Downloaded 31 times

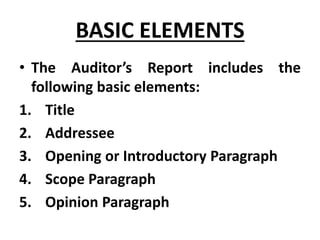

The document outlines the key elements that must be included in an auditor's report according to the Companies Ordinance 1984. It discusses the required sections of the report including the title, addressee, opening paragraph, scope paragraph, opinion paragraph, date of report, auditor's address and signature. It also describes the types of opinions that can be issued - unqualified, qualified, disclaimer of opinion, and adverse opinion - and the circumstances under which each would be appropriate.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)