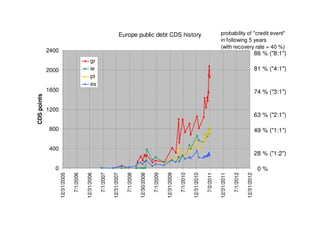

1. Europe public debt CDS history probability of "credit event"

in following 5 years

(with recovery rate = 40 %)

2400

86 % ("8:1")

gr

2000 ie 81 % ("4:1")

pt

es

1600 74 % ("3:1")

CDS points

1200

63 % ("2:1")

800 49 % ("1:1")

400

28 % ("1:2")

0 0%

12/31/2005

7/1/2006

12/31/2006

7/1/2007

12/31/2007

7/1/2008

12/30/2008

7/1/2009

12/31/2009

7/1/2010

12/31/2010

7/2/2011

12/31/2011

7/1/2012

12/31/2012

2. interest rate deltas (~ 10 year bonds *, relative to benchmark

bunds)

20% probability

de

of "credit

fr de Germany

event"

at fr France in next 5

at Austria

16% be years,

it be Belgium roughly !!

es it Italy

pt es Spain

12% ie pt Portugal

ie Ireland

70 %

gr

gr_model gr Greece

ie_model

8% pt_model 50%

es_model

it_model

be_model

4% 25%

10%

0%

0%

12/31/2009

4/1/2010

7/1/2010

9/30/2010

12/31/2010

4/1/2011

7/1/2011

10/1/2011

12/31/2011

* pt 5 years for data availability

3. Financial mechanics of

interest rate spreads / CDS / default probabilities

All cited data sources are reliable, and long term freely available

- Typical assessment of interest rates with percentage numbers for

3 month / 10 year (see e.g. http://www.economist.com/markets-data,

look for “trade exchange rates …) or

http://www.bloomberg.com/markets/rates-bonds/government-bonds/germany/)

- Typical CDS contracts for n = 5 years, with a r = 40 % “recovery rate”, cited with

points p (1 = 100 % = 10000 points, data from e.g. Markit(R) ,

shown at e.g. http://ftalphaville.ft.com/, or bloomberg

derived Default probability d = 1 - EXP(- n * p / (1-r) )

most simple, analytical approximation ONLY !

(interest) Rates and (CDS) points are normally strongly correlated