Download to read offline

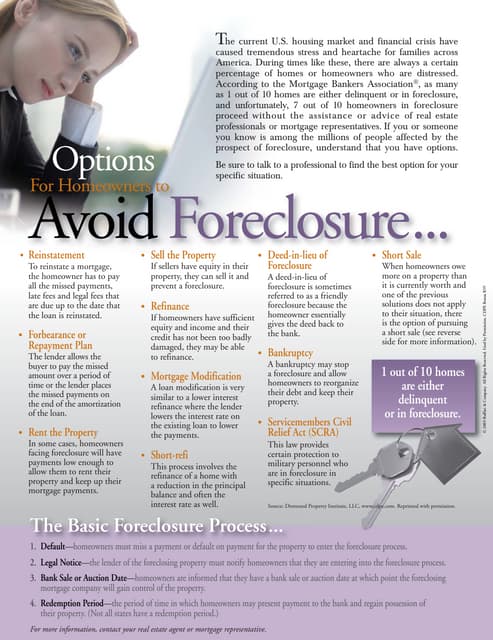

The document provides guidance on FHA mortgage eligibility for borrowers who had previously undergone a short sale or short payoff on their home. It states that borrowers are eligible if they were current on their mortgage at the time of the short sale, but ineligible for 3 years if they were in default. Exceptions can be made if the default was due to circumstances beyond the borrower's control. It also allows for refinancing with a short payoff if the borrower is current and there is insufficient equity or reduced income to pay off the existing debt.