Equities, interest rates, energy, commodities and currencies have become more correlated in their movements in recent years. This lack of diversification increases volatility and risk for portfolios. The document discusses how quantitative easing policies have caused liquidity to spread beyond domestic markets, influencing commodity prices globally and reducing benefits from diversification across asset classes.

(INDIRA) Call Girl Mumbai Call Now 8250077686 Mumbai Escorts 24x7

Commodity Wealth Creation

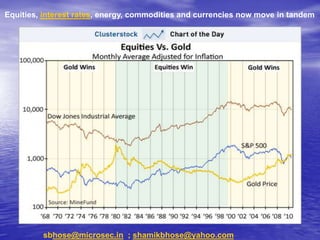

1. Equities, interest rates, energy, commodities and currencies now move in tandem

sbhose@microsec.in ; shamikbhose@yahoo.com

2. Gold will hit $1,650 before the end of the year) (the green line in the chart

below) has held; gold is in a nice channel; we have broken out to new highs; and

mid-March to the end of May is often a strong time of year for gold as is August

to November since 2005 .

This has been falling since 2000, when the Dow was incredibly expensive against

gold. In 1980 methinks that ratio is eventually falling back to 1:1. So, if the Dow

is at 10,000, so will gold be at $10,000. I’m slightly more conservative than that.

But here’s my simplification of his stepping-down pattern:

4. Recent gold versus Dow behaviour suggest that even during periods of stock

market volatility gold has continued to have a relatively smoother journey

upwards and the ratio can get much higher in favour of gold when the blow-

out phase occurs.... The benefits of diversification are thus destroyed and

the volatility of once low-risk portfolios greatly increases. looking further a

field to alternate assets ;

5. These prices have been also influenced by weaker & cheaper cost of money as Fed

monetized debt and flooded the system -- QE 1 ; QE 2 has seeped out to influence

commodity prices = most obvious manifestation is the lack of diversification, fat tail risk!!

The Query for 2011 --* Risk on Risk off + Inverted yield curve + Year Ending Comments

Looking back at -- Fat Tail Risk + Bubbles

6. Consumption: 70% of the US economy is driven by consumption. This in

turn accounts for 20% of the worlds consumption i.e. 5% of the world's

population accounts for 20% of its consumption.

Talk about an imbalance! Savings: The US finances its consumption by borrowing from the

Chinese, Japanese, Mid-East etc.. because they save.... One more area of deep significance is the

45% of GDP is exports for the Asian tigers , that means they are not de-coupled at all with USA in

fact they are anything but given how badly American consumer and consumer credit drives

demand there and how much a tiger like China needs that export market.

7. Risk trades will test investors through 2011

Correlations have continued to increase despite falls in individual asset volatility

U.S. government debt is now over $13.7 trillion (not including estimated

states' debt of $2.8 trillion and agencies' debt of $3.0 trillion). The

average rollover period for the debt is 49 months. With recent deficits

running over $1 trillion a year, the Treasury issues new debt and refunds

old debt at a rate of about $4.3 trillion a year.

A nation needs to inspire a lot of confidence to keep that Ponzi scheme

alive. Unfortunately, markets know that even the U.S. government will

print money to meet expenses when necessary.This leads to the

question, being asked from Beijing to Brussels: Does the risk match the

reward? A negative response to that question could lead to

hyperinflation.

Gold trading at more than $1,440 an ounce, despite no appreciable

increase in the consumer price index, is much more understandable

when you realize that in periods of hyperinflation , gold tends to

appreciate by 2,000% to 50,000% against a hyper-inflated currency.

8. The Lessons Of History

Quantitative easing hasn’t worked for Japan. If it’s going to work in the

U.S., capital controls may be inevitable. The Fed must stop the seepage

of liquidity overseas. It makes no sense for the Fed to take such

monumental risks with its balance sheet if America isn’t reaping the

benefits.

9. Here we see the US dollar index, which shows the dollar against a basket of

foreign currencies.

10. In Bear Market 4 stages -- stage 1: leverage killed

Stage 2: denial: market goes into a quite zone

Stage 3: realisation and pessimism & poison gets flushed out…

Stage 4: abject fear… which creates the base for the next bull market to

germinate…

13. Another week, another new high in gold and silver. The inexorable rise continued

with gold breaking out to new all-time highs at $ xxxx per ounce. It’s now in

positive territory for the year; But here’s the action that surprised me: gold was up

in the face of falling stock markets…and a ranged dollar index

Shamik Bhose

sbhose@microsec.in ; shamikbhose@yahoo.com

15. The best way to play a bull market –buy at the right time and then just sit

tight

I have always said that of all the metals silver has the most potential. There is its

monetary appeal. As a precious metal, investors are seeking it out because of its

increasing value at a time where governments are debasing their currencies. And there

is its industrial appeal. It is finding more and more uses each year in industries that,

recession or no recession, are growing. I’m talking particularly about its use in electrical

and medical applications. Meanwhile there is an ever-increasing supply deficit. Share-

lynx has charted this:

16.

17. Share-lynx says: “Note that since 1950, almost 925,000 tonnes have gone into demand

with 570,000 tonnes of this having come from production. This leaves a shortfall of

350,000 tonnes, which has come from central bank sales, stockpiles and scrap. This

deficit equals approximately 16 years of production”. The scrap is running out.

Meanwhile, on the futures exchanges, there seems to be a genuine supply squeeze which

is pushing prices higher and higher. And since one of the bigger sellers, JP Morgan,

announced the closure of its prop trading desks in late August, the price has catapulted

higher.

18. One day silver, much as it did in 1980, is going to rise higher than your wildest

dreams. (That $50 number from 1980, is somewhere north of $200 in today’s

money.)

22. Nomura set the bar pretty high with a warning that $220 a barrel might even

be overly-conservative should production in Libya and Algeria shut down

altogether. In 2007 Goldman had predicted a 150 $ per barrel of WTI crude

price for 2010 only to see 147$ in 2008

23. To sum up his point, Libya has plenty of oil money and should have been able to

bribe its citizens into submission. But they decided they want freedom instead.

And if “that is the case with Libya, which has a comparable ratio of income to

population to Saudi Arabia, one might worry more about the stability of Saudi Arabia,

which is of course the big one”. That’s an understatement.

24. A New Superabundance of Game-Changing Shale Gas Will Provide 250 Years of

Natural Gas A few years ago the United States was ready to import gas. In 2009 it had

become the world's biggest gas producer.

The U.S. achieved the change through a technological breakthrough in which firms

found a way of using tiny explosions to free gas previously trapped in a common rock

- shale.

Tactically this makes Americans less dependent on Middle East and Suez Canal and it

also means over time as this plays out – the dollar will regain traction vis-à-vis other

currencies............

25. 60990456, 60990522, 60990205 1750

1700

1650

1600

1550

A substantial tonnage of 1500

1450

corn has been used as 1400

ethanol bio-fuel in USA 1350

1300

with the help of generous 1250

1200

subsidies and green lobby 1150

1100

media campaigns; this has 1050

raised an ethical debate – 1000

950

if food should be diverted 900

850

with subsidy to become 800

750

fuels as crop shortages 700

and inflations have created 650

600

SOYBEAN

riots and surging grain 550

500

prices have been helped 450

along with the Fed’s cheap WHEAT

400

350

and easy money policies 300

250

200

CORN

150

100

50

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Attracted by these high prices farmers in USA have planted huge crops but weather

has been truant ; substantial Chinese and Russian demands as dollar has been weak

has added to price rise along with massive hedge fund and index fund participation.

All these connections are not linear though

26. Raw sugar and white sugar prices have been strong and getting higher as

crop shortages and demand have both played a part in the rally as has higher

crude oil prices as many countries notably Brazil uses sugar ethanol to fire

up flexi-fuel cars

SUG AR 11 CO NT INUOUS 112000 LBS [NY CSCE] (30.6000, 30.7600, 29.0000, 29.8800), LIG HT CRUDE CO NT INUO US 1000 BARRELS [ NYMEX] (101.700, 104.940, 101.540, 104.420)

155 38

150 37

36

145

35

140

34

135 33

130 32

SUG AR 31

125

30

120

29

115 28

110 27

105 26

25

100

CRUDE OI L 24

95

23

90 22

85 21

80 20

19

75

18

70 17

65 16

60 15

14

55

13

50

12

45 11

40 10

9

35

8

30

7

25

6

A S O N D 2005 A M J J A S O N D 2006 A M J J A S O N D 2007 A M J J A S O N D 2008 A M J J A S O N D 2009 A M J J A S O N D 2010 A M J J A S O N D 2011