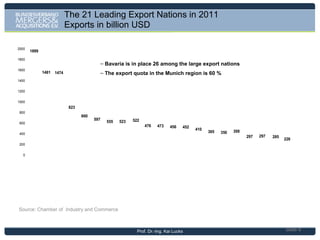

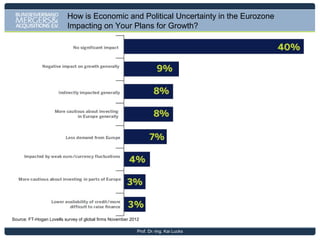

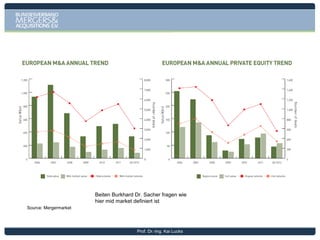

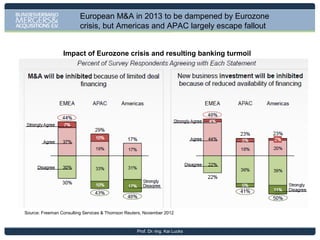

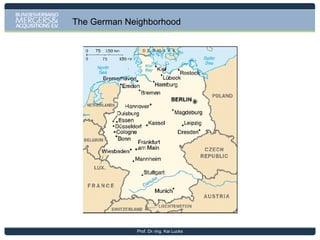

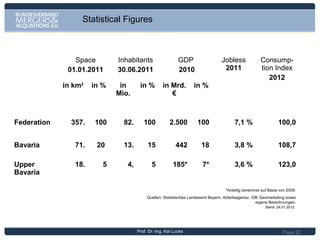

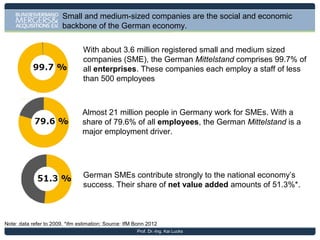

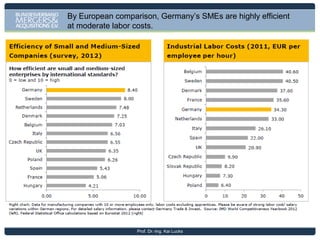

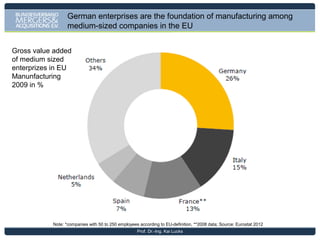

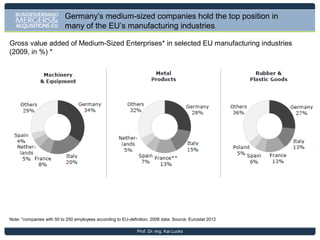

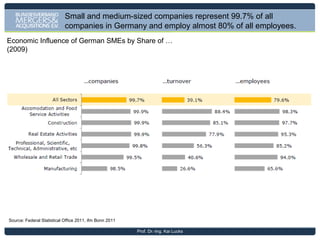

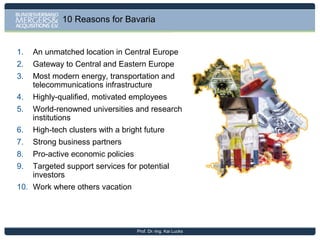

The document outlines the economic significance of German small and medium-sized enterprises (SMEs), particularly the 'Mittelstand', which constitutes 99.7% of all companies in Germany and employs nearly 80% of the workforce. It discusses Bavaria's strategic advantages for investment and trade, including a strong infrastructure and significant GDP contributions. Additionally, it highlights the impact of external economic factors, including the eurozone crisis, on mergers and acquisitions within the region.

![Germany[1]](https://cdn.slidesharecdn.com/ss_thumbnails/germany1-101205161233-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)