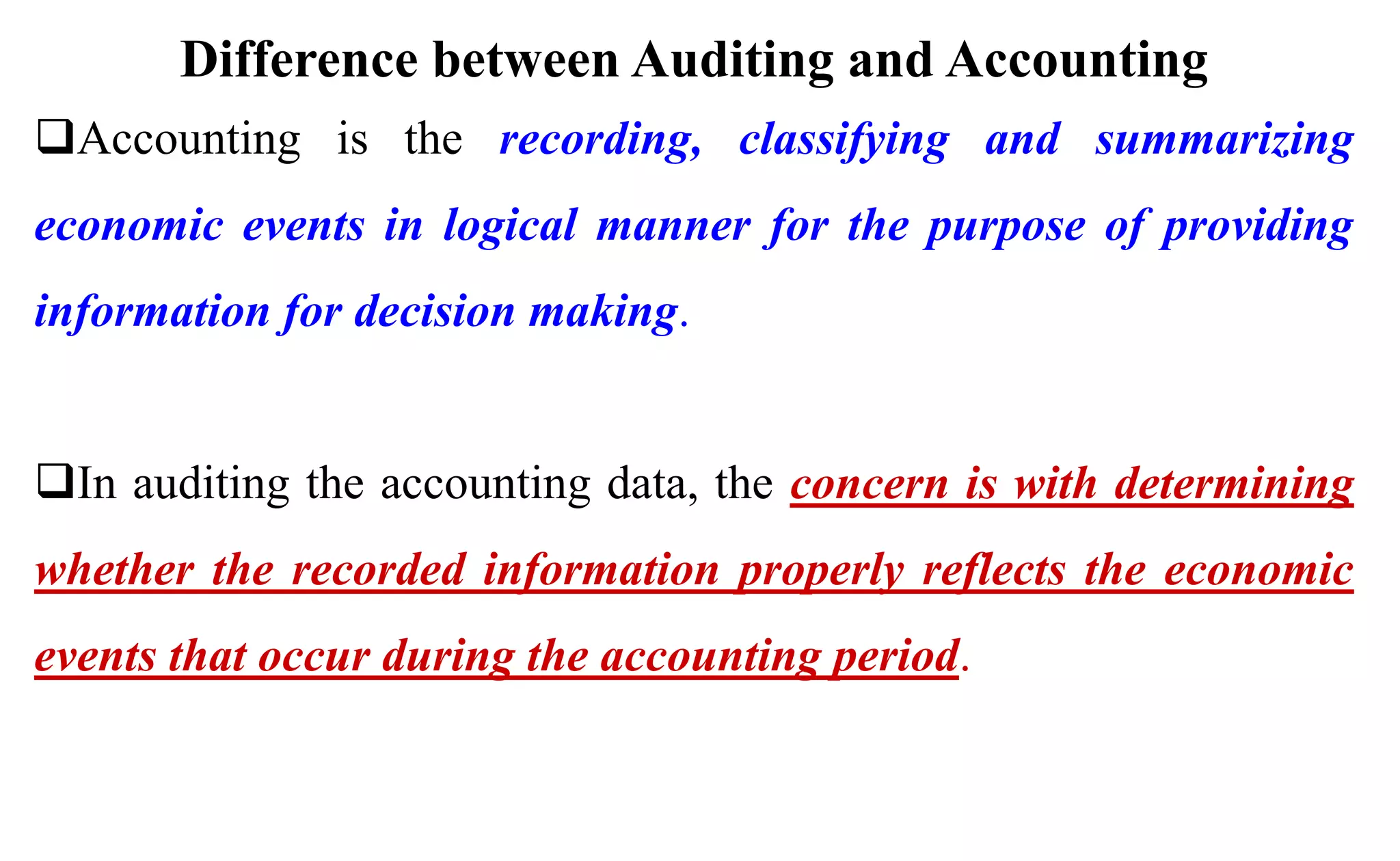

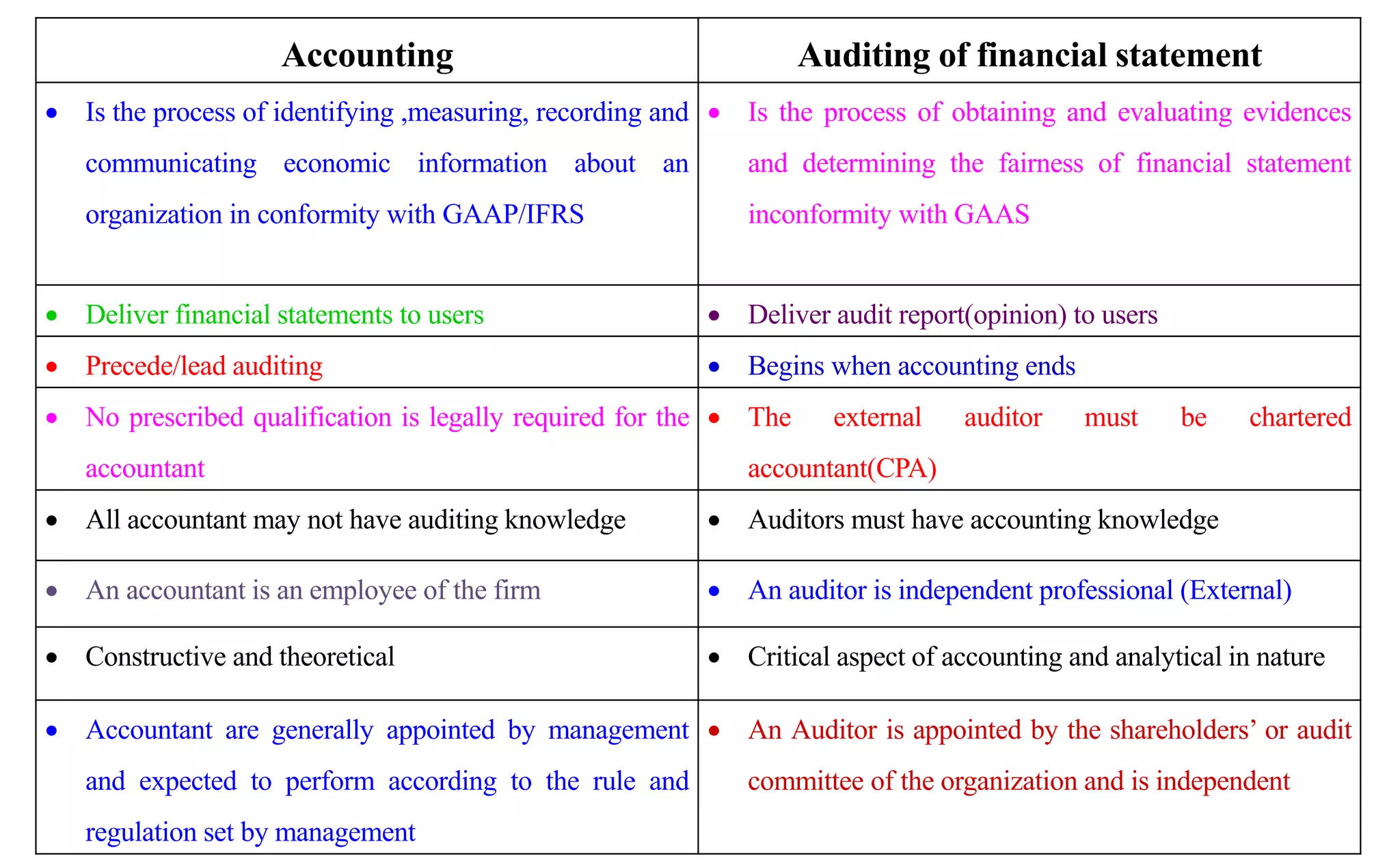

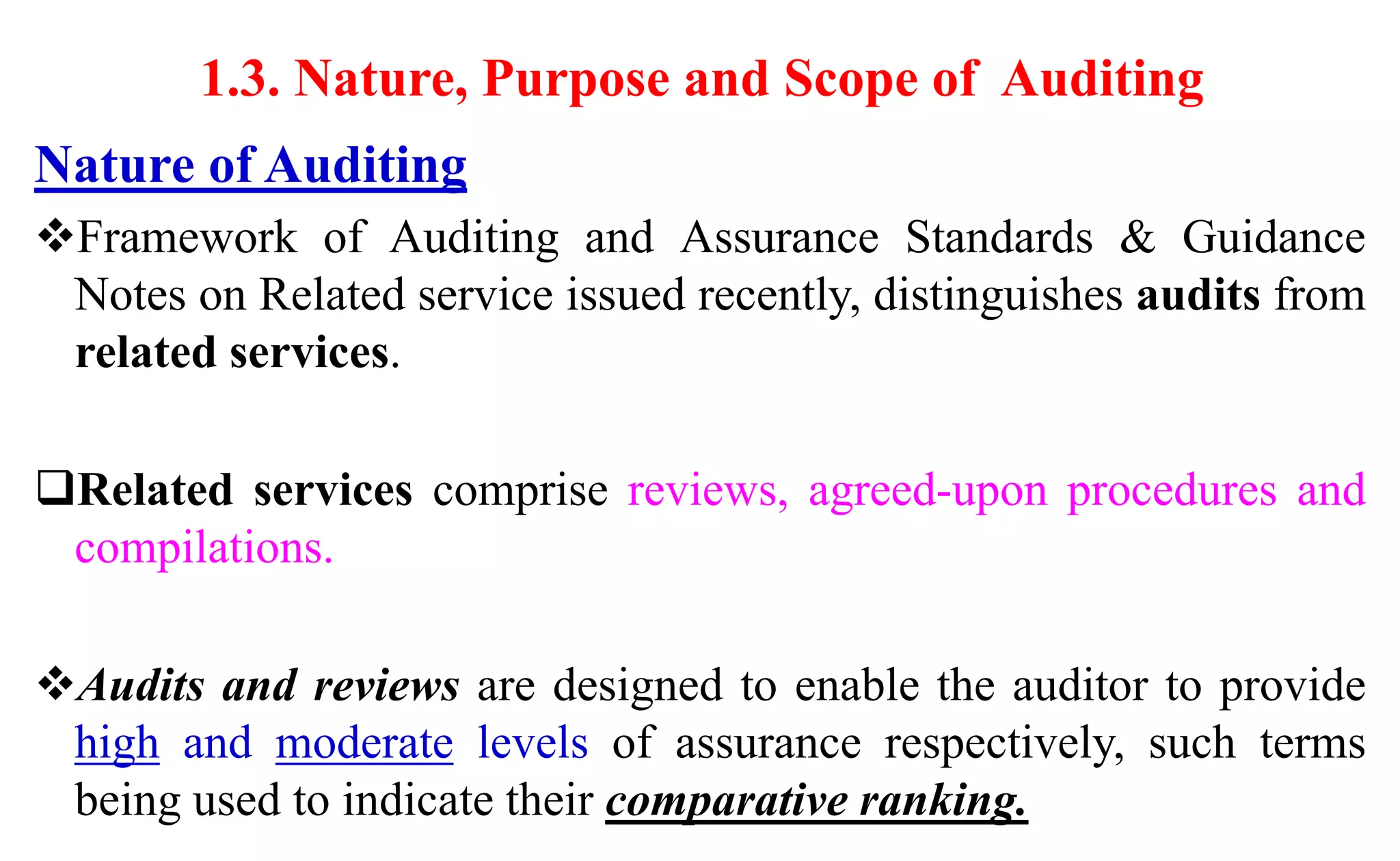

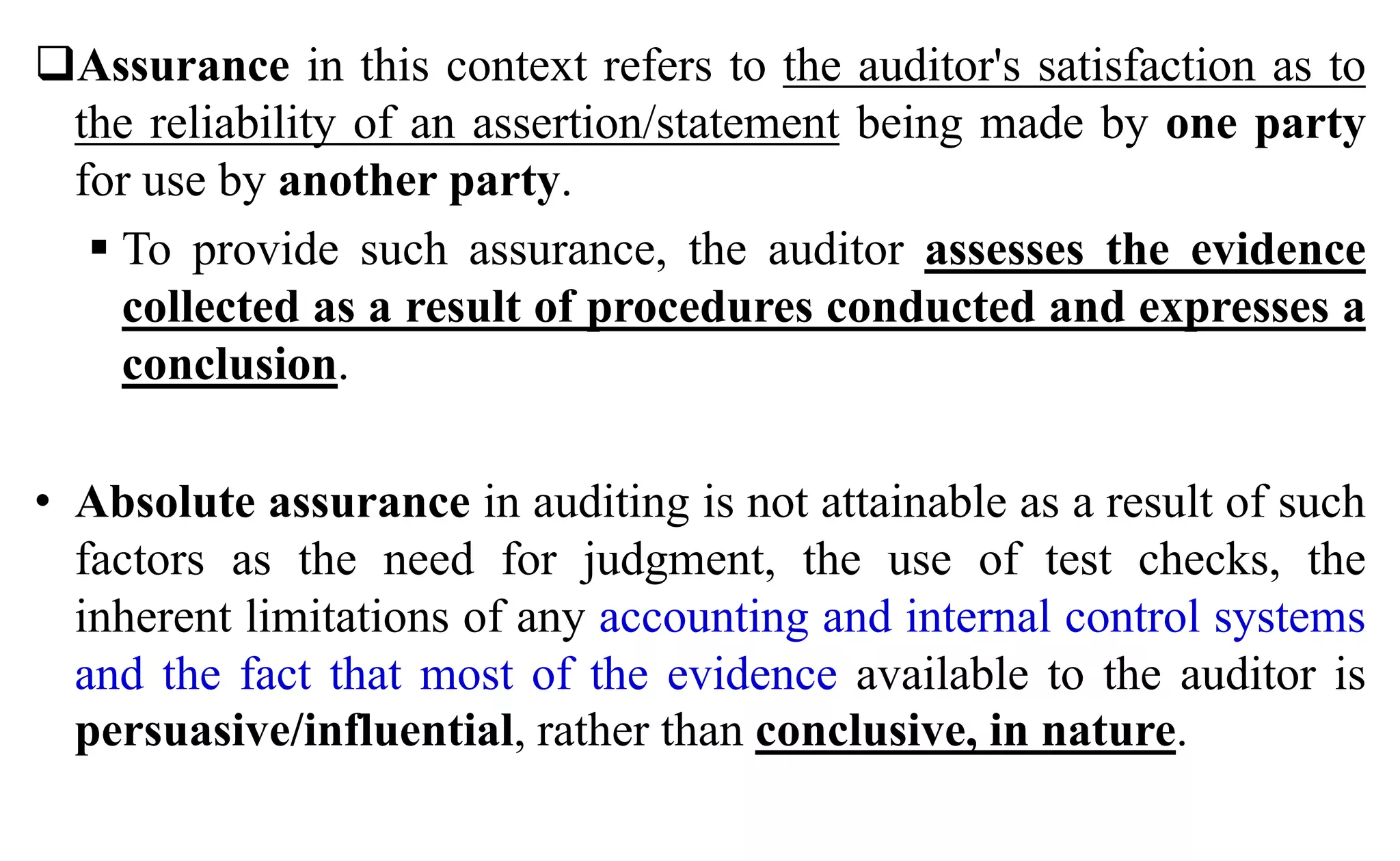

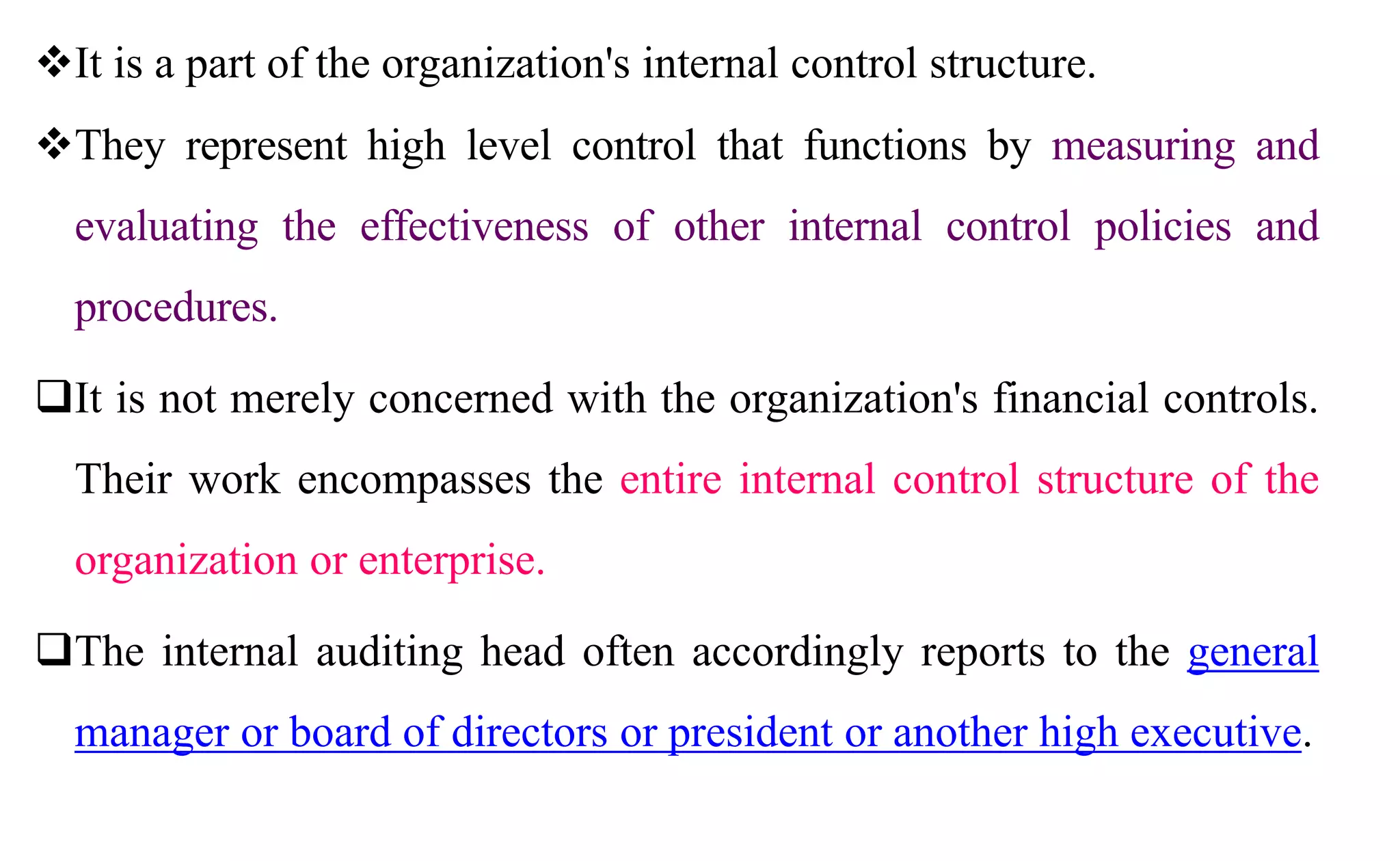

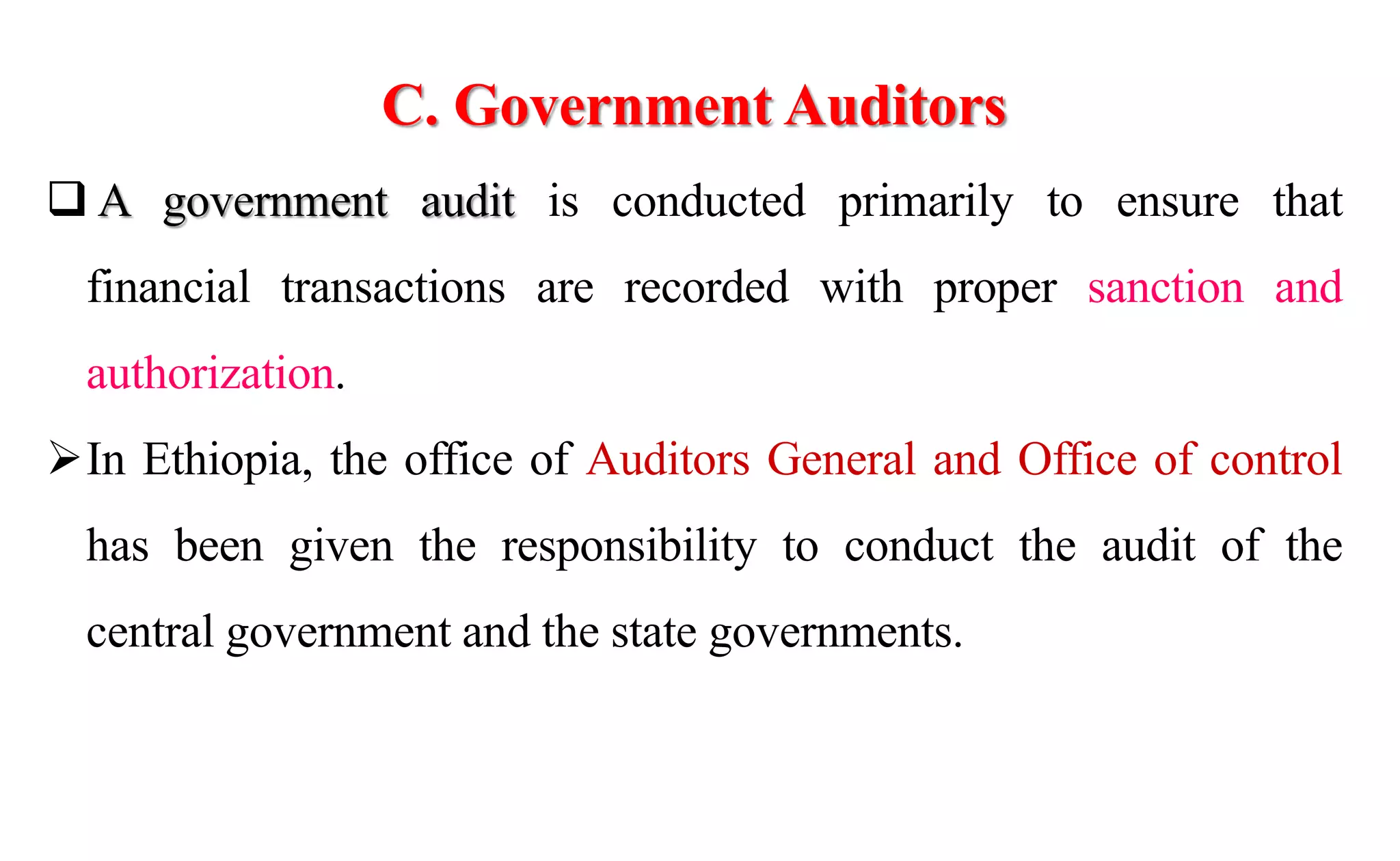

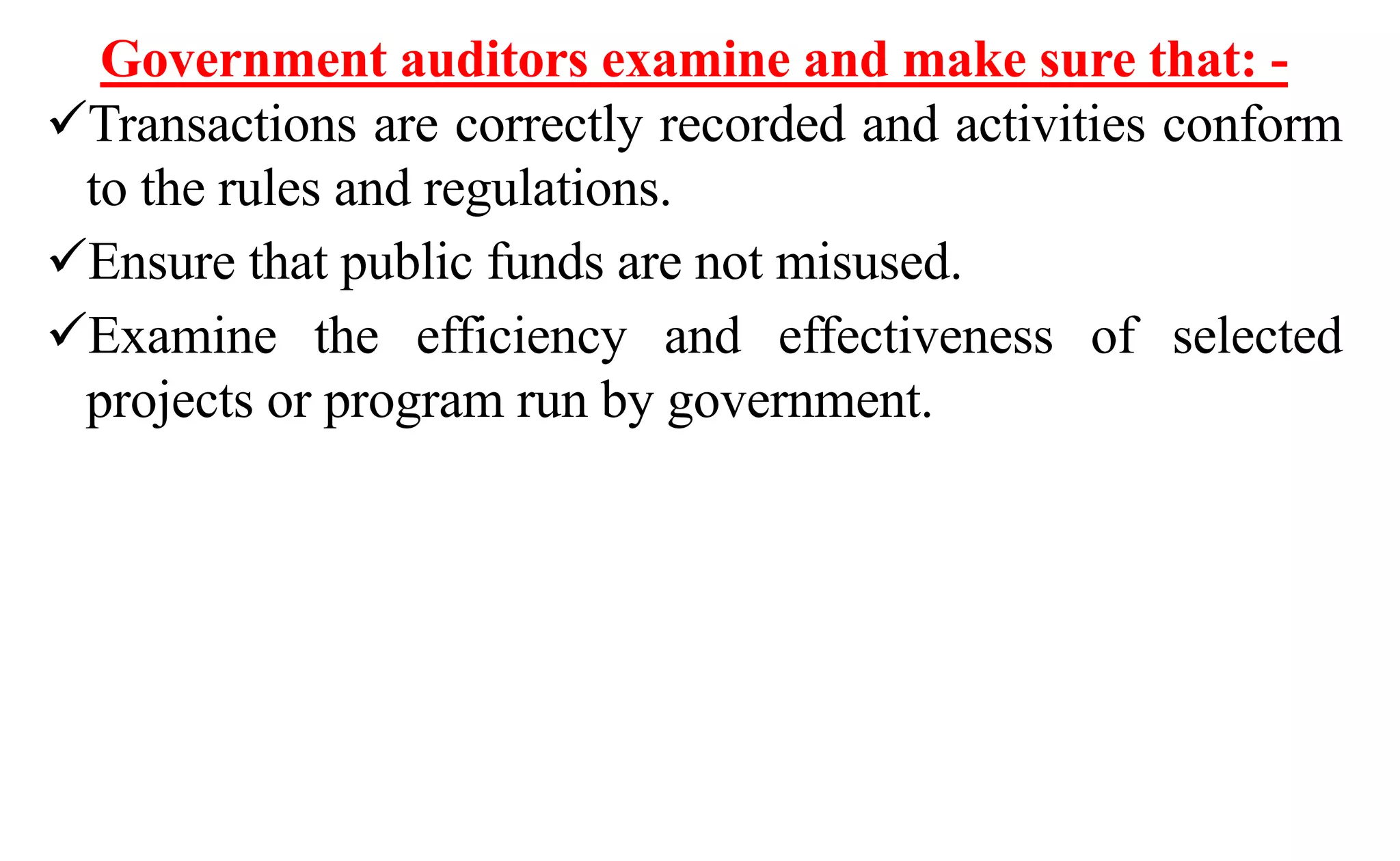

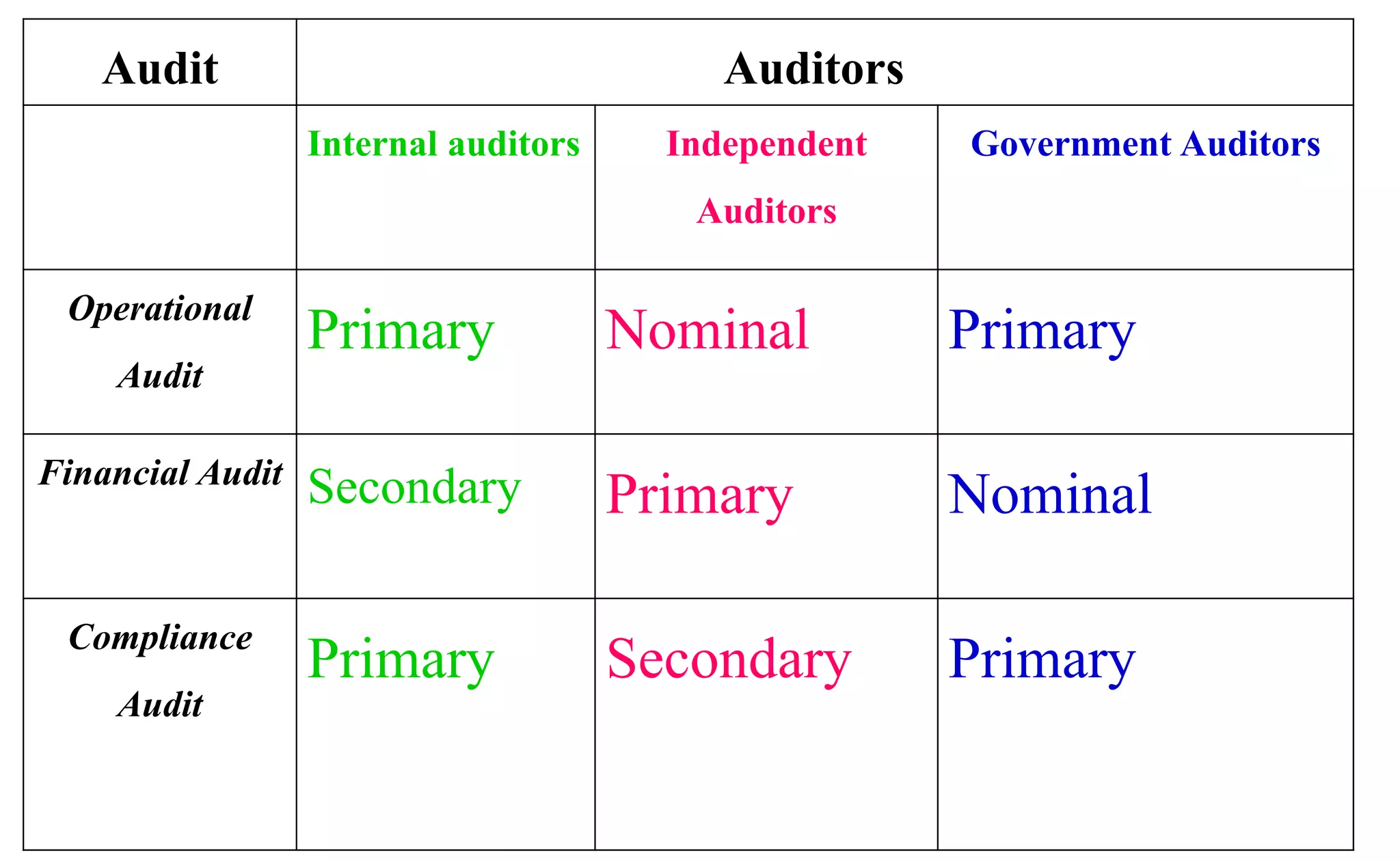

The document provides an introduction to auditing principles and practices. It defines auditing and distinguishes it from accounting. Auditing involves accumulating and evaluating evidence to determine if information matches established criteria, while accounting identifies, analyzes, records and communicates financial information. The purpose of auditing is to provide reliable financial information for decision making and ensure accountability. There are three main types of audits - financial statement audits, compliance audits, and operational/performance audits. Auditors can also be independent, internal to an organization, or from the government.

![• The description of auditing by Arens and Loebbecke includes several

key terminologies which are important.

Information and established criteria: To do an audit, there must be

information in a verifiable form and some standards [criteria] by which the auditor can

evaluate the information.

Accumulating and evaluating evidence: any information used by the auditor

(oral testimony, written communication and observation).

Competent, independent person: The auditor must be qualified & competent

and must have an independent mental attitude.

Reporting: The final stage in the audit process is the audit report,

which is the communication of the findings to users.](https://image.slidesharecdn.com/01auditingch1-220810030631-a5b6c72a/75/01-Auditing-CH-1-ppt-10-2048.jpg)