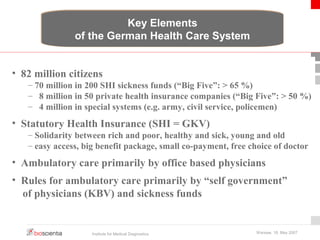

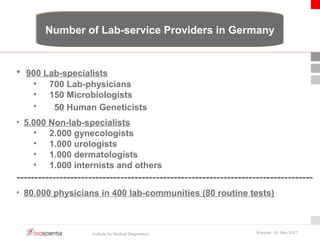

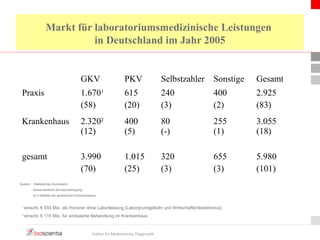

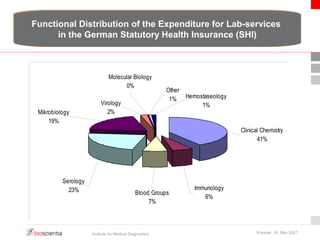

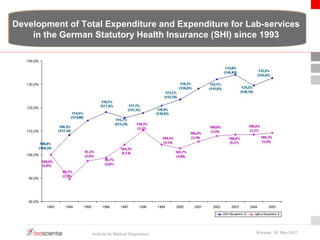

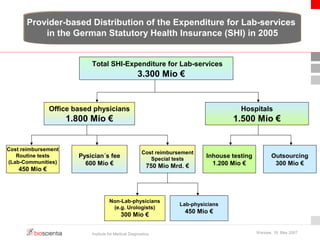

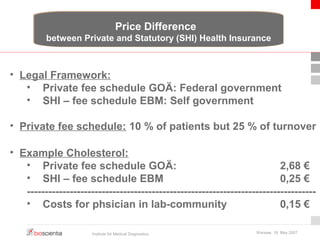

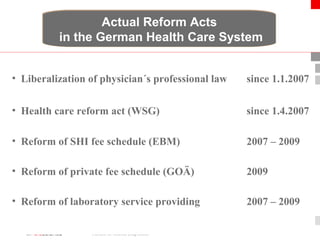

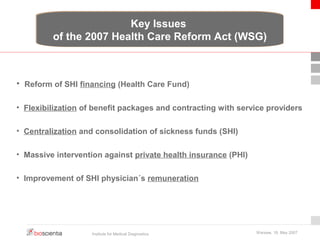

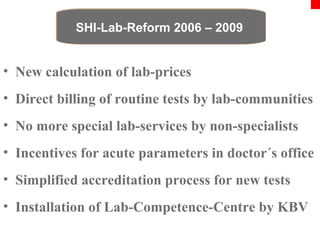

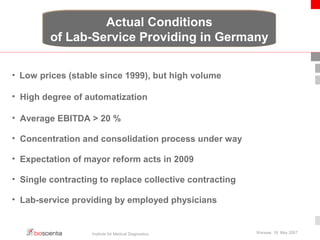

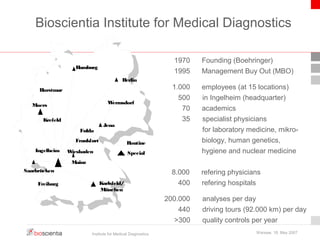

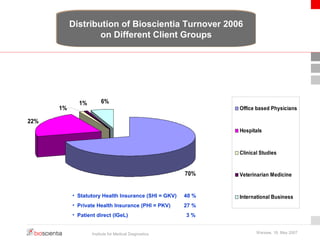

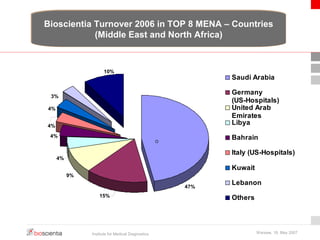

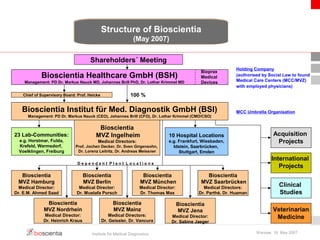

The document outlines the structure and financial landscape of laboratory diagnostics within the German health care system, which serves approximately 82 million citizens and includes multiple insurance types. It details the distribution of lab service providers, expenditure on laboratory services, and recent reforms aimed at improving the efficiency and management of healthcare delivery. Key players in the laboratory market and their financial performance are also highlighted, indicating trends in consolidation and strategic options for the future.

![CTEV [ clubfoot] DR ARUN LAL ,DR MOHAMED ASHRAF travancore medical college k...](https://cdn.slidesharecdn.com/ss_thumbnails/ctevclubfootdrarunlaldrmohamedashraftravancoremedicalcollegekollamkeralaindia-260208063247-18fc466c-thumbnail.jpg?width=640&height=640&fit=bounds)