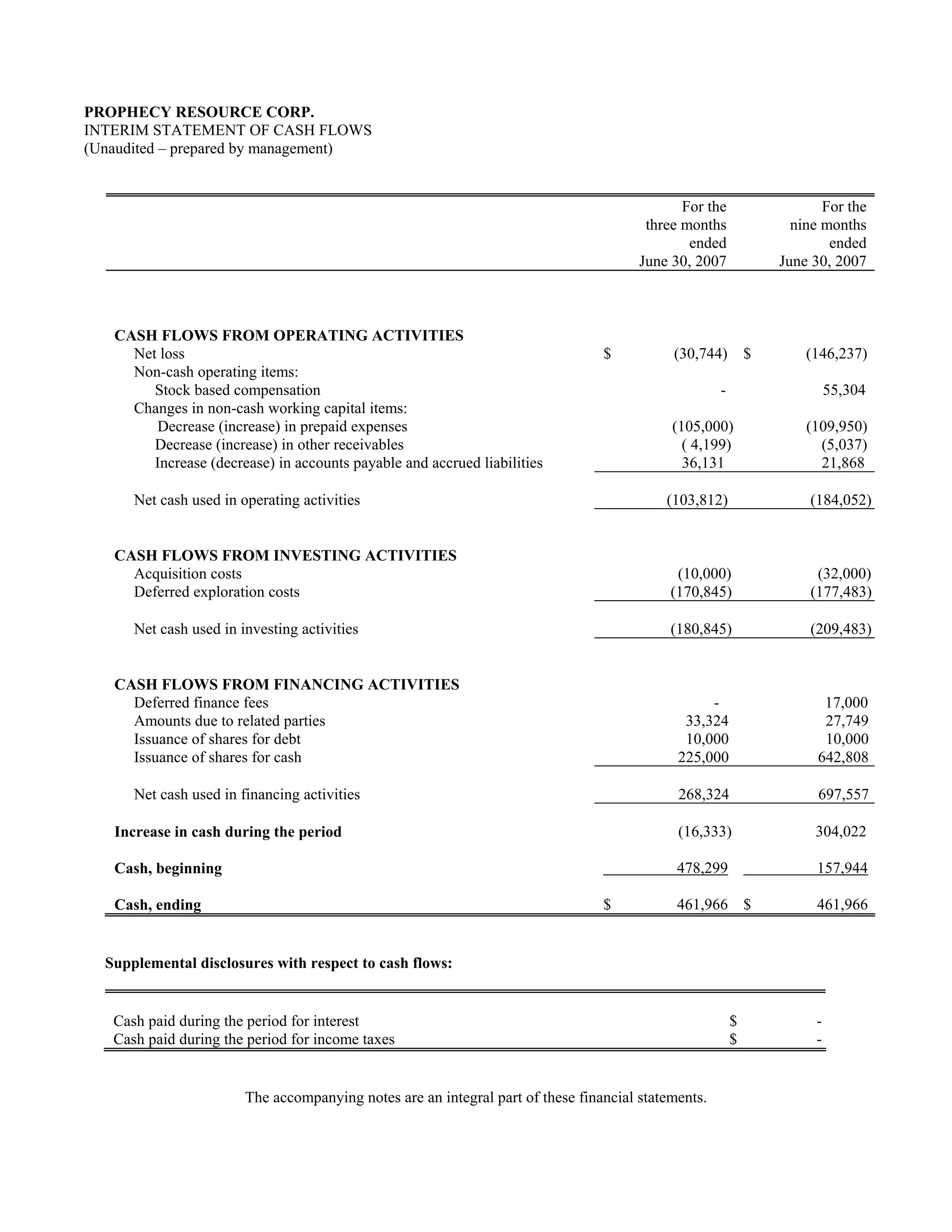

Prophecy Resource Corp. released unaudited interim financial statements for the period ended June 30, 2007. The statements included a balance sheet showing assets of $921,598 including cash of $461,966, mineral properties of $54,000, and deferred exploration costs of $279,716. The statements also showed a net loss of $30,744 for the quarter and $146,237 for the nine months ended June 30, 2007. Cash flow statements showed $103,812 used in operating activities for the quarter and $184,052 for the nine months.