Download as PDF, PPTX

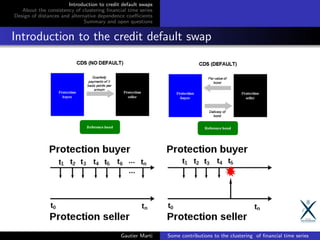

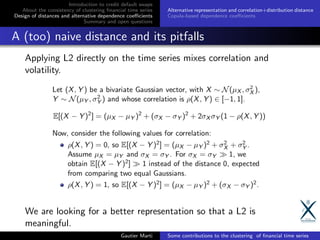

![Introduction to credit default swaps

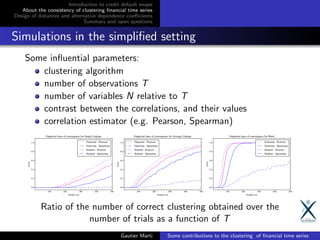

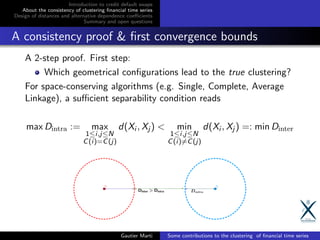

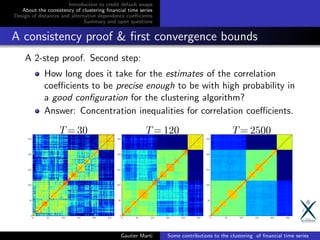

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Some movation for using clustering

Statistical modelling is difficult as the time series

are non stationary, e.g. economic regimes are changing, it

can be misleading to use data from a too distant past

are near efficient, i.e. behaving nearly like random walks (cf.

the efficient-market hypothesis (Fama, 1970) [5])

have a low signal-to-noise ratio, i.e. measure artifacts hide

information in random fluctuations

are in an unfavorable statistical setting, too few relevant

observations (length) wrt the number of variables (time series)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-4-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Introduction to the CDS raw dataset

Putting Self-Supervised Token Embedding on the Tables [15]

(ICMLA 2017)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-9-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

A ‘tick-by-tick’ dataset

Autoregressive Convolutional Neural Networks for Asynchronous

Time Series [1] (ICML Time Series WS 2017)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-10-320.jpg)

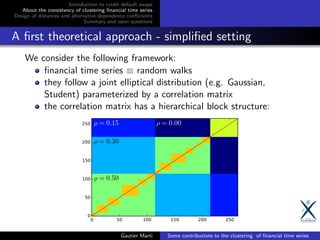

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Clustering of Financial Time Series

Stylized fact I: Financial time series correlations have a strong

hierarchical block diagonal structure (Mantegna, 1999) [6]

https://gmarti.gitlab.io/ml/2017/09/07/how-to-sort-distance-matrix.html

Stylized fact II: Most correlations are spurious (Bouchaud,

1999) [3]

Motivation for clustering financial time series using correlation as a

similarity measure:

dimensionality reduction ≡ filtering noisy correlations

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-13-320.jpg)

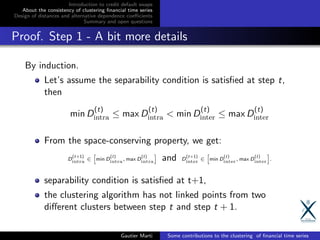

![Hierarchical clustering algorithms - A taxonomy

We consider Hierarchical Agglomerative Clustering algorithms.

Such as single linkage, average linkage, Ward.

Space contracting vs. Space conserving vs. Space dilating [2]

D(t+1)

C

(t)

i

∪ C

(t)

j

, C

(t)

k

≤ min D

(t)

ik

, D

(t)

jk

D(t+1)

C

(t)

i

∪ C

(t)

j

, C

(t)

k

∈

min D

(t)

ik

, D

(t)

jk

, max D

(t)

ik

, D

(t)

jk

D(t+1)

C

(t)

i

∪ C

(t)

j

, C

(t)

k

≥ max D

(t)

ik

, D

(t)

jk

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-16-320.jpg)

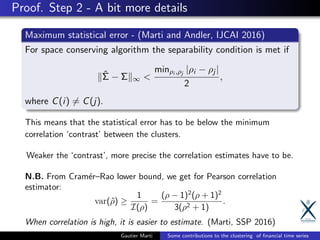

![Correlation estimates concentration bounds

number of variables N, observations T, minimum separation d

Concentration bounds [4]

If Σ and ˆΣ are the population and empirical Spearman correlation

matrices respectively, then for N ≥ 24

log T + 2, we have with

probability at least 1 − 1

T2 ,

ˆΣ − Σ ∞ ≤ 24

log N

T

.

P(“correct clustering”) ≥ 1 − 2N2

e−Td2/24

Not sharp enough for reasonable values of N, T, d.

For example, for N = 500, T = 2500, d = 0.2, we obtain

≈ −7750.

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-23-320.jpg)

![Future developments & open questions

Bounds are not sharp enough. We can try to refine them using:

(theoretical) Intrinsic dimension of the HCBM model [16];

(theoretical Use PSD-ness to refine the bounds for the matrix

(theoretical/empirical) A distance between dendrograms

(instead of correct/incorrect) for a finer analysis;

(empirical) A study of ‘correctness’ isoquants:

Precise convergence rates of clustering methodologies can provide

a useful model selection criterion for practitioners!

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-24-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

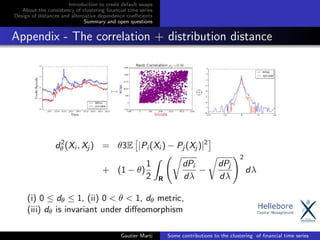

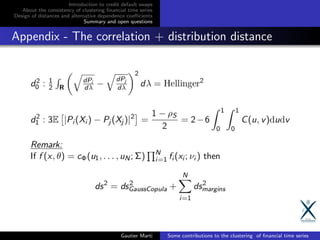

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

A novel representation for time series

Basically, we transform each time series of returns to a (normalized

ranks, square root of marginal density) vector.

Applying a L2 between two of these vectors is now equivalent to a

distance in Spearman correlation + Hellinger between the densities.

cf. (Marti et al., 2016) [13] (Pattern Recognition Letters) for more

details on this representation and the associated distance.

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-31-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

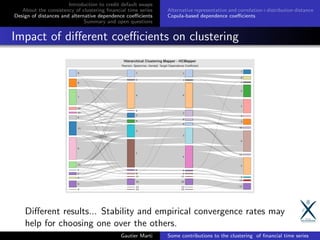

Analysing the differences - Using the Sankey diagram

cf. (Marti et al., 2015) [14] (ICMLA 2015) for guidelines on how to

compare several clustering methodologies for financial time series.

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-32-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

Relation to existing dependence coefficients

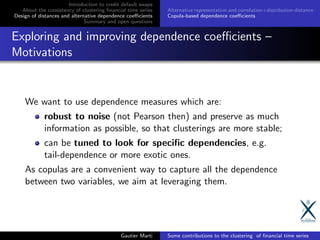

Some dependence coefficients can be readily expressed as:

deviation from Fr´echet-Hoeffding bounds

Spearman’s ρS = 1 − 6 [0,1]2 (ui − uj )2

dC(ui , uj ),

Gini’s γ,

Kendall distribution distance,

deviation from independence ui uj

Spearman ρS = 12 [0,1]2 (C(ui , uj ) − ui uj )dui

duj

,

Copula MMD,

Schweizer-Wolff’s σ,

Hoeffding’s φ2

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-35-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

Optimal Transport between empirical copulas

cf. (Marti et al., 2016) [12] (ICASSP 2016)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-37-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

Why choosing Optimal Transport over f -divergences?

Distances between Gaussian copulas C1, C2, C3:

cf. (Marti et al., 2016) [7] (SSP 2016)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-38-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

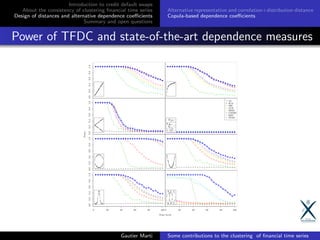

Standard setting: TFDC vs. Spearman

cf. (Marti et al., 2017) [8] (NIPS Time Series WS 2016)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-39-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Alternative representation and correlation+distribution distance

Copula-based dependence coefficients

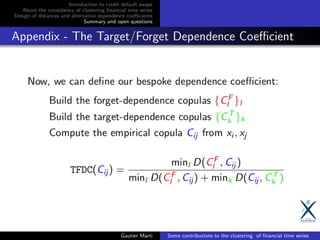

Some applications of the Target/Forget Dependence

Coefficient

Applications in non-standard settings: We can look for particular

associations between random variables.

cf. (Marti et al., 2017) [8] (NIPS Time Series 2016)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-41-320.jpg)

![Introduction to credit default swaps

About the consistency of clustering financial time series

Design of distances and alternative dependence coefficients

Summary and open questions

Summary of contributions

The contribution of the PhD thesis:

bring a greater focus on statistical reliability (convergence

rates and consistency) [9] (IJCAI 2016)

consider alternative representation and distances [13]

(Pattern Recognition Letters), [8] (NIPS Time Series 2016)

visualizations [10] and a framework to test for clustering

stability [14] (ICMLA 2015)

an extensive and regularly updated survey of the literature:

https://arxiv.org/pdf/1703.00485.pdf [11] (350+

references)

Gautier Marti Some contributions to the clustering of financial time series](https://image.slidesharecdn.com/gmartiphddefense-171111143021/85/Some-contributions-to-the-clustering-of-financial-time-series-Applications-to-credit-default-swaps-44-320.jpg)

This document discusses contributions to clustering financial time series, specifically credit default swap data. It introduces credit default swaps and the raw data set. It then discusses challenges in clustering financial time series due to non-stationarity and noisy correlations. It presents initial work on analyzing the consistency of clustering as the sample size increases, through simulations in a simplified setting. Finally, it proposes a two-step approach to proving consistency, by first identifying geometrical configurations that lead to the true clustering structure.