Dietrich & Associates: Pension RIsk Transfer Index September 2011

•

0 likes•27 views

Monthly index that tracks the relative attractiveness of annuitizing accured pension obligations.

Recommended

Recommended

More Related Content

Similar to Dietrich & Associates: Pension RIsk Transfer Index September 2011

Similar to Dietrich & Associates: Pension RIsk Transfer Index September 2011 (20)

More from Jay Dinunzio

More from Jay Dinunzio (17)

Recently uploaded

Recently uploaded (20)

Dietrich & Associates: Pension RIsk Transfer Index September 2011

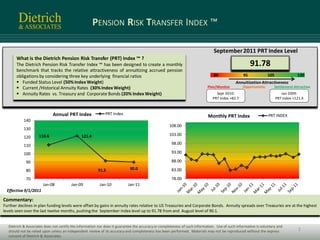

- 1. PENSION RISK TRANSFER INDEX ™ September 2011 PRT Index Level What is the Dietrich Pension Risk Transfer (PRT) Index ™ ? The Dietrich Pension Risk Transfer Index ™ has been designed to create a monthly 91.78 benchmark that tracks the relative attractiveness of annuitizing accrued pension obligations by considering three key underlying financial ratios 80 95 105 120 Funded Status Level (50% Index Weight) Annuitization Attractiveness Current /Historical Annuity Rates (30% Index Weight) Plan/Monitor Opportunistic Settlement Attractive Annuity Rates vs. Treasury and Corporate Bonds (20% Index Weight) Sept 2010: Jan 2009: PRT Index =82.7 PRT Index =121.4 Annual PRT Index PRT Index PRT INDEX Monthly PRT Index 140 108.00 130 110.6 121.4 103.00 120 110 98.00 100 93.00 90 88.00 80 91.5 90.0 83.00 70 78.00 Jan-08 Jan-09 Jan-10 Jan-11 Effective 9/1/2011 Commentary: Further declines in plan funding levels were offset by gains in annuity rates relative to US Treasuries and Corporate Bonds. Annuity spreads over Treasuries are at the highest levels seen over the last twelve months, pushing the September Index level up to 91.78 from and August level of 90.1. Dietrich & Associates does not certify the information nor does it guarantee the accuracy or completeness of such information. Use of such information is voluntary and should not be relied upon unless an independent review of its accuracy and completeness has been performed. Materials may not be reproduced without the express 1 consent of Dietrich & Associates.