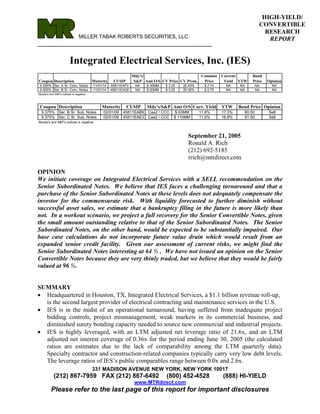

1. HIGH-YIELD/

CONVERTIBLE

RESEARCH

MILLER TABAK ROBERTS SECURITIES, LLC REPORT

__________________________________________________

Integrated Electrical Services, Inc. (IES)

Mdy's/ Common Current Bond

Coupon Description Maturity CUSIP S&P Amt O/S CV Price CV Prem. Price Yield YTW Price Opinion

6.500% Ser. A Sr. Conv. Notes 11/01/14 45811EAF0 NA $ 30MM $ 3.25 20.43% $ 2.70 NA NA NA NA

6.500% Ser. B Sr. Conv. Notes 11/01/14 45811EAG8 NA $ 20MM $ 3.25 20.36% $ 2.70 NA NA NA NA

Moody's and S&P's outlook is negative.

Coupon Description Maturity CUSIP Mdy's/S&P Amt O/S Curr. Yield YTW Bond Price Opinion

9.375% Ser. B Sr. Sub. Notes 02/01/09 45811EAB9 Caa2 / CCC $ 63MM 11.6% 17.3% 80.50 Sell

9.375% Ser. C Sr. Sub. Notes 02/01/09 45811EAE3 Caa2 / CCC $ 110MM 11.5% 16.8% 81.50 Sell

Moody's and S&P's outlook is negative.

September 21, 2005

Ronald A. Rich

(212) 692-5185

rrich@mtrdirect.com

OPINION

We initiate coverage on Integrated Electrical Services with a SELL recommendation on the

Senior Subordinated Notes. We believe that IES faces a challenging turnaround and that a

purchase of the Senior Subordinated Notes at these levels does not adequately compensate the

investor for the commensurate risk. With liquidity forecasted to further diminish without

successful asset sales, we estimate that a bankruptcy filing in the future is more likely than

not. In a workout scenario, we project a full recovery for the Senior Convertible Notes, given

the small amount outstanding relative to that of the Senior Subordinated Notes. The Senior

Subordinated Notes, on the other hand, would be expected to be substantially impaired. Our

base case calculations do not incorporate future value drain which would result from an

expanded senior credit facility. Given our assessment of current risks, we might find the

Senior Subordinated Notes interesting at 64 ½ . We have not issued an opinion on the Senior

Convertible Notes because they are very thinly traded, but we believe that they would be fairly

valued at 96 ½.

SUMMARY

• Headquartered in Houston, TX, Integrated Electrical Services, a $1.1 billion revenue roll-up,

is the second largest provider of electrical contracting and maintenance services in the U.S.

• IES is in the midst of an operational turnaround, having suffered from inadequate project

bidding controls, project mismanagement, weak markets in its commercial business, and

diminished surety bonding capacity needed to source new commercial and industrial projects.

• IES is highly leveraged, with an LTM adjusted net leverage ratio of 21.6x, and an LTM

adjusted net interest coverage of 0.36x for the period ending June 30, 2005 (the calculated

ratios are estimates due to the lack of comparability among the LTM quarterly data).

Specialty contractor and construction-related companies typically carry very low debt levels.

The leverage ratios of IES’s public comparables range between 0.0x and 2.6x.

331 MADISON AVENUE NEW YORK, NEW YORK 10017

(212) 867-7959 FAX (212) 867-6492 (800) 452-4528 (888) HI-YIELD

www.MTRdirect.com

Please refer to the last page of this report for important disclosures

2. • Near-term liquidity appears sufficient, providing management with a window to affect a

turnaround. Management has proven that it can raise additional liquidity through the sale of

business units, thirteen of which have been completed in the past eleven months. We are

concerned that future divestitures may prove more difficult to complete and less financially

productive. Management is currently behind on the divestiture schedule it provided on the

latest conference call. IES may also have the ability to extend its liquidity by expanding its

current senior credit facility, though we project default under the Fixed Charge Coverage

covenant in the first quarter ending December 31, 2005.

• IES is dealing with reduced surety bonding capacity. Given a shrinking backlog, it is unclear

whether the company will be successful in replacing large bonded projects with a sufficient

number of smaller ones. As a result, we fear a declining revenue line in its commercial and

industrial business units and a further impaired EBITDA margin. We also question whether

management-projected improved gross margin will be eroded by increased business

development costs associated with a greater number of projects.

• There has been substantial turnover within the senior management ranks over the past fiscal

year (ending September 30, 2005). While we do not believe that this is necessarily bad, we

are concerned with the possible implications. Additionally, conversations with industry

sources have pointed to potentially damaging attrition at IES’s subsidiaries.

• Our view to risk is colored by the potentially low reorganization value of a troubled

construction company, particularly one whose main asset is its workforce. Our recovery

analysis assumes that IES’s Residential segment is successfully reorganized, while the

Company’s commercial units are sold.

• Given our evaluation of the current risks associated with IES’s turnaround, we have based

our target pricing on a required return of 9% for the fixed income piece of the Senior

Convertible Notes and 15% for the Senior Subordinated Notes.

BACKGROUND

Integrated Electrical Services, Inc. (“IES” or the “Company”) was created in June 1997 to serve

as a leading national provider of electrical contracting and maintenance services to the

commercial, industrial and residential markets. Concurrent with the closing of its January 1998

initial public offering, IES acquired fifteen electrical contracting and maintenance service

companies and a related supply company, making it one of the largest competitors in the

domestic electrical specialty contracting space. Pro forma revenues for the newly formed entity

were $312.7 million, of which 63% was derived from commercial and industrial contracting,

25% from residential contracting, and 12% from electrical maintenance work.

IES was one of a number of specialty contractor roll-ups which occurred in the late 1990’s. The

roll-ups were driven by market fragmentation, the availability of capital, public versus private

market valuation arbitrage, as well as by visions of increased competitive advantage resulting

from an augmented market footprint, economies of scale, cross-selling and expertise

transference; twelve engineering and construction companies went public between 1997 and

2000.

Since its founding, IES has grown primarily through acquisitions, making 71 acquisitions from

April 1998 through December 2000. Presently comprised of 36 active business units with

estimated annual revenues of $1.1 billion, much of the Company’s current leverage was incurred

to finance this growth. IES fundamentals began to decline in fiscal year 2002 as a result of

2

3. increased competition and project mismanagement. Recently, the Company has been negatively

impacted by rapidly rising material costs and a difficult surety bonding environment. Losses

experienced by the surety industry in recent years have caused insurers to limit surety capacity

and increase costs to customers. In response, IES has divested thirteen business units, fiscal

year-to-date, that are heavily reliant upon surety bonding. Company management is presently

focusing on improving project bidding and execution, sourcing shorter term projects, as well as

reducing overhead costs.

BUSINESS

Headquartered in Houston, TX, Integrated Electrical Services is the second largest provider of

electrical contracting and maintenance services in the United States, following Quanta Services.

IES’s electrical contracting services include the design of electrical distribution systems, the

procurement and installation of wiring and fixtures within structures, as well as the long-term

maintenance of these systems. These installations support a variety of purposes, including

climate control, security and communications.

Within commercial structures, IES electricians will place piping or tubing, referred to as conduit,

inside designated partitions and walls; in residential construction, plastic-covered wire is usually

used in place of conduit. Insulated wires or cables are then run through the conduit to connect

various electrical boxes which house switches and outlets. The wiring is then connected to

circuit breakers, transformers, or other components. Upon completion of the installation, the

system is tested to ensure proper connectivity and safety. IES also installs low voltage wiring

systems, such as voice, data, and video wiring systems typically used for telephones, computers,

intercoms, fire alarms and security systems.

Success in the electrical contracting business is reliant upon an entrepreneurial spirit which may

prove to be unsustainable in a $1.1 billion roll-up which requires that the more profitable

business units financially support the less profitable ones. Illustrating this point, one industry

executive, in describing the owner of a Houston-based IES competitor, is quoted as saying, “He

has a following of top people…The way [he] runs his business, he pays his people more than

anybody else, he rewards them more than anybody else, but he expects them to move mountains

for him. So they work hard, but they have fun doing it. There’s a lot of loyalty from the people

who work for him” (Source: Dallas Business Journal, April 14, 2003).

Operating Segments

Commercial and Industrial. IES’s commercial work (70% of revenues) consists primarily of

electrical installations and renovations in office buildings, high-rise apartments and

condominiums, hotels, retail stores and centers, schools, community centers, theaters and

stadiums. Within industrial construction, the Company provides services for utilities, including

power generation and overhead and underground lines, water facilities, manufacturing and

processing facilities, highway and transportation projects, military installations, and airports.

IES’s customer base is comprised of general contractors, developers, building owners and

managers, engineers, architects and consultants. No customer accounts for more than 10% of

revenues.

New business is typically sourced through long-standing relationships. After reviewing the

engineer’s plans and meeting with the client, the IES business unit will construct cost estimates

3

4. and submit its bid for the project. If the project is awarded, it is scheduled in phases and

incrementally billed as it is completed, net of a 5% to 10% retainage based on total project cost.

The Commercial and Industrial (“C&I”) segment is characterized by long, complex projects

which are executed under fixed-priced or guaranteed maximum price contracts. This contract

structure has exposed IES to compromised margins resulting from under-bidding and cost

overruns and recently led management to shorten project duration and to shift revenue mix

toward its residential operating segment. IES’s average contract is currently between $500,000

and $600,000 and requires between six and nine months to complete. As of the third quarter of

2005, commercial and industrial revenue accounted for 70% of total revenue, down from 77% in

the prior year’s quarter. Much of the shift has been accomplished through the divestiture of

business units which focus on commercial and industrial contracting. This change in service mix

has also been motivated by an increasingly difficult surety bonding environment, a dynamic

which will be addressed in detail below in the Recent Trends section.

Residential. Anchored by subsidiary Houston-Stafford of Stafford, TX, IES is the largest

residential electrical contractor in the country. The Residential segment provides electrical

installations for developers of new single family homes and multi-family low-rise apartments,

condominiums and town homes. IES’s residential operating segment is considerably more

profitable than its commercial and industrial segment, typically executing projects which are

shorter in project duration and less complex. Also, the surety bonding requirement for this

segment is considerably lower. Demand for residential work is seasonal in nature, with higher

revenues generated during the spring and summer quarters (Q3 and Q4). Single-family

installations are not entered into the Company’s backlog.

Project Financial Structure

Revenues. Electrical contracting typically comprises 10% of the total construction costs of a

given project. IES recognizes revenue from construction contracts on a percentage-of-

completion method, whereby costs incurred and accrued to-date are compared with the estimated

total cost for each contract. While this methodology is common, its accuracy is vulnerable to

revisions in project costs produced by inaccurate bidding, and poor project management, job

performance and job conditions. The Company recently encountered errors at three of its

subsidiaries relating to improperly recording revenues associated with change orders, costs

charged to certain contracts and the estimates of costs to complete on certain contracts. As a

result, reported results for the six months ended March 31, 2004 and the years ended September

30, 2002 and 2003 have been revised, reflecting a decrease in operating profit in the amount of

$4.5 million, $1.0 million and $0.8 million, respectively.

Costs. IES’s operating costs are comprised mainly of materials, labor and insurance. Materials

are ordered for a particular project and are typically utilized within 30 days. They consist of

commodity-based products such as conduit, wire, fuses, fixtures and control panels. At the

commodity level, IES makes use of steel, copper and gasoline. While the Company does hedge

its materials exposure on fixed-priced contracts to a reasonable extent, the contracts do not

contain material escalation clauses, leaving IES vulnerable to rapidly rising commodity pricing.

Material cost savings are one of the touted benefits of roll-ups such as IES, but such savings

are often absorbed by increased overhead and compliance costs. For the years ending

September 30, 2002, 2003 and 2004, materials expense as a percentage of cost of services was

42%, 43% and 51%, respectively.

4

5. As a non-union shop, IES benefits from lower employee benefit costs, as well as more flexible

work rules. In a tight labor market, though, labor costs can effectively become less variable. In

what is considered an ongoing and ever increasing labor shortage of electricians, we believe that

IES is currently faced with supporting an underutilized labor force in some of its markets,

due to Company anticipation of an up-tick in commercial electrical contracting demand

and the commensurate difficulty with staffing up. For the years ending September 30, 2002,

2003 and 2004, labor and related expenses as a percentage of cost of services was 43%, 42% and

48%, respectively.

Geographic Markets

As of August 6, 2005, IES had 36 active business units and over 100 Figure 1

locations serving the continental U.S. During the formation of IES, Business Unit

management touted the competitive advantage that a national footprint Headquarter Locations

As of September 9, 2005

would provide in competing for projects with national or regional

customers. Outside of service work, this does not appear to have been Region Southeast

State No. Units

AL 1

the case, given the local nature of construction and contracting. Figure FL 2

GA 1

1 delineates our estimate of IES’s current business unit headquarter KY 1

locations. While it has a national presence, the Company has NC 1

SC 2

derived the majority of its revenue from the Sunbelt states. As TN 2

VA 3

shown in Figure 2, nearly 70% of revenue has historically come from 13

the South, with the Mid-Atlantic and Northeast a distant second. It is West AZ 3

CA 2

evident in the following charts (see Figures 3a-3c) that private CO 1

nonresidential construction put-in-place spending is down from its OR 3

NV 2

2000 to 2001 highs and is essentially running flat in IES’s main WA 1

12

markets. On a national basis, year-over-year monthly growth of Southwest TX 9

private nonresidential construction put-in-place spending has leveled Midwest IA 1

NE 1

off at approximately 5%, as compared with what had been a trend of OH 1

increases over the second half of 2004 (see Figure 3a). Spending in 3

Mid-Atlantic MD 2

the Southeast region has grown by approximately 4% in years 2003 Northeast MA 1

and 2004 (see Figure 3b), while in the Southwest region, spending has SUBTOTAL 40

declined (see Figures 3c). Construction spending forecasts are Less adjustments 4

TOTAL 36

Figure 2 addressed below in Source: Company and MTR estimates.

the Outlook

Percentage of Revenue by Region section. According to our market feedback,

As of June 2004 demand within IES’s commercial markets

varies considerably. Florida, for example, is

Southwest,

10%

one market in which customers seem

Northeast, 6% desperate for electrical contracting services,

South, 34%

Mid-Atlantic, while in Texas demand is considered anemic

14% throughout the industry. It is anticipated,

Midwest, 5% though, that a number of Texas markets will

Northwest, 6% rebound on the heels of rising oil and gas

Southeast,

25%

prices. As for Hurricane Katrina,

management has stated that, though IES

Source: Company.

does not have a presence in the affected

areas, the tragedy may result in additional

work for regionally located business units and/or increased project margins due to reduced

contractor capacity in its markets.

5

6. Figure 3a

Private Nonresidential Construction Put-In-Place

National - Seasonally Adjusted Annual Rate

250,000 10.0%

Percentage Change

Dollars in Millions

245,000 8.0%

240,000 6.0%

235,000 4.0%

230,000 2.0%

225,000 0.0%

Se 4

' 05

'04

M 5

M 5

'05

A 4

N 4

D 4

'04

A 5

Fe 5

'0

'0

'0

'0

0

'0

'0

'0

l'

ug

ay

n

ct

p

ov

b

ar

pr

ec

n

Ju

Ju

Ja

O

Spending Year-Over-Year Change

Source: Department of Commerce.

Figure 3b

Private Nonresidential Construction Put-In-Place

Southeast Region

70,000 30.0%

Percentage Change

Dollars in Millions

60,000

20.0%

50,000

40,000 10.0%

30,000 0.0%

20,000

-10.0%

10,000

0 -20.0%

94

95

96

97

98

99

00

01

02

03

04

19

19

19

19

19

19

20

20

20

20

20

Spending Annual Change

Source: Department of Commerce.

Figure 3c

Private Nonresidential Construction Put-In-Place

Southwest Region

30,000 30.0%

Percentage Change

Dollars in Millions

25,000 20.0%

20,000

10.0%

15,000

0.0%

10,000

5,000 -10.0%

0 -20.0%

94

95

96

97

98

99

00

01

02

03

04

19

19

19

19

19

19

20

20

20

20

20

Spending Annual Change

Source: Department of Commerce.

6

7. RECENT TRENDS

Surety Bonding

Surety bonding has historically been an important component of new business development for

IES. Large projects and government funded projects typically always require the Company to

post bid, payment and performance bonds. A surety bond is a three-party instrument among a

surety, the contractor and the project owner. The agreement requires the contractor to comply

with the terms and conditions of a contract. If the contractor is unable to successfully perform

the contract, the surety assumes the contractor’s responsibilities and ensures that the project is

completed.

Financial losses experienced by surety providers in recent years have led providers to tighten

underwriting standards and caused many to leave the business entirely. IES’s faltering

fundamentals in its Commercial and Industrial segment have led IES’s surety provider, Chubb,

to limit bonding capacity and to secure most of its exposure. As of June 30, 2005, IES had $110

million of cost-to-complete on bonded projects, as compared with $151 million as of March 31,

2005. Of this amount, collateral was comprised of $18.0 million in cash, $11.4 million in letters

of credit and $60 million in receivables, summing to 81% of total exposure.

These limitations on securing bonding have altered IES’s strategic direction. Through a change

in projects bid and a recent divestiture program, the Company has refocused its sourcing efforts

on smaller projects, which do not require surety bonding. The Company purports that these

smaller projects will carry higher margins, though this is contrary to the feedback we have

received from the marketplace, which indicated that there is a greater degree of

competition for smaller assignments. Additionally, selling expense should increase given

smaller project size and constant selling expense per project. On the other hand, an increase

in gross margin may be achieved because IES can more accurately bid on and properly execute

smaller scale projects.

The Company has also mentioned its intention to obtain a secondary surety provider. We

consider success with this endeavor unlikely and believe that Chubb will continue to secure

the balance of its unsecured exposure and reduce its outstanding bonds. We also believe

that Chubb will continue to work with IES management in a fiscally prudent manner.

Abandoning IES’s surety bonding program would limit the Company’s ability to win future

business and potentially harm Chubb’s current bonding exposure to IES if deteriorating sales

imperiled its ability to complete current projects.

Divestitures

In October 2004, IES announced a strategic realignment of all its business units. The

realignment is aimed at divesting underperforming commercial units and is expected to be

completed within fiscal 2005. Management has classified each of IES’s business units as either

Core, Under Review or Planned Divestiture. The Core category is comprised of the Company’s

residential units and well-performing commercial units. While subject to change, remaining

Planned Divestiture units accounted for an estimated $106 million of fiscal 2004 revenues and

approximately $55 million of LTM revenues through July 2005, a percentage decrease of 48%.

To-date, divested units are comprised of thirteen business units responsible for an estimated $244

million of fiscal 2004 revenues (see Figure 4). The vast majority of these units are

headquartered in the Southeast and Southwest regions. As of this writing, only two divestitures

7

8. had been announced in the fourth quarter of 2005, as compared with five that had been scheduled

to be completed by quarter-end.

Figure 4

Divestitures Fiscal Year-to-Date

(In Millions of Dollars)

Cash 2004 2004 Proceeds/

Business Unit State Proceeds Revenue Op. Margin Revenue Date

Goss Electrical AL $ 4.0 $ 19.0 -2.2% 0.21x 11/30/04

Delco Electric OK

7.5 38.7 3.9% 0.19x 12/10/04

B. Rice Electric TX

Ace/Putzel GA 3.5 17.3 -2.8% 0.20x 01/07/05

DKD Electric NM

4.4 27.3 2.2% 0.16x 02/01/05

Howard Brothers Electric NC

T&H Electric NC 4.5 16.5 9.1% 0.27x 03/02/05

Canova Electrical PA 1.7 8.0 11.3% 0.21x 04/18/05

Anderson & Wood ID

3.2 13.3 4.5% 0.24x 05/04/05

Tech Electric NC

Ernest P. Breaux Electrical LA 5.6 49.3 4.3% 0.11x 06/30/05

Brink Electric Construction SD 4.7 19.3 10.3% 0.24x 08/05/05

Florida Industrial Electric * FL 6.0 35.5 -0.8% 0.17x 09/05/05

Subtotal 44.9

Adjustment to Subtotal 1.9

Cash True-Up 3.1

TOTAL $ 49.9 $ 244.2 0.20x

Source: Company Reports and MTR.

* Revenue figure reflected is for LTM ending August 2005.

Cash proceeds for the Company’s current divestiture Figure 5

program total $50 million, and given average cash proceeds Divestiture Summary

As of September 5, 2005

of $0.20 per fiscal 2004 revenue dollar (as compared with an (In Millions of Dollars)

estimated $0.75 per revenue dollar paid for IES’s founding

No. Cash Est LTM

companies), the balance of Planned Divestitures could Status Units Proceeds Revenue

generate an incremental $28 million, assuming that those Sold 13 $ 48.0 $ 244.2

Closed 2 - 9.3

already divested units were not low-hanging fruit. An Planned 4 28.1 140.7

additional three units are classified as Under Review ($196 Under Review 3 39.2 195.8

Source: Company Reports and MTR.

million of 2004 revenues) and could produce estimated cash * Cash proceeds for Planned and Under Review are estimated.

proceeds of $39 million, though based on comments made on

the fiscal third quarter 2005 conference call, we assume that these units will be retained in the

medium-term. In what we believe to be every case, each divested unit has been sold to its

previous owner/current manager. This implies that 1) the previous owner believes that she

can create value once disassociated from IES; 2) the unit’s projects can get bonded when

separated from IES (possibly via owner personal guarantees); 3) the buyer of the divested unit

perceives that she is buying at a level at which she can make an acceptable return; and 4) there

does not exist another buyer for the unit. This also clearly demonstrates that IES has the

ability to readily divest its structurally disparate units and to generate incremental

liquidity.

As for what IES will do with the cash proceeds of its divestiture program, we believe that it

will not readily use recent proceeds to repurchase debt, as it is not required under its

indentures given the size of asset sales. With backlog declining, uncertainty surrounding future

8

9. commercial project awards and declining operating margins, we suspect that the Company will

likely wait and see if it requires the cash proceeds to support operations.

MACRO DRIVERS

Demand for commercial and industrial electrical contracting services is driven by construction

and renovation activity, which is highly correlated to growth in real gross domestic product and

to the rate of unemployment. Electrical contracting will lag a construction trend, as it is put-in-

place during the latter part of the project. As shown in the Figure 6, our correlation analysis

produced an R2 (statistical measure, 100% signifies perfect correlation) of 99.5%, showing an

extremely high correlation among real GDP, the rate of unemployment and fixed investment in

nonresidential construction spending.

Figure 6 Figure 7

Nonresidential Correlation Analysis Residential Correlation Analysis

(In Billions of Dollars) (In Billions of Dollars)

Nonresidential Home New

Unemploy. Fixed Mortgage Housing

Year Real GDP Rate Investment Year Real GDP Yields Investment

1995 $ 8,031.7 5.59% $ 762.5 1995 $ 8,031.7 7.87% $ 171.4

1996 8,328.9 5.41% 833.6 1996 8,328.9 7.80% 191.1

1997 8,703.5 4.94% 934.2 1997 8,703.5 7.71% 198.1

1998 9,066.9 4.51% 1,037.8 1998 9,066.9 7.07% 224.0

1999 9,470.3 4.23% 1,133.3 1999 9,470.3 7.04% 251.3

2000 9,817.0 4.02% 1,232.1 2000 9,817.0 7.52% 265.0

2001 9,890.7 4.79% 1,180.5 2001 9,890.7 7.00% 279.4

2002 10,074.8 5.80% 1,075.6 2002 10,074.8 6.43% 298.8

2003 10,381.3 6.00% 1,110.8 2003 10,381.3 5.80% 345.7

2004 10,841.9 5.50% 1,228.6 2004 10,841.9 5.77% 416.1

Variables Variables

Y Real Nonresidential Fixed Investment Y Real New Housing Investment

X1 Real GDP X1 Real GDP

X2 Unemployment Rate X2 Home Mortgage Yields

Output Output

2 2

R = 99.5% R = 95.0%

Y= 0.1668 * X1 - 10610.8 * X2 + 13.46175 Y= 0.05077 * X1 - 3756.68 * X2 + 46.7746

Source: Department of Commerce and MTR analysis. Source: Department of Commerce and MTR analysis.

Demand for residential electrical contracting services is correlated to housing starts and is, in

large part, driven by the health of the economy and the level of interest rates. With new housing

investment as the dependent variable and an R2 of 95.0%, the regression analysis in Figure 7

clearly shows a very strong relationship among the three.

CORPORATE STRUCTURE

Figure 8

INTEGRATED ELECTRICAL SERVICES, INC.

(Holding Company)

Revolving Credit Facility

6.5% Senior Convertible Notes

9.375% Senior Subordinated Notes

Operating Subsidiaries

Revolving Credit Facility

Guarantors of:

6.5% Senior Convertible Notes

9.375% Senior Subordinated Notes

Source: Company reports.

9

10. CAPITAL STRUCTURE

IES is structured as a holding company with substantially all of its assets and operations held by

its subsidiaries. Each of the Company’s notes has been issued by the holding company entity,

while both the parent and its operating subsidiaries are co-borrowers on the bank facility.

Revolving Credit Facility

On August 1, 2005, IES obtained a new three-year $80 million revolving credit facility with

Bank of America, N.A., replacing its old facility which was scheduled to mature on August 31,

2005. As of August 9, 2005, there were no cash borrowings under the facility. Net of $15

million of reserves and $47 million of outstanding LC’s, revolver availability was $18 million.

A Back-Up Letter of Credit in the amount of $42.1 million has been issued to secure the letters

of credit that had been issued under the previous facility; in addition, a $5.0 million letter of

credit has been issued to Chubb as additional security for its surety obligations. The letters of

credit issued collateralize $36 million in casualty insurance and $11.4 million in surety bonding.

The Company and each of its operating subsidiaries are co-borrowers of the facility; all other

subsidiaries are guarantors of the facility. The obligations of the borrowers and the guarantors

are secured by a pledge of substantially all of the assets of the Company and its subsidiaries,

excluding any assets pledged to secure surety bonds procured by the Company and its

subsidiaries in connection with their operations. The facility also carries a $70 million Letter of

Credit sub-facility.

Outstanding borrowings are charged an interest rate equal to 1) LIBOR plus an applicable margin

ranging from 2.5% to 3.5%, based upon the Fixed Charge Coverage ratio, or 2) a domestic bank

rate plus an applicable margin ranging from 0.5% to 1.5%, based upon the Fixed Charge

Coverage ratio, at the election of the borrower. Fixed Charges are defined as interest expense,

capital expenditures, principal payments of debt, depreciation associated with equipment, and

income taxes.

The facility’s Borrowing Base is calculated as a percentage of Eligible Accounts Receivable,

Inventory and Equipment, less a reserve of $15 million. Borrowings against accounts receivable

are determined as an amount equal to the lesser of 85% Eligible Accounts Receivable and 80%

of cash collections; against inventory, as an amount equal to the lesser of $10 million and the

lesser of (a) 65% of Eligible Inventory and (b) 85% of Eligible Inventory Liquidation Value; and

against equipment, as an amount equal to the lower of cost or market.

The loan agreement contains a covenant that specifies a Fixed Charge Coverage ratio for each

cumulative monthly period (starting at one month and increasing up to a trailing twelve months),

commencing in July 2005 at 0.59, scaling in a non-linear fashion to 1.00 in May 2007. We

project covenant default during the first quarter of fiscal 2006, ending December 31, 2005,

and believe that the bank will issue a waiver; our calculation of this ratio is not certain

given current guidance. In addition to customary events of default, the facility is cross-

defaulted to the Senior Convertible Notes, the Senior Subordinated Notes and the Company’s

agreement with Chubb.

6.5% Senior Convertible Notes

On November 24, 2004, IES sold Series A and B Senior Convertible Notes due November 1,

2014 in the amount of $30 million and $6 million, respectively, followed by a $14 million Series

B issue on February 24, 2005. The capital raise was conducted in two parts to comply with the

$30 million basket provision under the Limitation on Indebtedness covenant in the Subordinated

10

11. Note indenture. The proceeds from the sale were used to repay a portion of the Company’s old

credit facility and for corporate purposes. The Convertible Notes bear interest at an annual rate

of 6.5%, payable semiannually on May 1 and November 1, and are convertible into common

shares at an initial conversion price of $3.25 per share.

The Convertible Notes are senior unsecured obligations and are guaranteed on a senior

unsecured basis by the Company’s significant domestic subsidiaries. Prior to March 1, 2006, the

Series B Convertible Notes are not convertible as long as any Series A Convertible Notes are

issued and outstanding. On or after November 1, 2008, the Company has the option to redeem

the Convertible Notes if the last reported trading price of the Common Stock is greater than

150% of the then current conversion price for at least 20 trading days in the 30 consecutive

trading days ending on the day prior to the date on which the Company delivers notice of

redemption. Upon a Change of Control, defined, in part, as the purchase of more than 50% of

the Voting Stock, the Company is required to repurchase the Convertible Notes at par plus

accrued interest. The holder of Notes who converts her securities during the Fundamental

Change Conversion Period is entitled to the Make-Whole Premium upon conversion. As of June

30, 2005, $50 million of Senior Convertible Notes were outstanding.

9.375% Senior Subordinated Notes

On January 25, 1999 and May 29, 2001, IES issued $150.0 million and $125.0 million of Series

B and C Senior Subordinated Notes due February 1, 2009. Proceeds from the Series B issuance

were used to finance acquisitions, while those of the Series C issuance were used to repay

amounts outstanding under the credit facility. The notes bear interest at 9.375%, payable

semiannually on February 1 and August 1.

The Subordinated Notes are unsecured and subordinated to all existing and future senior

indebtedness, including the Senior Convertible Notes. They are guaranteed on a senior

subordinated basis by all of IES’s subsidiaries. Post-default distributions, including those made

at exit from bankruptcy, are to be paid to holders of senior indebtedness until they are made

whole (including pre- and post-petition interest). However, the indenture contains a so-called “X

Clause.” This X Clause, in theory, entitles holders of the Subordinated Notes to retain

distributions consisting of “Permitted Junior Securities,” even if senior creditors haven’t been

made whole. Permitted Junior Securities are defined as “capital stock of the Company or debt

securities that are subordinated to all Senior Indebtedness to at least the same extent as the Notes

are subordinated to all Senior Indebtedness.” X Clauses are not particularly powerful protections

for holders of subordinated debt. First, they don’t require debtors to structure bankruptcy

distributions to include Permitted Junior Securities, and, second, courts have been very reluctant

to actually enforce them, when to do so would permit a substantial recovery to junior

bondholders before senior bondholders are made whole. While we are aware of recent efforts to

draft X Clauses to compel a more favorable judicial interpretation, the X Clause in question

doesn’t have such strengthened language. The Subordinated Notes are callable on or after

February 1, 2005 at $103.125, February 1, 2006 at $101.563 and February 1, 2007 at $100. The

notes carry a change of control put at 101%.

Under the definition of Permitted Indebtedness, the Subordinated Note indenture allows the

Company to borrow up to $250 million under a credit facility, as compared with its current

facility of $80 million. We calculate that, given its estimated eligible trade accounts

receivable balance alone, IES working capital accounts should support at least an

additional $50 million in senior credit. This, of course, assumes lender willingness, which

11

12. should not be taken for granted given the potential speed with which receivables become

uncollectible on non-performing construction projects and/or the property of the surety

provider via its subrogation rights. Otherwise, the Company’s ability to incur indebtedness is

limited through a Consolidated Fixed Charge Coverage ratio of at least 2.0, pro forma for the

acquired indebtedness, with which it is clearly not in compliance. Fixed Charges are defined as

interest expense and dividends paid or accrued on Redeemable Capital Stock or Preferred Stock.

Pursuant to the indenture, net cash proceeds from asset sales that are not used to reduce senior

indebtedness or to reinvest in assets that are useful in the business within 360 days of the asset

sale, and which are equal to or exceed $10 million, are to be used to purchase the Subordinated

Notes for cash at 100% of the principal amount plus accrued and unpaid interest to the purchase

date. Noncompliance with this provision of the indenture is not an Event of Default. Given the

sale price (averaging $3.4 million) of the divestitures completed year-to-date and of those

currently planned, it would appear that this provision is not applicable to IES’s current

strategic realignment.

The Company redeemed two tranches of Subordinated Notes in the amount of $27.1 million and

$75.0 million on September 30, 2002 and September 30, 2004, respectively. As of June 30,

2005, $62.9 million of the Series B Notes and $110 million of the Series C Notes were

outstanding.

Leverage / Liquidity

Figure 9

IES had total net debt of $192.4 million as of June 30, 2005. Leverage

Given an LTM adjusted EBITDA (defined as operating As of June 30, 2005

(In Millions of Dollars)

income before depreciation and amortization, net of MTR-

Leverage

determined non-recurring items) of $8.9 million, the Amt. O/S Thru

Revolving Credit Facility $ - 0.0x

Company had a net leverage ratio of 21.6x. LTM adjusted Senior Convertible Notes 50.0 5.6x

net interest coverage is calculated at 0.36x for the period. Senior Subordinated Notes

Total

172.9

222.9

25.1x

25.1x

As of August 9, 2005, IES had liquidity in the amount of $53

LTM Adjusted EBITDA $ 8.9

million, comprised of $35 million in cash and $18 million of Source: MTR analysis.

revolver availability.

MANAGEMENT / OWNERSHIP

C. Byron Snyder, Founder of IES and Chairman of the Board Figure 10

Beneficial Ownership

since the Company’s inception in 1997, replaced H. Roddy of IES Common Stock

Allen as president and CEO effective June 30, 2005. On June As of May 13, 2005

(Shares In Millions)

2, 2005, Mr. Allen announced that he had retired as president,

Owner No. Shares % Class

CEO and a director of IES. Mr. Allen had been a director since Marathon Asset 7.7 17.9%

2001, and CEO and president since October 2002. Throughout Amulet Limited

Fidelity

7.7

4.7

16.4%

12.1%

his career, Mr. Snyder has held leadership roles at both private Directors and Off., other 3.9 10.1%

Jeffrey Gendell 3.7 9.4%

equity firms and operating companies. As reported in the Barclays Global Investors 3.5 9.0%

Dimensional Fund 3.2 8.1%

Company’s latest proxy statement, Mr. Snyder beneficially State Street Research 2.8 7.0%

owns 6.4% of IES common stock (see Figure 10). Our C.ByronPartners Artisan

Snyder 2.6

2.2

6.7%

5.6%

feedback from the marketplace has been positive regarding Mr. Ardsley Advisory

Source: Company reports.

2.0 5.1%

Snyder. Those who purport to know him well consider him an

accomplished dealmaker and an astute business person. We view his assumption of the CEO

role as positive for IES, but telling of its current state of affairs.

12

13. Richard Humphrey was named COO of IES on March 31, 2005, replacing Richard China, who

left the Company in November 2004. Mr. Humphrey has 35 years of experience in the industry,

beginning in 1970 when he founded ARC Electric, Inc., currently a subsidiary of IES. Mr.

Humphrey remained as president of ARC until 2001, when he assumed the role of regional

operating officer.

David Miller was appointed CFO of IES in January 2005. Mr. Miller has been with the

Company since January 1998 and was previously chief accounting officer. He replaced William

Reynolds, who had been CFO since June 2000.

Bob Callahan was promoted to senior vice president of human resources in February 2005,

replacing Margery Harris, who had been with IES since October 2000. Mr. Callahan has been

with the Company since 2001.

COMPETITION

Based on data from F.W. Dodge and EC&M Magazine, IES management estimates that the

electrical contracting industry generated $90 billion in annual revenues for 2004. The industry is

highly fragmented and is comprised of over 70,000 companies, most of which are owner-

operated. Within the top 10 companies, as ranked by size, electrical contracting revenues range

from approximately $1.5 billion down to $300 million; of these, four companies are public (see

Figure 11).

Figure 11

Specialty Contractors - Public Comparables

As of August 31, 2005

(In Millions of Dollars)

LTM LTM EBITDA Enterprise EV / EV / Net Debt /

Company Ticker Specialty Sales EBITDA Margin Net Debt Value EBITDA Sales EBITDA

Integrated Electrical Services IES Electrical $ 1,169.4 $ 8.9 0.8% $ 192.4 $ 299.7 33.8x 0.26x 21.7x

EMCOR Group EME Elec. / Mechanical 4,719.1 83.7 1.8% 1.5 857.8 10.3x 0.18x 0.0x

EMCOR Group, US Electrical Division* Electrical 1,233.2 74.9 6.1%

Quanta Services PWR Electrical / Utilities 1,694.1 83.3 4.9% 220.2 1,623.8 19.5x 0.96x 2.6x

InfraSource Services IFS Utilities / Electrical 775.0 54.5 7.0% 99.3 690.3 12.7x 0.89x 1.8x

Comfort Systems USA FIX Mechanical / HVAC 869.6 28.4 3.3% (26.2) 299.9 10.5x 0.34x 0.0x

Dycom Industries DY Utilities / Comm. 996.1 130.6 13.1% (67.6) 797.9 6.1x 0.80x 0.0x

Source: Company Reports and MTR analysis.

* Estimated.

EMCOR Group (EME). Headquartered in Norwalk, CT, EMCOR Group has an interesting

history with predecessor entities that have focused on supplying water for municipalities and on

computer systems reselling. Formerly known as JWP, EMCOR emerged from bankruptcy in

1994 to concentrate on its core mechanical and electrical contracting businesses. Since then, it

has grown successfully through acquisition. Its installed systems are used for power generation

and distribution, lighting, communications, plumbing and HVAC. LTM electrical contracting

revenues are $1.2 billion with estimated EBITDA margins of 6.1%. The company had net debt

of $1.5 million as of June 30, 2005.

Quanta Services (PWR). Quanta Services, which is headquartered out of Houston, TX, is a

leading national provider of network infrastructure solutions to the electric power, gas,

telecommunications and cable television industries. Quanta recently posted total LTM sales of

$1.7 billion with an EBITDA margin of 4.9%. Its net leverage ratio, as of June 30, 2005, was

2.6x.

13

14. InfraSource Services (IFS). InfraSource Services, located in Media, PA, provides transmission

and distribution services to electric and gas utilities throughout the U.S. In 2003, the company

was sold off by its parent, Exelon (a subsidiary of the utility PECO), to GFI Energy Ventures and

Oaktree Capital Management, and it was subsequently taken public in 2004. LTM sales for the

period ending June 30, 2005 were $775 million, with an EBITDA margin of 7.0%. The

company’s net leverage ratio was 1.8x.

Other large, private competitors include Rosendin Electric, Fisk Corp., Xcelecom Inc., Morrow-

Meadows Corp., Red Simpson Inc., ANECO Electrical Construction and Miller Electric.

The following paragraph recounts the cautionary tale of Encompass Services, a now defunct roll-

up, which not too long ago, was the largest electrical contracting business in the United States.

Encompass Services. Encompass Services began with Figure 12

the formation of Group Maintenance America Corp. Encompass Services

(GroupMAC). Established to consolidate the electrical Financial Comparison

(In Millions of Dollars)

contracting industry, GroupMAC went public in 1997.

Following a number of add-on acquisitions, GroupMAC Encompass IES

3Q02 3Q05

merged with Building One to create the country’s largest Revenues 838.6 284.0

facilities services conglomerate. Crushed by its heavy Adjusted EBITDA 15.7 3.4

Adjusted EBITDA Margin 1.9% 1.2%

debt load and the economic recession of the early 2000’s, Interest Expense, net 19.6 7.6

Encompass filed for bankruptcy protection in 2002. The Net Debt 1,088.6 192.5

LTM Net Interest Coverage 1.1x 0.36x

firm’s decline is recounted well in its Disclosure Net Leverage Ratio 12.7x 21.7x

Statement dated April 11, 2003: following a disappointing Backlog 1,300.0 383.0

Months Backlog 4.7 5.8

second quarter of 2002, “Encompass’s customers Liquidity 76.8 44.1

increasingly began to demand bid and performance Source: Company reports and MTR estimates.

bonds for new and existing construction contracts. In early October, Encompass began

experiencing increased difficulty securing new construction contracts and bid and

performance bonds for its commercial activity. In addition, Encompass's sureties began

notifying Encompass of new and increased collateral requirements, based upon their concern

for Encompass's creditworthiness, demanding that Encompass and its Subsidiaries post letters of

credit in order to obtain the necessary bonding, which further exacerbated Encompass's

liquidity problems…In light of Encompass's announced financial difficulties, customers for

existing projects increasingly requested bonds, or requested increased coverage amounts of

bonds, on continuing projects, and threatened to terminate Encompass from such projects if

such requests were not satisfied. Bonding requirements for new projects significantly increased

in frequency, and Encompass was entirely excluded from bidding on a number of projects.

Encompass's sureties imposed increasingly stringent requirements to the issuance of bonds,

including requiring full cash collateral for the face amount of new bonds issued.” Subsequently,

in October 2002, Encompass submitted a prepackaged plan of reorganization, which was later

rejected. Ultimately, the company’s business units were sold.

One of the more notable sales was Encompass’s Residential Services Group (“RSG”). With

annual revenues of approximately $300 million, RSG provided HVAC, plumbing and other

contracting services in residential and small commercial buildings. Acquired by Wellspring

Capital Management, RSG was purchased for approximately $50 million, or 2.25x estimated

EBITDA. Wellspring Capital sold RSG fifteen months later to Direct Energy for $150 million,

or 6.25x EBITDA.

14

15. RECENT FINANCIAL RESULTS

Commercial and Industrial Segment Figure 13

Commercial and industrial revenues

Commercial and Industrial Segment

decreased 13.6% to $197.7 million in Cost Structure

the third quarter of fiscal 2005 ending 105.0%

Percentage of Revenues

June 30, 2005, down from $228.9 100.0%

million in the prior year’s quarter. The 95.0%

decrease is a result of decreased awards 90.0%

of bonded projects, the closure of plant 85.0%

and utility work at one subsidiary, and 80.0%

Q4 '03 Q1 '04 Q2 '04 Q3 '04 Q4 '04 Q1 '05 Q2 '05 Q3 '05

more selective bidding. Adjusted gross

margins for the third quarter of 2005 Adjusted Cost of Services as % Revenue Adjusted SG&A as % Revenue

remained relatively flat at 9.9% on a Source: Company and MTR estimates.

year-over-year basis, improving from 8.3% in the prior quarter; unadjusted gross margin

declined due to decreased awards of bonded projects and reduced job profitability at certain

subsidiaries. SG&A expense in the third quarter of 2005 continued to rise despite business unit

divestitures, increasing to $19.1 million, or 9.6% of segment revenue. As a result, adjusted

EBITDA margin for the commercial and industrial segment decreased to 1.1% for the third

quarter of 2005 from 3.1% in the prior year’s quarter (see Figure 16).

Residential Segment Figure 14

Residential revenues increased

4.8% in the third quarter of Residential Segment Cost Structure

2005 to $86.3 million from 100.0%

$82.3 million in the prior year’s

Percentage of Revenues

95.0%

quarter due primarily to the

90.0%

increased demand for new

85.0%

single-family and multi-family

80.0%

housing. Gross margins

75.0%

increased to 22.1% in the

70.0%

quarter versus 21.4% and Q4 '03 Q1 '04 Q2 '04 Q3 '04 Q4 '04 Q1 '05 Q2 '05 Q3 '05

17.5% for the second quarter of

Adjusted Cost of Services as % Revenue Adjusted SG&A as % Revenue

2005 and the third quarter of

2004, respectively. SG&A Source: Company and MTR estimates

expense in the third quarter of 2005 rose 11.8% year-over-year to $9.8 million, or 11.3% as a

percentage of revenues, versus 10.6% in the prior year’s quarter. Adjusted EBITDA margin

increased to 11.1% in the third quarter of 2005, as compared with 9.1% in the second quarter of

2005 and 7.2% in the third quarter of 2004. Excluding corporate overhead, IES’s residential

segment accounted for 81.4% of total operating segment adjusted EBITDA while

comprising just 30.4% of total revenues.

Corporate

Adjusted SG&A increased 57% in the third quarter of 2005 to $8.8 million, or 3.1% of total

revenue, from $5.6 million in the prior quarter. The increase was due to costs associated with an

incentive program, consulting fees associated with Sarbanes-Oxley compliance, and increased

audit fees. Total adjusted EBITDA was basically flat, sequentially, in the third quarter of 2005

at $3.4 million, but down 53% from $7.2 million in the third quarter of 2004.

15

16. Backlog Figure 15

Backlog for the third quarter of 2005 Backlog

decreased 32% to $383 million from $566 (In Millions of Dollars)

million in the prior year’s quarter, 3Q05 2Q05 ** Q/Q 3Q04 Y/Y

representing 5.8 months of backlog versus Backlog 383 435 -12% 566 -32%

Months Backlog * 5.8 6.0 -0.2 7.4 -1.6

7.4 months in the prior year (calculated on Backlog as % Ann. C&I Rev.* 48.4% 50.3% -190bps 61.8% -1,340bps

Source: Company Reports

annualized quarterly commercial and * Figures calculated using annualized quarterly C&I revenue.

** Revenue figures for 2Q05 used in calculations have not been adjusted for subsequent divestitures.

industrial segment revenues).

Cash Flow

Cash flow from operations before working capital in Q3 2005 was $0.3 million, as compared

with -$5.9 million in the prior quarter, due to semiannual cash interest payments. Since the third

quarter of 2004, average quarterly trailing twelve-month cash flow from operations has averaged

-$1.6 million. Over the past three quarters, asset sales have supplemented cash from operations

with $36.2 million of cash flow, some of which was used to reduce debt levels (see Figure 16).

16

18. Figure 17

INTEGRATED ELECTRICAL SERVICES, INC.

Historical Quarterly Cash Flow Summary *

(In Millions of Dollars)

Q4 Q1 Q2 Q3 Q4 ** Q1 Q2 Q3

SOURCES 9/30/03 12/31/03 3/31/04 6/30/04 9/30/04 12/31/04 3/31/05 6/30/05

Adjusted EBITDA $ 18.6 $ 15.7 $ 7.5 $ 7.2 $ (0.5) $ 2.4 $ 3.5 $ 3.4

Non-Cash Comp. Expense - 0.1 0.2 0.2 0.2 0.2 0.4 0.4

Total Sources 18.6 15.8 7.7 7.4 (0.3) 2.6 4.0 3.8

USES

Cash Interest Expense (11.7) (0.2) (13.3) (0.7) (9.2) (1.1) (8.7) (1.4)

Cash Income Taxes - (0.4) (0.3) (0.3) 0.1 (0.3) (0.4) (0.1)

Capital Expenditures (1.4) (1.6) (1.3) (1.4) (2.3) (1.2) (1.0) (1.3)

Working Capital Changes (16.8) 0.4 (1.5) (0.8) 3.9 (5.1) 9.0 4.1

Change in Noncurrents (2.9) 0.3 2.9 (1.3) (1.1) (0.4) 0.2 (0.6)

Total Uses (32.9) (1.4) (13.4) (4.6) (8.6) (8.1) (0.9) 0.6

Adjusted Free Cash Flow $ (14.3) $ 14.3 $ (5.7) $ 2.8 $ (8.9) $ (5.4) $ 3.1 $ 4.4

Asset Sales - - - - - 11.7 12.4 12.1

Net Changes in Debt (0.1) (0.1) (25.1) (7.1) 15.0 10.3 (15.9) (2.4)

Net Change in Cash $ (14.3) $ 14.2 $ (30.8) $ (4.3) $ 6.1 $ 16.6 $ (0.5) $ 14.1

Cash Balance 40.2 44.2 19.0 13.3 22.2 31.7 32.4 31.5

Revolver Availability 97.6 95.0 91.3 99.2 41.3 38.7 33.4 12.6

Total 137.8 139.2 110.3 112.5 63.5 70.4 65.8 44.1

Source: Company and MTR estimates

* Quarterly figures exclude non-recurring items.

* Quarterly figures are not necessarily comparable due to divestitures and financial restatements.

** Q4 2004 figures do not incorporate adjustments for divestitures.

OUTLOOK

We are not bullish on IES’s prospects, but we do not consider its future to be determined at

this time. The loss of quality people at many of the Company’s business units and the

dependency of future growth on the state of the Company’s current financial health pose

significant challenges. Aside from unforeseen factors, it appears that management may have

time to affect a turnaround, given the Company’s limited capital requirements and its ability to

sell units to generate liquidity.

Markets

The U.S. commercial construction market has experienced a significant decline since its peak in

2000. Having been revised downward, forecasted commercial construction spending is projected

to grow 3% in 2005 by F.W. Dodge, which is a far cry from initial projections upwards of 10%.

While this forecast is certainly better than a market contraction, marketplace demand

must accelerate to utilize unabsorbed capacity so that incremental utilization drives IES

top-line growth and improved project margins. Industry sources have commented that the

overall construction industry has improved over the past few months.

18

19. According to the National Association of Home Builders, the U.S residential construction

market, as measured by new housing starts, grew by 5.8% in 2004. As of August 10, 2005, the

NAHB forecasts the market to peak in 2005 with 2.0 million starts (a record year), or 3.3%

annual growth, declining to 1.9 million starts in 2006. These forecasts bode well for IES’s

residential operating segment, which should continue to show a strong top line and

operating margin.

Financial Projections

Our projections reflect our concern with the difficulties facing IES management in turning

around its Commercial and Industrial operating segment. Specifically, we are concerned about

IES’s declining backlog, high leverage, a difficult surety bonding environment, markets

which have yet to rebound and the loss of quality people within the organization. The

model’s drivers are intended to portray a degrading fundamental picture at the Company’s

Commercial and Industrial segment, and a resulting decrease in liquidity.

Commercial and Industrial. We project C&I segment revenue will decrease 2.5% sequentially

for the quarters ending September 30, 2005 and December 31, 2005, accelerating to 4.0%,

thereafter, through the end of fiscal 2007. We have accelerated the decline in revenue to reflect

anticipated backlog shrinkage; projected revenues are net of projected divestitures. Gross

margin for the segment is forecast at 9.5%, as compared with an adjusted gross margin of 9.9%

in Q3 2005 and an LTM adjusted gross margin of 8.8%. Based on some of the positive feedback

we have received from the marketplace concerning recent cost-cutting activity, we have assumed

that management successfully reduces annual SG&A by $500k each quarter, and thus have

projected SG&A to improve $125k quarterly. From a historical perspective, it is surprising that

given the recent divestiture of business units that had high SG&A expense relative to their

revenue base, segment SG&A as a percentage of segment revenues has only increased on a year-

over-year basis in each of the last four quarters. Our resulting projected C&I adjusted EBITDA

margin declines sequentially, averaging -0.5% over the next four quarters, or -$850k.

Figure 18

INTEGRATED ELECTRICAL SERVICES, INC.

Commercial and Industrial Segment

Projected Quarterly Operating Statement

(In Millions of Dollars)

4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07

Revenues $ 186.4 $ 172.3 $ 162.3 $ 155.8 $ 149.5 $ 143.6 $ 137.8 $ 132.3 $ 127.0

Cost of Services 168.7 155.9 146.8 141.0 135.3 129.9 124.7 119.7 114.9

SG&A Expense 18.9 18.8 18.6 18.5 18.4 18.3 18.1 18.0 17.9

Depreciation and Amortization (1.9) (1.8) (1.7) (1.7) (1.6) (1.6) (1.5) (1.5) (1.4)

Adjusted EBITDA 0.7 (0.6) (1.5) (2.0) (2.6) (3.1) (3.5) (4.0) (4.4)

Revenues, Q/Q % Change * -5.7% -7.6% -5.8% -4.0% -4.0% -4.0% -4.0% -4.0% -4.0%

As a % Revenues:

Cost of Services 90.5% 90.5% 90.5% 90.5% 90.5% 90.5% 90.5% 90.5% 90.5%

SG&A Expense 10.1% 10.9% 11.5% 11.9% 12.3% 12.7% 13.2% 13.6% 14.1%

Depreciation and Amortization -1.0% -1.0% -1.1% -1.1% -1.1% -1.1% -1.1% -1.1% -1.1%

Adjusted EBITDA 0.4% -0.3% -0.9% -1.3% -1.7% -2.1% -2.6% -3.0% -3.5%

Source: MTR projections.

* Percentage change in 4Q05, 1Q06 and 2Q06 reflects divestitures.

19

20. Residential. Residential segment revenue, on a year-over-year basis, is projected to increase

4.5% in the fourth quarter of 2005, remain flat through fiscal 2006 and decline by 2.5% in fiscal

2007, in-line with a slowing housing market. Gross margins are expected to remain strong,

ranging between 21% and 22% through fiscal 2007. Segment SG&A is projected to be flat at

$9.6 million, given our limited visibility. Resulting projected Residential adjusted EBITDA

margin varies between 7.2% and 11.5% through fiscal 2007, primarily due to seasonality.

Figure 19

INTEGRATED ELECTRICAL SERVICES, INC.

Residential Segment

Projected Quarterly Operating Statement

(In Millions of Dollars)

4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07

Revenues $ 85.2 $ 69.7 $ 71.4 $ 86.3 $ 85.2 $ 67.9 $ 69.6 $ 84.1 $ 83.1

Cost of Services 66.0 55.0 56.4 67.3 66.4 53.7 55.0 65.6 64.8

SG&A Expense 9.6 9.6 9.6 9.6 9.6 9.6 9.6 9.6 9.6

Depreciation and Amortization (0.2) (0.2) (0.2) (0.2) (0.2) (0.2) (0.2) (0.2) (0.2)

Adjusted EBITDA 9.8 5.3 5.6 9.6 9.3 4.9 5.2 9.1 8.9

Revenues, Y/Y % Change 4.5% 0.0% 0.0% 0.0% 0.0% -2.5% -2.5% -2.5% -2.5%

As a % Revenues:

Cost of Services 77.5% 79.0% 79.0% 78.0% 78.0% 79.0% 79.0% 78.0% 78.0%

SG&A Expense 11.3% 13.8% 13.4% 11.1% 11.3% 14.1% 13.8% 11.4% 11.6%

Depreciation and Amortization -0.3% -0.3% -0.3% -0.2% -0.2% -0.3% -0.3% -0.2% -0.2%

Adjusted EBITDA 11.5% 7.5% 7.9% 11.1% 11.0% 7.2% 7.5% 10.8% 10.7%

Source: MTR projections.

Projected Cash Flow / Liquidity

Given our view of cash burn in the foreseeable future, sufficient medium-term liquidity is

reliant upon successful asset sales. To-date, the Company has sold two business units in the

fourth quarter of 2005, generating $10.7 million in cash proceeds and a $2.0 million three-year

promissory note. Based upon information provided in the Company’s second quarter 10-Q, our

projections assume that three additional units are sold in the first quarter of 2006, producing

$21.1 million in proceeds (0.2x fiscal 2004 revenues) and one unit is sold in the second quarter

of 2006, producing $7.0 million in proceeds. On the last Company conference call, management

had guided that all asset sales should be completed in the current quarter.

Assuming no working capital contributions/requirements or cash income taxes, IES is

projected to maintain liquidity through the third quarter of fiscal 2007; without successful

asset sales, management is projected to have through fiscal 2006 to affect a turnaround.

We have assumed that the remaining revolver availability will be used to issue letters of credit to

collateralize additional surety bonding.

20

21. Figure 20

INTEGRATED ELECTRICAL SERVICES, INC.

Projected Quarterly Cash Flow Summary

(In Millions of Dollars)

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

SOURCES 9/30/05 12/31/05 3/31/06 6/30/06 9/30/06 12/31/06 3/31/07 6/30/07 9/30/07

Adjusted EBITDA

Commerical and Industrial $ 0.7 $ (0.6) $ (1.5) $ (2.0) $ (2.6) $ (3.1) $ (3.5) $ (4.0) $ (4.4)

Residential 9.8 5.3 5.6 9.6 9.3 4.9 5.2 9.1 8.9

Corporate SG&A (7.3) (7.3) (7.3) (7.3) (7.3) (7.3) (7.3) (7.3) (7.3)

Corporate Depreciation 0.5 0.5 0.5 0.5 0.5 0.4 0.4 0.4 0.4

Total Adjusted EBITDA 3.8 (2.1) (2.6) 0.8 (0.0) (5.0) (5.2) (1.7) (2.4)

Non-Cash Comp. Expense 0.4 0.4 0.4 0.4 0.4 0.4 0.4 0.4 0.4

Total Sources 4.1 (1.7) (2.3) 1.1 0.3 (4.7) (4.8) (1.4) (2.0)

USES

Cash Interest Expense (2.4) (8.8) (2.8) (9.3) (2.9) (9.3) (2.9) (9.3) (2.9)

Cash Income Taxes - - - - - - - - -

Capital Expenditures (1.3) (1.3) (1.3) (1.3) (1.3) (1.3) (1.3) (1.3) (1.3)

Working Capital Changes - - - - - - - - -

Change in Noncurrents - - - - - - - - -

Total Uses (3.7) (10.1) (4.0) (10.6) (4.2) (10.6) (4.2) (10.6) (4.2)

Adjusted Free Cash Flow $ 0.5 $ (11.8) $ (6.3) $ (9.4) $ (3.9) $ (15.2) $ (9.0) $ (11.9) $ (6.2)

Asset Sales, Completed 10.7 - - - 0.7 - - - 0.7

Asset Sales, Projected - 21.1 7.0 - - - - - -

Net Changes in Debt - - - - - - - - -

Net Change in Cash $ 11.1 $ 9.3 $ 0.7 $ (9.4) $ (3.2) $ (15.2) $ (9.0) $ (11.9) $ (5.6)

Beginning Cash Balance 31.5 42.6 52.0 52.7 43.3 40.0 24.8 15.8 3.9

Ending Cash Balance 42.6 52.0 52.7 43.3 40.0 24.8 15.8 3.9 (1.7)

Without Additional Asset Sales

Beginning Cash Balance 31.5 42.6 30.8 24.5 15.1 11.9 (3.4) (12.3) (24.3)

Ending Cash Balance 42.6 30.8 24.5 15.1 11.9 (3.4) (12.3) (24.3) (29.9)

Source: MTR projections.

RATING AGENCIES

On May 17, 2005, Moody’s downgraded IES’s Senior Implied rating to B3 from B2 and its

senior unsecured issuer rating to Caa2 from Caa1, changing its rating outlook to negative from

stable. The downgrade reflects the Company’s current negative cash flow generation, the lower-

than-expected reduction in debt balances via asset sales, its weak liquidity, and the difficulty the

Company is expected to encounter as it attempts to grow its core operations.

Standard and Poor’s, on May 19, 2005, announced that it placed IES’s corporate credit and

subordinated debt rating on CreditWatch with negative implications. S&P stated that the

CreditWatch placement reflects the Company’s weakened liquidity position following a credit

facility covenant violation.

21