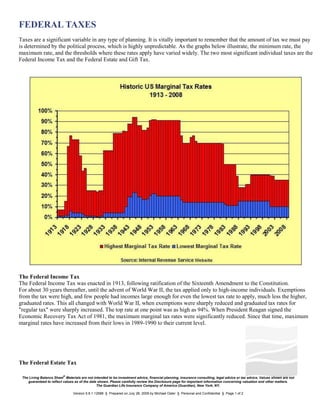

1. Federal Taxes Taxes are a significant variable in any type of planning. It is vitally important to remember that the amount of tax we must pay is determined by the political process, which is highly unpredictable. As the graphs below illustrate, the minimum rate, the maximum rate, and the thresholds where these rates apply have varied widely. The two most significant individual taxes are the Federal Income Tax and the Federal Estate and Gift Tax. The Federal Income TaxThe Federal Income Tax was enacted in 1913, following ratification of the Sixteenth Amendment to the Constitution.For about 30 years thereafter, until the advent of World War II, the tax applied only to high-income individuals. Exemptions from the tax were high, and few people had incomes large enough for even the lowest tax rate to apply, much less the higher, graduated rates. This all changed with World War II, when exemptions were sharply reduced and graduated tax rates for

regular tax

were sharply increased. The top rate at one point was as high as 94%. When President Reagan signed the Economic Recovery Tax Act of 1981, the maximum marginal tax rates were significantly reduced. Since that time, maximum marginal rates have increased from their lows in 1989-1990 to their current level. The Federal Estate TaxThe estate tax (also known as the death tax) is one of the most inefficient features of the current tax system. Once the headache of the wealthy, it now reaches well into middle-class America. Because the estate tax falls on assets, it reduces incentives to save and invest and, therefore, hampers growth. It also unfairly hits owners of small businesses, family farms, and savers who amass wealth through hard work and thrift. Financing worldwide conflict at the beginning of the 20th century motivated Congress in 1916 to pass the Revenue Act of 1916, which introduced the modern-day income tax and also contained an estate tax with many features of today's system. Even though it was enacted primarily to finance the war effort, the estate tax did not go away after the war ended. Despite sizable budget surpluses, Congress increased rates and introduced a gift tax in 1924. Like the estate tax, the gift tax is a levy on the transfer of property from one person to another. During the 1920s through the 1940s, estate taxes were used as another way to attempt to redistribute income. Tax rates of up to 77% on the largest estates were supposed to prevent wealth from becoming increasingly concentrated in the hands of a few. In 1976, in an effort to close loopholes, the Estate Tax and the Gift Tax were combined into a single, unified Federal Estate and Gift Tax. Source: Figures based upon information from the U.S. Treasury Department – Internal Revenue Service 2009