Download to read offline

![32

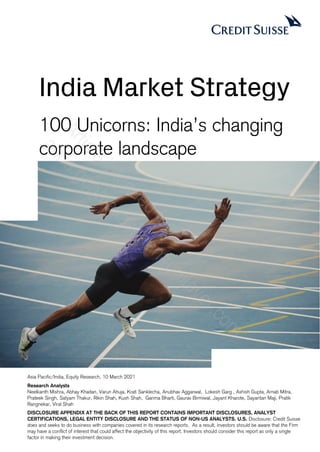

High unorganised contribution presents strong growth

prospects for online platforms

One of the key unique aspects of the India retail market is the

higher contribution from the unorganised sector especially in

the grocery space. The unorganised segment is more than

80% of the total Indian retail market while the same for

grocery is c.96%. Also, the online contribution in grocery is in

low single digit while in non-grocery the online contribution is

in the teens. We note that grocery’s share of the total retail

market was c.65% in 2020 increasing from c.60% in 2019.

With total retail market growth due to go back to 9-10% by

2021, we believe the e-commerce market size in India can be

c.US$100 bn by 2025, representing c.10% total retail sales.

Given massive growth opportunities in the grocery vertical, the

sector has seen the emergence of many vertical players—Big

Basket, Grofers, Nykaa, etc. Even established horizontal

companies, such as Flipkart and Amazon, are making increasing

investment in to the segment. The other key theme is hyperlocal

or modernisation of mom-and-pop stores so as to provide

inventory fulfilment and enabling them to do last mile delivery.

Reliance Industries is looking to play a big role in the segment.

We expect e-commerce to remain one of the largest sub-

segments of India’s internet sector due to the strong growth

prospects in organised Indian retail and, thus, support

emergence of more unicorns in the sector.

Figure 67: E-commerce’s contribution to FMCG sales has

inched up in 2020

Figure 68: And also has the share of online retail spend

for SBI cards

Source: Nielsen, Credit Suisse Source: SBI Cards, Credit Suisse

Figure 69: Unorganised segment is more than 80% of

the total Indian retail market…

Figure 70: …while the same for grocery is c.96%.

Source: Euromonitor, IBEF, Credit Suisse Source: Euromonitor, Credit Suisse

Figure 71: Online contribution in grocery is the lowest Figure 72: E-commerce market size in India can

potentially be c.US$100 bn by 2025

Source: Euromonitor, Credit Suisse Source: Euromonitor, BCG, Credit Suisse]

0

2

4

6

8

10

1QCY20 3QCY20

All India Metros

Vaue contribution of E-commerce to FMCG Sales

0%

10%

20%

30%

40%

50%

60%

FY17 FY18 FY19 FY20 1H21

Share of online retail spends

84%

9%

7%

Unorganised

Organised

e-commerce

Non-Grocery

34%

Traditional

96%

Modern

3%

Online

1%

Grocery

66%

17%

1%

7%

% online,

Grocery

% online,

Non-Grocery

% online,

Total retail

sales

42

101

0

200

400

600

800

1,000

1,200

2020 2025E

Offline Online

640

1,007

5-year

CAGR of

9.5%

Penetration

6.5%

Penetration

10.0%

US$ bn

A

r

t

i

c

l

e

i

n

t

e

n

d

e

d

f

o

r

:

a

s

h

a

.

g

o

p

a

l

a

k

r

i

s

h

n

a

n

#

u

n

i

l

e

v

e

r

.

c

o

m](https://image.slidesharecdn.com/indias100unicorns-210724041519/85/India-s-100-unicorns-32-320.jpg)

![India Market Strategy 127

Sri Chaitanya

Education Varun Ahuja, Krati Sanklecha

Reason for inclusion: Valuation >US$1 bn at latest EBITDA and multiple

Company profile

Sri Chaitanya Group is engaged in providing educational services. It operates under the name Sri Chaitanya Educational

Institutions. It provides coaching for entrance exams like Indian Institute of Technology joint entrance exam (IIT-JEE), pre-

medical test (PMT), chartered accountancy, Indian administrative service (IAS) exams, and the like. The group also operates

private schools, junior colleges, a] chartered accountancy academy and an Indian administrative service academy. The

company was founded in 1986 and is based in Hyderabad, Telangana.

Funding history

NA

Management profiles

Name Position Profile

Dr BS Rao Founder and Chairman A practicing doctor, Dr BS Rao opened the first school in 1986 with just one

branch of 56 students.

Sushma Bopanna Academic Director Mrs Sushma Bopanna completed her BTech from BITS Pilani and her master’s in

IT from US University.

Source: Company data

Figure 316: Number of universities growing at a CAGR of

8%

Figure 317: Education industry grew by 10% in India

Source: Company data, Credit Suisse Source: Company data, Credit Suisse

0

200

400

600

800

1,000

1,200

FY16 FY17 FY18 FY19

Number of Universities in India

0

20

40

60

80

100

FY18 FY19

Number of Universities in India

A

r

t

i

c

l

e

i

n

t

e

n

d

e

d

f

o

r

:

a

s

h

a

.

g

o

p

a

l

a

k

r

i

s

h

n

a

n

#

u

n

i

l

e

v

e

r

.

c

o

m](https://image.slidesharecdn.com/indias100unicorns-210724041519/85/India-s-100-unicorns-127-320.jpg)

![136

Vishal Mega Mart

Consumer Discretionary Arnab Mitra, Pratik Rangnekar

Reason for inclusion: Valuation <US$1 bn, but strong growth

Company profile

Founded by Mr Ram Chandra Agarwal in 1994, Vishal Mega Mart started off as a value retailer franchising out ~170 stores

across India mainly outside the metros. However, saddled with debt, the company was sold to TPG Private Equity and

Shriram Group for Rs700 mn in a fire sale. In 2018, the company changed hands again with Kedaara Capital and Global

investment firm Partners Group acquiring it. The network has grown to 375 franchised stores across 241 cities mainly in

north, south and east of India with an area of 6.4 mn sq ft. Its presence in under-penetrated markets and a value positioning

have driven a 35% CAGR over the last three years with a wide offering of private label fast fashion and other general

merchandise and grocery.

Funding history

Vishal Mega Mart was sold to TPG Private Equity and Shriram Group for Rs700 mn in a fire sale. In 2018, the company

changed hands again with Kedaara Capital and global investment firm, Partners Group, acquiring it for a deal reported in

media at ~US$700 mn (source: Mint).

Figure 339: Kedaara Capital and Partners Group acquired Vishal from TPG capital in 2018

Source: Factset

Management profile

Name Position Profile

Gunendar Kapoor CEO Has been the CEO since TPG took over and has overseen a turnaround in the

company. Prior to this he has been a veteran in Unilever/HUL for 12 years and

thereafter was the CEO at Reliance Retail for c.4 years.

Source: Company data

Figure 340: Revenues have grown at a 16% CAGR over

FY15-19

Figure 341: PAT margin has expanded sharply as well

(EBITDA = US$ mn]

Source: Company data, Euromonitor Credit Suisse Source: Company data, Credit Suisse

TPG Capital purchased in

slump sale

Kedaara Capital and

Partners Group

0

400

800

1,200

0

1

1

2

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Funding (US$ mn) Estimated Valuation (US$ mn, RHS)

Founded in 1994

30%

32%

34%

36%

38%

0

100

200

300

400

500

600

2017 2018 2019

Revenues (US$ m) % YoY (RHS)

9%

10%

10%

11%

0

20

40

60

2019 2020

EBITDA EBITDA % (RHS)

A

r

t

i

c

l

e

i

n

t

e

n

d

e

d

f

o

r

:

a

s

h

a

.

g

o

p

a

l

a

k

r

i

s

h

n

a

n

#

u

n

i

l

e

v

e

r

.

c

o

m](https://image.slidesharecdn.com/indias100unicorns-210724041519/85/India-s-100-unicorns-136-320.jpg)

![India Market Strategy 145

Companies Mentioned (Price as of 08-Mar-2021)

Alphabet (GOOGL.OQ, $2007.5)

Disclosure Appendix

Analyst Certification

Neelkanth Mishra and Abhay Khaitan each certify, with respect to the companies or securities that the individual analyzes, that (1) the views

expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her

compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report.

3-Year Price and Rating History for Alphabet (GOOGL.OQ)

GOOGL.OQ Closing Price Target Price

Date (US$) (US$) Rating

20-Apr-18 1077.32 1350.00 O

16-Jul-18 1196.51 1330.00

24-Jul-18 1258.15 1375.00

19-Oct-18 1105.18 1500.00

26-Oct-18 1083.75 1450.00

05-Feb-19 1151.87 1400.00

26-Jul-19 1245.22 1500.00

23-Oct-19 1257.63 1700.00

20-Apr-20 1261.15 1500.00

29-Apr-20 1342.18 1600.00

20-Jul-20 1563.84 1850.00

30-Oct-20 1616.11 1950.00

22-Jan-21 1892.56 2000.00

03-Feb-21 2058.88 2360.00

* Asterisk signifies initiation or assumption of coverage.

As of December 10, 2012 Analysts’ stock rating are defined as follows:

Outperform (O) : The stock’s total return is expected to outperform the relevant benchmark* over the next 12 months.

Neutral (N) : The stock’s total return is expected to be in line with the relevant benchmark* over the next 12 months.

Underperform (U) : The stock’s total return is expected to underperform the relevant benchmark* over the next 12 months.

*Relevant benchmark by region: As of 10th December 2012, Japanese ratings are based on a stock’s total return relative to the analyst's coverage universe which

consists of all companies covered by the analyst within the relevant sector, with Outperforms representing the most attractive, Neutrals the less attractive, and

Underperforms the least attractive investment opportunities. As of 2nd October 2012, U.S. and Canadian as well as European (excluding Turkey) ratings are

based on a stock’s total return relative to the analyst's coverage universe which consists of all companies covered by the analyst within the relevant sector, with

Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. For Latin America,

Turkey and Asia (excluding Japan and Australia), stock ratings are based on a stock’s total return relative to the average total return of the relevant country or

regional benchmark (India - S&P BSE Sensex Index); prior to 2nd October 2012 U.S. and Canadian ratings were based on (1) a stock’s absolute total return

potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe. For Australian and

New Zealand stocks, the expected total return (ETR) calculation includes 12-month rolling dividend yield. An Outperform rating is assigned where an ETR is

greater than or equal to 7.5%; Underperform where an ETR less than or equal to 5%. A Neutral may be assigned where the ETR is between -5% and 15%. The

overlapping rating range allows analysts to assign a rating that puts ETR in the context of associated risks. Prior to 18 May 2015, ETR ranges for Outperform and

Underperform ratings did not overlap with Neutral thresholds between 15% and 7.5%, which was in operation from 7 July 2011.

Restricted (R) : In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications,

including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain

other circumstances.

Not Rated (NR) : Credit Suisse Equity Research does not have an investment rating or view on the stock or any other securities related to the

company at this time.

Not Covered (NC) : Credit Suisse Equity Research does not provide ongoing coverage of the company or offer an investment rating or

investment view on the equity security of the company or related products.

Volatility Indicator [V] : A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past

24 months or the analyst expects significant volatility going forward.

Analysts’ sector weightings are distinct from analysts’ stock ratings and are based on the analyst’s expectations for the fundamentals and/or

valuation of the sector* relative to the group’s historic fundamentals and/or valuation:

Overweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is favorable over the next 12 months.

Market Weight : The analyst’s expectation for the sector’s fundamentals and/or valuation is neutral over the next 12 months.

Underweight : The analyst’s expectation for the sector’s fundamentals and/or valuation is cautious over the next 12 months.

*An analyst’s coverage sector consists of all companies covered by the analyst within the relevant sector. An analyst may cover multiple sectors.

Target Price Closing Price GOOGL.OQ

01- Jan- 2019 01- Jan- 2020 01- Jan- 2021

500

1,000

1,500

2,000

2,500

O U T PERFO RM

A

r

t

i

c

l

e

i

n

t

e

n

d

e

d

f

o

r

:

a

s

h

a

.

g

o

p

a

l

a

k

r

i

s

h

n

a

n

#

u

n

i

l

e

v

e

r

.

c

o

m](https://image.slidesharecdn.com/indias100unicorns-210724041519/85/India-s-100-unicorns-145-320.jpg)

This document lists and analyzes 100 Indian startup companies that have reached unicorn status, meaning a valuation of over $1 billion. It discusses how India's corporate landscape is being transformed by the rapid growth of startups in recent years. Key factors enabling this transformation include increased funding from investors, improved infrastructure and regulation, and growth in sectors like FinTech, EdTech, e-commerce, and pharmaceuticals/biotech. The document argues this trend could create a virtuous cycle of further startup growth and investment in India.