The document contains a series of accounting transactions recorded between June 1st and June 22nd. On June 1st, capital stock of $30,000 was deposited into the bank. Machinery worth $5,000 was purchased from the bank on June 2nd. $6,000 was deposited into the bank from the cash account on June 5th. Merchandise worth $25,000 was purchased from suppliers on credit on June 8th. The suppliers were paid $25,000 on June 9th. A loan of $25,000 was taken out from the bank on June 12th. Customers purchased $15,000 worth of merchandise on credit on June 15th. The customers paid $15,000 on

A Geometrical Approach to Multi-currency Reconciliation

Práctica 1 tema 5 libro diario

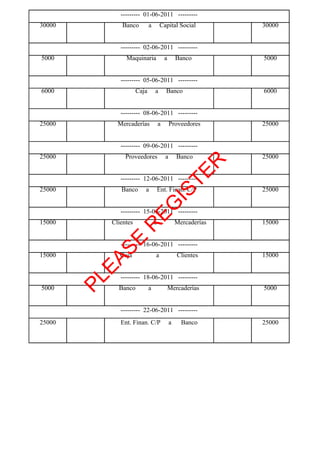

1. --------- 01-06-2011 ---------

30000 Banco a Capital Social 30000

--------- 02-06-2011 ---------

5000 Maquinaria a Banco 5000

--------- 05-06-2011 ---------

6000 Caja a Banco 6000

--------- 08-06-2011 ---------

25000 Mercaderías a Proveedores 25000

--------- 09-06-2011 ---------

25000 Proveedores a Banco 25000

R

TE

--------- 12-06-2011 ---------

25000 Banco a Ent. Finan. C/P 25000

IS

EG

--------- 15-06-2011 ---------

15000 Clientes a Mercaderías 15000

R

E

--------- 16-06-2011 ---------

S

15000 Caja a Clientes 15000

EA

--------- 18-06-2011 ---------

PL

5000 Banco a Mercaderías 5000

--------- 22-06-2011 ---------

25000 Ent. Finan. C/P a Banco 25000