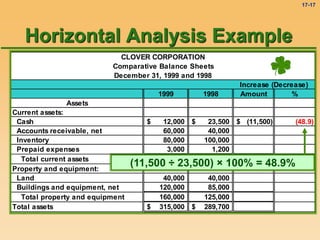

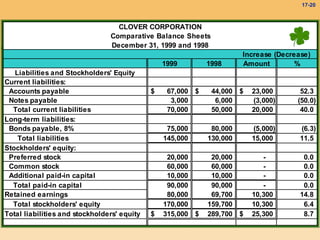

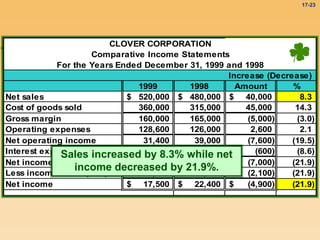

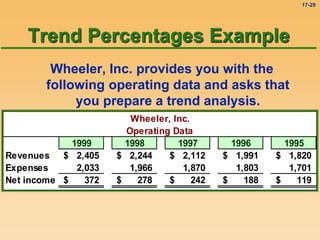

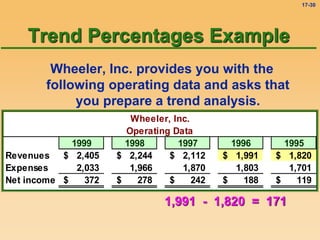

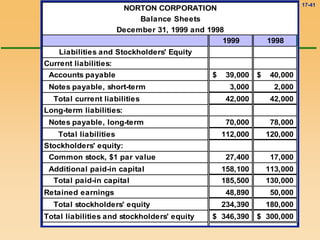

The document discusses various methods for analyzing financial statements, including horizontal analysis, vertical analysis, common-size statements, trend percentages, and ratio analysis. It provides examples of each method. For horizontal analysis, it shows an example of analyzing changes in dollar amounts and percentages for items on a company's balance sheet between two years. For vertical analysis, it demonstrates expressing each item on the balance sheet as a percentage of total assets. For trend percentages, it shows calculating growth rates for a company's revenues, expenses, and net income over five years.