Countrywide Option Arm Loans (Negative Amortization) July 26 2006

•

0 likes•1,036 views

Countrywide Option Arm loans (Negative Amortization) July 26 2006. These loans could qualify to 90% loan-to-value and allowed a teaser rate of as low as 1% payment, which would negatively amortize up to 120% of the value of the property. The borrower would make the 1% payment, and go further into debt. Countrywide likely sold these loans as derivatives before having to deal with the inevitable foreclosure.

Recommended

More Related Content

Similar to Countrywide Option Arm Loans (Negative Amortization) July 26 2006

Similar to Countrywide Option Arm Loans (Negative Amortization) July 26 2006 (20)

More from Bitsytask

More from Bitsytask (20)

Recently uploaded

Recently uploaded (20)

Countrywide Option Arm Loans (Negative Amortization) July 26 2006

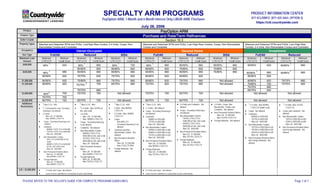

- 1. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Product PayOption ARM Finance Type Purchase and Rate/Term Refinances Seller’s Guide Section 10.3 Property Types Attached and Detached SFRs and PUDs, Low/High-Rise Condos, 2-4 Units, Coops, Non- Warrantable Condos and Condotels Attached and Detached SFRs and PUDs, Low-/High-Rise Condos, Coops, Non-Warrantable Condos and Condotels Attached and Detached SFRs and PUDs, Low-/High-Rise Condos, 2-4 Units, Non-Warrantable Condos and Condotels Occupancy Owner-Occupied Second Home Investment Doc Type Full/Alt Reduced SISA Full/Alt Reduced SISA Full/Alt Reduced Maximum Loan Amount Maximum LTV/CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score $400,000 95% 95% 1 680 95% 1 700 95% 1 660 90/90% 660 90/90% 660 1 620 90/90% 620 90/90% 620 90/90% 620 75/80% 620 70/80% 620 90/90% 620 80/80% 1 660 95% 1 680 90/90% 660 80/80% 660 90/90% 660 80/80% 660 90/90% $650,000 1 660 90/90% 620 75/75% 620 75/75% 620 80/90% 620 65/80% 620 75/80% 660 80/90% 620 80/80% 1 660 $1,000,000 80/90% 620 75/90% 660 75/75% 660 80/80% 620 75/75% 660 Not allowed 80/80% 620 75/75% 660 75/75% 70/80% 720 2 700 70/70% 660 $1,500,000 80/80% 620 70/70% 660 65/70% 660 75/75% 620 70/70% 660 Not allowed 65/70% 620 70/70% 660 $3,000,000 80%2 700 70/70% 700 Not allowed 70/70% 700 65/70% 700 Not allowed Not allowed Not allowed 70/70% 700 $6,000,000 60/70% 720 60/70% 720 Not allowed 60/70% 720 60/70% 720 Not allowed Not allowed Not allowed Additional Restrictions: • 1 Max CLTV: 90% • 2 1-Unit properties only. Secondary financing is not allowed • 3-4 Units: - Max. L/A: $1,500,000 - Max. 90/90% LTV/CLTV • Coops: Secondary financing is not allowed. • Condotels: - 80/80% LTV/CLTV to $350,000 - 75/75% LTV/CLTV to $650,000 - Max L/A: $650,000 • Non-Warrantable Condos: - 95% LTV to $300,000 w/ 620 credit - 80/80% LTV/CLTV to $650,000 w/ min. 620 credit score. - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90/90% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 80/80% LTV/CLTV • 1 Max CLTV: 90% • 2 2-4 Units: Max 70/70% w/ min. 660 credit • 3-4 Units: - Max. L/A: $1,500,000 - Max. 90/90% LTV/CLTV • Coops: Secondary financing is not allowed. • Condotels: Not allowed • Non-Warrantable Condos: - 80/80% LTV/CLTV to $500,000 w/ min. 660 credit - 75/75% LTV/CLTV to $650,000 w/ min. 660 credit - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90/90% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75/75% LTV/CLTV • 1 Max CLTV: 90% • 2 Units: Max 90/90% LTV/CLTV • 3-4 Units: Max. 80/80% LTV/CLTV • Coops: - Max 80% LTV - Secondary financing is not allowed. • Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max LTV/CLTV 90% • Foreign Nationals: Not allowed • 1 Max CLTV: 90% • 2 -4 units: Not allowed • Coops: Secondary financing is not allowed. • Condotels: - 80/80% to $350,000 - 75/75% to $650,000 - Max L/A: $650,000 • Non-Warrantable Condos: - 90/90% to $400,000 at 680 - 80/80% to $500,000 at 620 - 75/75% to $650,000 at 620 - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90/90% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75/75% LTV/CLTV • 2-4 Units and Condotels: Not allowed • Coops: Secondary financing is not allowed. • Non-Warrantable Condos: - 70/70% LTV/CLTV to $400,000 w/ min. 660 credit - 65/65% LTV/CLTV to $650,000 w/ min. 660 credit - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 75/75% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75/75% LTV/CLTV • 2-4 Units, Coops, Non- Warrantable Condos and Condotels: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 75/75% LTV/CLTV • Foreign Nationals: Not allowed • 1 3-4 Units: Max 90/90% LTV/CLTV w/680 credit • Coops: Not allowed • Condotels: - 80/80% to $350,000 - 75/75% to $650,000 - Max L/A: $650,000 • Non-Warrantable Condos: - 75/75% to $350,000 at 620 - 70/70% to $400,000 at 620 - 65/65% to $650,000 at 620 - Max L/A: $650,000 • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 1 3-4 Units: Max 75/75% LTV/CLTV • Coops and Condotels: Not allowed • Non-Warrantable Condos: - 70/70 to $350,000 at 680 - 65/65 to $650,000 at 680 - Max L/A: $650,000 • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed L/A > $3,000,000 • 2-4 Units and Coops: Not allowed • Loans must be submitted to Countrywide for prior underwriting. • 2-4 Units and Coops: Not allowed • Loans must be submitted to Countrywide for prior underwriting. PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 1 of 7

- 2. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Product PayOption ARM Finance Type Cash Out Refinances Seller’s Guide Section 10.3 Property Types Attached and Detached SFRs and PUDs, Low/High Rise Condos, 2-4 Units and Coops Attached and Detached SFRs and PUDs and Low/High-Rise Condos Attached and Detached SFRs and PUDs, Low/High-Rise Condos and 2-4 Units Occupancy Owner-Occupied Second Home Investment Doc Type Full/Alt Reduced SISA Full/Alt Reduced Full/Alt Reduced Maximum Loan Amount Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/ CLTV Minimum Credit Score Maximum LTV/CLTV Minimum Credit Score Maximum LTV/CLTV Minimum Credit Score $400,000 90/90% 620 90/90% 660 90/90% 660 90/90% 660 90/90% 1 660 75/75% 620 75/75% 620 90/90% 620 75/75% 620 75/90% 620 75/75% 660 80/90% 1 660 90/90% 2 660 $650,000 90/90% 620 2 70/70% 1 620 70/70% 660 90/90% 660 75/75% 660 70/90% 620 75/75% 1 660 $1,000,000 80/80% 1 620 75/75% 660 70/70% 660 80/80% 620 75/75% 660 80/80% 3 620 75/75% 2 660 70/70% 3 660 $1,500,000 75/75% 3 2 620 70/70% 660 Not allowed 75/75% 620 70/70% 660 60/60% 3 620 70/70% 660 $3,000,000 70/70% 700 60/70% 700 Not allowed 65/70% 700 60/70% 700 Not allowed Not allowed $6,000,000 55/70% 720 55/70% 720 Not allowed 55/70% 720 55/70% 720 Not allowed Not allowed Additional Restrictions: • 3-4 Units: - Max. L/A: $1,500,000 - Max. 80/80% LTV/CLTV - 1 Min. 660 credit score required - 2 Max. 70/70% LTV/CLTV with min. 680 credit score • Coops: Secondary financing is not allowed. • Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: – Max L/A: $1,500,000 – Max 70/70% LTV/CLTV • Foreign Nationals: – Max L/A: $1,000,000 – Max 70/70% LTV/CLTV • 3-4 Units: - Max. L/A: $1,500,000 - 1 Max. 75/75% LTV/CLTV with min. 660 credit score • Coops: - Max LTV 80% - Secondary financing is not allowed. • Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70/70% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 70/70% LTV/CLTV • 3-4 Units: Max. 80/80% LTV/CLTV • Coops: - Max LTV 80% - Secondary financing is not allowed. • Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 2-4 units, Coops, Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70/70% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 65/65% LTV/CLTV • 2-4 units, Coops, Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 65/65% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 65/65% LTV/CLTV • L/A > $3,000,000: Loans must be submitted to Countrywide for prior underwriting. • 1 1-2 units only • 2 3-4 Units: Max 75/75% LTV/CLTV w/ min. 680 credit • 3 3-4 Units: Max 55/60% LTV/CLTV w/ min. 620 credit • Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 1 3-4 Units: Max 70/70% LTV/CLTV • 2 3-4 Units: Max 45/65% LTV/CLTV • Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 3-4 Units: Max L/A: $1,000,000 L/A > $3,000,000 • 2-4 Units and Coops: Not allowed • Loans must be submitted to Countrywide for prior underwriting. L/A > $3,000,000: Loans must be submitted to Countrywide for prior underwriting. Maximum Cash Out • LTV > 80%: $325,000 • LTV 55.01-80%: $500,000 • LTV < 55%: Unrestricted • LTV > 80%: $325,000 • LTV 55.01-80%: $500,000 • LTV < 55%: Unrestricted • LTV > 55%: $325,000 • LTV < 55%: Unrestricted PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 2 of 7

- 3. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Product 1-Month and 6-Month Interest Only LIBOR ARM Finance Type Purchase and Rate/Term Refinances Seller’s Guide Section 10.3 Eligible Property Types Attached and Detached SFRs and PUDs, Low & High Rise Condos, 2-4 Units and Coops, Non- Warrantable Condos and Condotels Attached and Detached SFRs and PUDs, Low & High Rise Condos and Coops, Non- Warrantable Condos and Condotels Attached and Detached SFRs and PUDs, Low & High Rise Condos, 2-4 Units, Non-Warrantable Condos and Condotels Occupancy Owner-Occupied Second Home Investment Doc Type Full/Alt Reduced Fast & Easy Full/Alt Reduced Fast & Easy Full/Alt Reduced Maximum Maximum LTV/CLTV Minimum Credit Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Loan Amount Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Minimum Credit Score 95/95 1,4 700 95/95% 620 95/95% 680 95/95 660 90/90% 660 90/90% 620 $400,000 80/100% 660 1 80/100% 700 90/95 620 75/80% 620 90/90% 700 90/90% 620 80/80% 1 660 80/90 2 700 95/95% 680 90/90% 660 90/90 660 80/80% 660 90/90% 1 660 1 90/95% 620 75/75% 620 $650,000 80/100% 680 80/100% 700 80/95 620 65/80% 620 80/90% 1 700 80/90% 620 80/80% 1 660 $1,000,000 80/100% 680 80/95% 620 75/90% 660 80/90 2 700 80/80% 620 75/75% 660 Not allowed 80/80% 620 75/75% 660 75/75% 70/80% 720 1 700 70/70% 660 $1,500,000 80/80% 620 70/70% 660 60 3 LTV 700 75/75 620 70/70% 660 Not allowed 65/70% 620 70/70% 660 $2,000,000 80%2 or 70/70% 700 70/70% 700 60 3 LTV 700 70/70 700 65/70% 700 $3,000,000 80%2 or 70/70% 700 70/70% 700 Not allowed 70/70 700 65/70% 700 Not allowed Not allowed Not allowed $6,000,000 60/70% 720 60/70% 720 Not allowed 60/70 720 60/70% 720 Not allowed Not allowed Not allowed Additional Restrictions: • 1 2 Units: Min. 680 credit required • 2 80% LTV: 1-Unit properties only. Secondary financing is not allowed • 3-4 Units: - Max. L/A: $1,500,000 - Max. 90/90% LTV/CLTV • Coops: Secondary financing not allowed. • Condotels: - 80/80% to $350,000 - 75/75% to $650,000 - Max L/A: $650,000 • Non-Warrantable Condos: - 95/95% to $300,000 at 620 - 80/80% to $650,000 at 620 - Max L/A: $650,000 • Non-Permanent Resident Aliens: – Max L/A: $1,500,000 – Max 90/90% LTV/CLTV • Foreign Nationals: – Max L/A: $1,000,000 – Max 80/80% LTV/CLTV • 1 2-4 Units: Max 70/70% w/660 credit • 3-4 Units: - Max. L/A: $1,500,000 - Max. 90/90% LTV/CLTV • Coops: Secondary financing not allowed. • Non-Warrantable Condos: - 80/80% to $500,000 at 660 - 75/75% to $650,000 at 660 - Max L/A: $650,000 • Condotels: Not allowed • Non-Permanent Resident Aliens: – Max L/A: $1,500,000 – Max 90/90% LTV/CLTV • Foreign Nationals: – Max L/A: $1,000,000 – Max 75/75% LTV/CLTV • 1 2 Units: Max 90/90% LTV/CLTV at 730 • 2 2 Units: Max 80/80% LTV/CLTV at 730 • 3 2 Units: Not allowed • 4 High-Rise Condos: Max 90/90% LTV/CLTV • 3-4 Units, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90/90% LTV/CLTV • Foreign Nationals: Not allowed • Secondary financing not allowed on loans over $1 million. • 2 -4 Units: Not allowed • Coops: Secondary financing is not allowed. • Non-Warrantable Condos: - 90/90% to $400,000 at 680 - 80/80% to $500,000 at 620 - 75/75% to $650,000 at 620 - Max L/A: $650,000 • Condotels: - 80/80% LTV/CLTV to $350,000 - 75/75% LTV/CLTV to $650,000 - Max L/A: $650,000 • Non-Permanent resident aliens: - Max L/A: $1,500,000 - Max 90/90% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75/75% LTV/CLTV • 2-4 Units and Condotels: Not allowed • Coops: Secondary financing is not allowed. • Non-Warrantable Condos: - 70/70% LTV/CLTV to $400,000 at 660 - 65/65% LTV/CLTV to $650,000 at 660 - Max L/A: $650,000 • Non-Permanent resident aliens: - Max L/A: $1,500,000 - Max 75/75% LTV/CLTV • Foreign Nationals: – Max L/A: $1,000,000 – Max 75/75% LTV/CLTV • 1 High-Rise Condos: Max 75/75% LTV/CLTV • 2-4 Units, Coops, Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90/90% LTV/CLTV - Foreign Nationals: Not allowed • 1 3-4 Units: Max 90/90% LTV/CLTV w/ 680 credit • Coops: Not allowed • Condotels: - 80/80% LTV/CLTV to $350,000 - 75/75% LTV/CLTV to $650,000 – Max L/A: $650,000 • Non-Warrantable condos: - 75/75% LTV/CLTV to $350,000 at 620 - 70/70% LTV/CLTV to $400,000 at 620 - 65/65% LTV/CLTV to $650,000 at 620 - Max L/A: $650,000 • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 1 3-4 Units: Max 75/75% LTV/CLTV • Coops and Condotels: Not allowed • Non-Warrantable condos: - 70/70% LTV/CLTV to $350,000 at 680 - 65/65% LTV/CLTV to $650,000 at 680 - Max L/A: $650,000 • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed L/A > $3,000,000 • 2-4 Units and Coops: Not allowed • Loans must be submitted to Countrywide for prior u/w • Coops: Not allowed. • Loans must be submitted to Countrywide for prior underwriting. PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 3 of 7

- 4. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Product 1-Month and 6-Month Interest Only LIBOR ARM Finance Type Cash Out Refinances Seller’s Guide Section 10.3 Eligible Property Types Attached and Detached SFRs and PUDs, Low & High Rise Condos, Cooperatives, and 2-4 Units Attached and Detached SFRs and PUDs and Low & High Rise Condos Attached and Detached SFRs and PUDs, Low & High Rise Condos and 2-4 Units Occupancy Owner-Occupied Second Home Investment Doc Type Full/Alt Reduced Fast & Easy Full/Alt Reduced Fast & Easy Full/Alt Reduced Maximum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Minimum Maximum Loan Amount LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Credit Score LTV/CLTV Minimum Credit Score $400,000 90/95% 620 90/90% 660 90/90% 660 90/90% 1 620 75/75% 620 70/70% 700 90/90% 620 75/75% 620 70/70% 700 75/90% 620 75/75% 660 80/90% 1 660 90/90% 2 660 $650,000 90/95% 620 2 70/70% 1 620 70/70% 700 90/90% 660 75/75% 660 70/70% 700 70/90% 620 75/75% 1 660 $1,000,000 80/80% 1 620 75/75% 660 Not allowed 80/80% 620 75/75% 660 Not allowed 80/80% 3 620 75/75% 2 660 70/70% 3 660 $1,500,000 75/75% 3 2 620 70/70% 660 Not allowed 75/75% 620 70/70% 660 Not allowed 60/60% 3 620 70/70% 660 $3,000,000 70/70% 700 60/70% 700 Not allowed 65/70% 700 60/70% 700 Not allowed Not allowed Not allowed $6,000,000 55/70% 720 55/70% 720 Not allowed 55/70% 720 55/70% 720 Not allowed Not allowed Not allowed Additional Restrictions: • 3-4 Units: - Max. L/A: $1,500,000 - Max. 80/80% LTV/CLTV - 1 Min. 660 credit score - 2 Max. 70/70% LTV/CLTV with 680 credit score • Coops: Secondary financing is not allowed. • Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70/70% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 70/70% LTV/CLTV • 3-4 Units: - Max. L/A: $1,500,000 1 75/75% LTV/CLTV with min. 660 credit score • Coops: - Max 80% LTV - Secondary financing is not allowed. • Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70/70% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 70/70% LTV/CLTV • 2 Units: Minimum 730 credit score required • 3-4 Units, Condotels and Non- Warrantable Condos: Not allowed • Coops: Secondary financing is not allowed. • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70/70% LTV/CLTV • Foreign Nationals: Not allowed • 2-4 Units, Coops, Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70/70% LTV/CLTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 65/65% LTV/CLTV • 2-4 Units, Coops, Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 65/65% LTV/CLTV • Foreign Nationals: Max 65/65% LTV/CLTV • 2-4 Units, High-Rise Condos, Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: Max 70/70% LTV/CLTV • Foreign Nationals: Not allowed • 1 -2 units only • 2 3-4 Units: Max 75/75% LTV/CLTV w/ 680 credit • 3 3-4 Units: Max 55/60% LTV/CLTV w/620 credit • Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 1 3-4 Units: Max 70/70% LTV/CLTV • 2 3-4 Units: Max 45/65% LTV/CLTV • Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 3-4 Units: Max L/A $1,000,000 L/A > $3,000,000 • 2-4 Units and Coops: Not allowed • Loans must be submitted to Countrywide for prior underwriting. Loans greater than $3,000,000 must be submitted to Countrywide for prior underwriting. Maximum Cash Out • LTV > 80%: $325,000 • LTV 55.01-80%: $500,000 • LTV < 55%: Unrestricted • LTV > 80%: $325,000 • LTV 55.01-80%: $500,000 • LTV < 55%: Unrestricted • LTV > 55%: $325,000 • LTV < 55%: Unrestricted PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 4 of 7

- 5. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Product FlexSaver (First Lien HELOC) Finance Type Purchase and Rate/Term Refinances Seller’s Guide Section 10.3 Property Types Attached and Detached SFRs and PUDs, Low & High Rise Condos, 2-4 Units, Coops, Non-Warrantable Condos and Condotels Attached and Detached SFRs and PUDs, Low & High Rise Condos, Coops, Non-Warrantable Condos and Condotels Attached and Detached SFRs and PUDs, Low & High Rise Condos, 2-4 Units, Non-Warrantable Condos and Condotels Occupancy Owner-Occupied Second Home Investment Doc Type Full/Alt Reduced Full/Alt Reduced Full/Alt Reduced Maximum Loan Amount Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score $400,000 95% 620 95% 680 95% 660 90% 660 90% 620 90% 620 75% 620 90% 620 80% 1 660 95% 680 90% 660 90% 660 80% 660 90% 660 $650,000 1 90% 620 75% 620 80% 620 65% 620 80% 620 80% 1 660 $1,000,000 80% 620 75% 660 80% 620 75% 660 80% 620 75% 660 75% $1,500,000 80% 620 1 700 70% 660 70% 660 75% 620 70% 660 65% 620 70% 660 $3,000,000 80%1 700 70% 700 70% 700 70% 700 65% 700 Not allowed Not allowed Additional Restrictions: • 1 1-Unit properties only • Secondary financing is not allowed. • 3-4 Units: - Max. L/A: $1,500,000 - Max. 90% LTV • Non-Warrantable Condos: - 95% LTV to $300,000 at 620 - 80% LTV to $650,000 at 620 - Max L/A: $650,000 • Condotels: - 80% LTV to $350,000 - 75% LTV to $650,000 - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 80% LTV • 1 2-4 Units: Max 70% LTV w/660 credit • Secondary financing is not allowed. • 3-4 Units: - Max. L/A: $1,500,000 - Max. 90% LTV • Non-Warrantable Condos: - 80% LTV to $500,000 at 660 - 75% LTV to $650,000 at 660 - Max L/A: $650,000 • Condotels: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75% LTV • Secondary financing is not allowed. • 2 -4 Units: Not allowed • Non-Warrantable Condos: - 90% LTV to $400,000 at 680 - 80% LTV to $500,000 at 620 - 75% LTV to $650,000 at 620 - Max L/A: $650,000 • Condotels: - 80% LTV to $350,000 - 75% LTV to $650,000 - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 90% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75% LTV • Secondary financing is not allowed. • 2-4 Units and Condotels: Not allowed • Non-Warrantable Condos: - 70% LTV to $400,000 at 660 - 65% LTV to $650,000 at 660 - Max L/A: $650,000 • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 75% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 75% LTV • 1 3-4 Units: 680 credit required • Secondary financing is not allowed. • Condotels: - 80% LTV to $350,000 - 75% LTV to $650,000 - Max L/A: $650,000 • Non-Warrantable Condos: - 75% LTV to $350,000 at 620 - 70% LTV to $400,000 at 620 - 65% LTV to $650,000 at 620 - Max L/A: $650,000 • Coops: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 1 3-4 Units: Max 70% LTV • Secondary financing is not allowed. • Non-Warrantable Condos: - 70% LTV to $350,000 at 680 - 65% LTV to $650,000 at 680 - Max L/A: $650,000 • Coops and Condotels: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 5 of 7

- 6. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Product FlexSaver (First Lien HELOC) Finance Type Cash Out Refinances Seller’s Guide Section 10.3 Property Types Attached and Detached SFRs and PUDs, Low & High Rise Condos, 2-4 Units and Coops Attached and Detached SFRs and PUDs, Low & High Rise Condos and Coops Attached and Detached SFRs and PUDs, Low & High Rise Condos, and 2-4 Units Occupancy Owner-Occupied Second Home Investment Doc Type Full/Alt Reduced Full/Alt Reduced Full/Alt Reduced Maximum Loan Amount Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score Maximum LTV Minimum Credit Score $400,000 90% 620 90% 660 90% 660 90% 1 660 75% 620 90% 620 75% 620 75% 620 75% 680 80% 1 660 90% 2 660 $650,000 90% 620 2 70% 1 620 90% 660 75% 660 70% 620 75% 1 680 $1,000,000 80% 1 620 75% 660 80% 620 75% 660 80% 3 620 75% 2 680 70% 3 660 $1,500,000 75% 3 2 620 70% 660 75% 620 70% 660 60% 3 620 70% 660 $3,000,000 70% 700 65% 700 65% 700 60% 700 Not allowed Not allowed Additional • 3-4 Units: Restrictions: - Max. L/A: $1,500,000 - Max. 80% LTV - 1 Min. 660 credit score - 2 Max. 70% LTV with 680 credit score • Secondary financing is not allowed. • Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 70% LTV • Secondary financing is not allowed. • 3-4 Units: - Max. $1,500,000 - 1 75% LTV with min. 660 credit score • Coops: Max 80% LTV • Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 65% LTV • Secondary financing is not allowed. • 2-4 Units, Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 70% LTV • Foreign Nationals: - Max L/A: $1,000,000 - Max 65% LTV • Secondary financing is not allowed. • 2-4 Units, Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens: - Max L/A: $1,500,000 - Max 65% LTV • Foreign Nationals: Not allowed • 1 1-2 units only • 2 3-4 Units: Max 75% LTV w/680 credit • 3 3-4 Units: Max 55% LTV w/620 credit • Secondary financing is not allowed. • Coops, Condotels and Non-Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed • 1 3-4 Units: Max 70% LTV • 2 3-4 Units: Max 45% LTV • Secondary financing is not allowed. • Coops, Condotels and Non- Warrantable Condos: Not allowed • Non-Permanent Resident Aliens and Foreign Nationals: Not allowed Maximum Cash Out • LTV > 80%: $325,000 • LTV 55.01-80%: $500,000 • LTV < 55%: Unrestricted • LTV > 80%: $325,000 • LTV 55.01-80%: $500,000 • LTV < 55%: Unrestricted • LTV > 55%: $325,000 • LTV < 55%: Unrestricted PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 6 of 7

- 7. SPECIALTY ARM PROGRAMS PayOption ARM, 1-Month and 6-Month Interest Only LIBOR ARM, FlexSaver PRODUCT INFORMATION CENTER 877-4CLDINFO (877-425-3463, OPTION 3) https://cld.countrywide.com July 26, 2006 Underwriting Addendum Section 10.3 Documentation Description Reserve Requirements Appraisal Requirements Eligible Borrowers Credit Score DTI Ratio Full/Alt • Verify Income/Verify Assets Documentation • Current verification of employment, 2- year history required (self-employed = same business at same location for 2 years) • 4506-T required (if tax returns are included in loan file) • L/A < $3,000,000: - Owner-occupied: 2 months - Second homes: 6 months - Investment: 6 months • L/A > $3,000,000: - Owner-occupied: 9 months - Second homes: 9 months • L/A or combined L/A < $1,000,000: One full appraisal • L/A or combined L/A > $1,000,000 < $3,000,000: One full appraisal plus one field review from a Countrywide-approved review appraisal company* • L/A or combined L/A > $3,000,000: One full appraisal plus one field review completed by a LandSafe® Services-approved “Super Jumbo” appraiser * Refer to Section 6.9, Collateral Appraisal, of the Seller’s Guide for a list of Countrywide-approved review appraisal companies. • Salaried, self-employed and passive income borrowers allowed • U.S. Citizens and Permanent resident aliens: Allowed • Non-Permanent Resident Aliens: Allowed with restrictions • Foreign Nationals: Allowed with restrictions • Minimum 620 • Use middle of 3 or lowest of 2 for the LOWEST scoring borrower 40% • This ratio may be exceeded with a CLUES “Accept” • Loans greater than $3,000,000: DTI of 50% allowed with compensating factors as determined by Countrywide prior underwrite. Non-conforming Fast & Easy Documentation • State Income/State Assets • Current verification of employment, 2 year history required (self-employed = same business at same location for 2 years) • 4506-T required Not required • 1 full Uniform Residential Appraisal Report (URAR) or Form 2055 Interior/Exterior required • L/A or combined L/A < $1,000,000: One full appraisal • L/A or combined L/A > $1,000,000: One full appraisal plus a field review from a Countrywide-approved review appraisal company* * Refer to Section 6.9, Collateral Appraisal, of the Seller’s Guide for a list of Countrywide-approved review appraisal companies. • Salaried, self-employed and passive income borrowers allowed • US Citizens and Permanent Resident Aliens: Allowed • Non-Permanent Resident Aliens: Allowed with restrictions • Foreign Nationals: Not allowed • Minimum 700 • Use middle of 3 or lowest of 2 for the LOWEST scoring borrower Determined by CLUES: generally not to exceed 55% Reduced Documentation • State Income/Verify Assets • Current verification of employment with 2 year history in the same location • 4506-T required for loans greater than $3,000,000 • L/A < $3,000,000: – Owner-occupied: 3 months – Second homes & Investment: 6 months • L/A > $3,000,000: • Owner-occupied & second homes: 12 months • Salaried, commissioned self-employed and passive income borrowers allowed • U.S. Citizens and Permanent Resident Aliens: Allowed • Non-Permanent Resident Aliens: Allowed with restrictions • Foreign Nationals: Allowed with restrictions • Minimum 620 • Use middle of 3 or lowest of 2 for the LOWEST scoring borrower DTI < 38% Loans greater than $3,000,000: DTI of 50% allowed with compensating factors as determined by Countrywide prior underwrite. SISA Documentation • State Income/State Assets • Current verification of employment with 2 year history in the same location • 4506-T not required • Owner-occupied: 3 months • Second homes: 6 months • L/A or combined L/A < $1,000,000: One full appraisal • L/A or combined L/A > $1,000,000 < $3,000,000: One full appraisal plus one field review from a Countrywide-approved review appraisal company* • L/A or combined L/A > $3,000,000: One full appraisal plus one field review completed by a LandSafe Services-approved “Super Jumbo” appraiser *Refer to Section 6.9, Collateral Appraisal, of the Seller’s Guide for a list of Countrywide-approved review appraisal companies. • Salaried, commissioned self-employed and passive income borrowers allowed • U.S. Citizens and Permanent Resident Aliens: Allowed • Non-Permanent Resident Aliens: Allowed with restrictions • Foreign Nationals: Not allowed • Minimum 620 • Use middle of 3 or lowest of 2 for the LOWEST scoring borrower DTI < 38% Geographic Restrictions • Loans exceeding $650,000: Restricted to major metropolitan areas only, or in areas where there is sufficient marketability, as established in the appraisal, for upper-end properties. • Arkansas and Texas: FlexSaver is not available. • Maine: PayOption and 1-Month & 6-Month Interest Only LIBOR are not available. • New York: - PayOption loans allowed to a maximum 80% LTV. - FlexSaver loans are not allowed with consolidation, extension and modification refinances. Refer to Section 4.6, Geographic Restrictions, for information on additional state restrictions. PLEASE REFER TO THE SELLER'S GUIDE FOR COMPLETE PROGRAM GUIDELINES. Page 7 of 7