CBP PRE-ASSESSMENT IMPORT AUDIT QUESTIONNAIRE

•Download as PPTX, PDF•

1 like•593 views

Licensed Customs Broker and Certified Customs Specialist makes your Company's Import Operations compliant with U.S. Customs and Border Protection (CBP) Regulations, thereby eliminating CBP penalties against your Company! Presented by Brent Claypool, LCB/CCS Email: bc606039@gmail.com

Recommended

More Related Content

What's hot

What's hot (20)

Similar to CBP PRE-ASSESSMENT IMPORT AUDIT QUESTIONNAIRE

Similar to CBP PRE-ASSESSMENT IMPORT AUDIT QUESTIONNAIRE (20)

More from Brent Claypool

More from Brent Claypool (6)

Recently uploaded

Recently uploaded (20)

CBP PRE-ASSESSMENT IMPORT AUDIT QUESTIONNAIRE

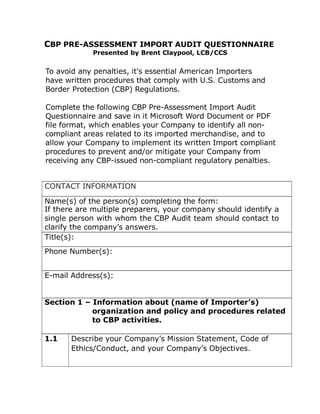

- 1. CBP PRE-ASSESSMENT IMPORT AUDIT QUESTIONNAIRE Presented by Brent Claypool, LCB/CCS To avoid any penalties, it's essential American Importers have written procedures that comply with U.S. Customs and Border Protection (CBP) Regulations. Complete the following CBP Pre-Assessment Import Audit Questionnaire and save in it Microsoft Word Document or PDF file format, which enables your Company to identify all non- compliant areas related to its imported merchandise, and to allow your Company to implement its written Import compliant procedures to prevent and/or mitigate your Company from receiving any CBP-issued non-compliant regulatory penalties. CONTACT INFORMATION Name(s) of the person(s) completing the form: If there are multiple preparers, your company should identify a single person with whom the CBP Audit team should contact to clarify the company’s answers. Title(s): Phone Number(s): E-mail Address(s): Section 1 – Information about (name of Importer’s) organization and policy and procedures related to CBP activities. 1.1 Describe your Company’s Mission Statement, Code of Ethics/Conduct, and your Company’s Objectives.

- 2. 1.1.1 How is the Mission Statement, Code of Ethics/Conduct, and your Company’s Objectives communicated within your organization? 1.2 Who is responsible for assessing the risks to achieving your Company’s Objectives? Identify if there is a sub- Group or individual responsible for assessing your Company’s risk for being non-compliant with CBP Laws and Regulations. 1.2.1 Describe how the Risk Assessment is accomplished. For example, identify when, how, and how often the Risk Assessment is performed, what information is used, and what tolerances your Company considers to be acceptable. 1.2.2 When was the last Risk Assessment your Company performed? Describe any significant changes that your Company made as a result of its last Risk Assessment. 1.3 Within your Company, who has the overall responsibility for ensuring compliance with CBP Laws and Regulations?

- 3. Identify if there is an import function or department and describe your Company’s chain of command (for example, identify to whom they report). If on the other hand your Company contracts its Import Compliance to a Customs Broker, Customs Consultant, or to another Outside Agent, identify them, and identify whom within your Company (for example, individuals or groups) is/are responsible for interacting with the Customs Broker, Customs Consultant, or to another Outside Agent (for example, providing information to them and monitoring their work). 1.3.1 If there is an import function or department, identify the following information: How is it staffed? Identify if an individual is assigned as the manager and identify the number of employees that report to them. How long has the manager been at his or her position? What are the manager’s responsibilities and how is the manager accountable? Identify if the manager is responsible for providing Weekly Activity Reports and describe any performance measures.

- 4. 1.3.2 If your Company’s Import Compliance is handled by a Customs Broker, Customs Consultant, or another Outside Agent (for example, your Company doesn’t have an import department), identify the following information: How long has your Company used the current Customs Broker, Customs Consultant, or another Outside Agent? Identify the processes your Company uses to com- municate information, and to monitor their work? Describe if your Company has a Written Agreement or Contract with its current Customs Broker, Customs Consultant, or another Outside Agent. 1.4 Whom at your Company is responsible for developing and maintaining the written policies and procedures implemented to ensure your Company’s import compliance with CBP Laws and Regulations? How frequent are your Company’s written policies and procedures updated?

- 5. Section 2 – Information about the valuation of imported merchandise. 2.1 What is the Appraisement method used in your Company’s imported merchandise valuation? 2.2 Who is responsible at your Company for transacting with its Foreign Vendors? Identify all Company individuals, groups, or departments that are responsible. 2.2.1 Describe how your Company negotiates its transactions with its Foreign Vendors? Identify all processes used and the applied conditions. 2.2.2 Describe the Terms of Sale used? If there are different Terms of Sale, identify the conditions for each Terms of Sale applied. 2.2.3 If applicable, describe the terms/conditions when your Company applies discounts or rebates?

- 6. 2.2.4 If applicable, describe any additional expenses such as Management Fees or Engineering Services that are separately billed by the Foreign Vendors? 2.2.5 What documentation shows the Terms of Sale and prices (for example, contracts, distribution and other similar agreements, invoices, purchase orders, bills of lading, proof of payment, correspondence between the parties, and Company reports or catalogs/brochures)? 2.3 Describe your Company’s accounting procedures for recording purchases and payments. What Company accounts are used to record purchases of Foreign merchandise? Identify or provide a list of Vendor Codes. What Company accounts are used to record payments made to Foreign Vendors? Describe the payment methods used (for example, wire transfer, letters of credit). 2.4 If applicable, what Company accounting data/reports are provided to the Company’s import function or department? Identify how often the Company data/reports are provided (for example, quarterly

- 7. reports of Price Adjustments for purchases from Foreign Vendors). For risk pertaining to related party transactions. 2.5 Describe the nature of the relationship between your Company and the related Foreign Vendor/Seller? Identify if your Company is the exclusive U.S. Importer. 2.5.1 Identify any financial arrangements (for example, loans, financial assistance, and expense reimbursement) between your Company and the Foreign Vendor/Seller? 2.5.2 If applicable, explain the terms and conditions of goods sold to your Company on consignment. 2.5.3 Describe how prices between your Company and the Foreign Vendor/Seller/Manufacturer are determined? Identify all sources of data used and, where appropriate, describe the applied accounting methodology or computational formulas. If Transaction Value is used, identify if your Company supports “circumstances of sale” or “test

- 8. values.” If applicable, provide the following information: Describe when Price Adjustments are made. Identify any additional expenses such as Management Fees or Engineering Services that are separately billed to your Company. 2.5.4 Explain how your Company accounts for its transactions? Identify if your Company maintains its own accounting books and records. 2.5.4.1 What are the intercompany accounts your Company uses? For risk pertaining to statutory additions. 2.6 Assists

- 9. 2.6.1 If applicable, identify the type of Assists that are provided to the Foreign Vendors for free or at a reduced cost (for example, tooling, hangtags, art or design work). 2.6.2 Within your company, who determines that the Assists will be provided? Identify all Company individuals, groups, or departments that are involved in the decision. When is it decided that the Assists will be provided? What Company accounts are used to record the costs of the Assists? 2.6.3 Describe the Company procedures used to ensure the Assist costs are included in the values declared to CBP. Identify whom at your Company decides how the actual Assist cost will be apportioned to the imported items, and also describe how the apportioned cost is tracked.

- 10. 2.7 Packing 2.7.1 If applicable, describe the Packing type (for example, Labor or Materials), Containers (exclusive of Instruments of International Traffic), and Coverings of whatever nature that is paid separately to the Vendor to put your Company’s imported merchandise in condition ready for shipment to the United States. 2.7.2 Whom at your Company determines that the Packing cost will be separately charged? Identify all Company individuals, groups, or departments that are involved in the decision. When is it decided that Packing cost will be separately charged? What Company accounts are used to record the costs of Packing, Containers, and Coverings? 2.7.3 Describe the Company procedures used to ensure the Packing cost is included in the declared values to CBP.

- 11. 2.8 Commissions 2.8.1 If applicable, identify the Terms of Sale with Foreign Vendors that require your Company to separately pay for “Selling Agent” Commissions. Identify the Vendors. 2.8.2 Whom at your Company determines that “Selling Agent” Commissions will be paid directly to the intermediary? When is it decided that the “Selling Agent” Com- missions will be paid directly to the intermediary? What Company accounts are used to record the payment of these Commissions? 2.8.3 Describe the Company procedures used to ensure these Commissions are included in the declared values to CBP.

- 12. 2.9 Royalty and License Fees 2.9.1 If applicable, describe the Terms of Sale with Foreign Vendors that require your Company to pay, directly or indirectly, any Royalty or License Fees related to the imported merchandise as a condition of the sale of the imported merchandise for exportation to the United States. Identify the Vendors. 2.9.2 Whom at your Company determines that Royalty or License Fees will be paid as a condition of the sale? When is it decided that Royalty or License Fees will be paid as a condition of the sale? What Company accounts are used to record the payment of the Royalty or License Fees related to imported merchandise?

- 13. 2.9.3 What Company procedures ensure that Royalty or License Fees are included in the declared values to CBP? 2.10 Proceeds of Any Subsequent Resale, Disposal, or Use 2.10.1 If applicable, describe any Company agreements with the Foreign Vendors where the proceeds of any Subsequent Resale, Disposal, or Use of the imported merchandise accrue directly or indirectly to the Foreign Vendor. Identify the Vendors. 2.10.2 Whom at your Company determines the proceeds of any Subsequent Resale, Disposal, or Use of the imported merchandise will accrue directly or indirectly to the Foreign Vendor? When is it decided the proceeds of any Subsequent Resale, Disposal, or use of the imported merchandise will accrue directly or indirectly to the Foreign Vendor? What Company accounts are used to record the payment of these proceeds?

- 14. 2.10.3 Describe the Company procedures used to ensure the proceeds of any Subsequent Resale, Disposal, or Use of the imported merchandise accruing directly or indirectly to the Foreign Vendor are included in the declared values to CBP. Section 3 – Information about the classification of imported merchandise. 3.1 Whom at your Company is responsible for determining how imported merchandise is classified? Identify all Company individuals or groups that are responsible. 3.1.1 What Company records and other information (for example, product specifications, engineering drawings, physical items, laboratory analyses, etc.) are used to determine the classification of merchandise? 3.2 Does your Company have a Classification Database? 3.2.1 If there is a Classification Database, does your Company archive previous versions of it? Identify how long previous versions are retained.

- 15. 3.2.2 If your Company has a Classification Database, is a copy provided to the Customs Broker? Indicate how it is provided to the Customs Broker. 3.2.3 If there is a Classification Database, what Company procedures ensure the information in the Database is accurate? Section 4 – Information about special classification provisions HTSUS Number 9801. 4.1 Describe the type of merchandise your Company imports under HTSUS Number 9801. 4.2 Whom at your Company determines that products of the United States will be returned after having been exported? Identify all Company individuals, groups, or departments that are involved in the process. When is it determined that products will be returned after having been exported?

- 16. What Company documentation/records are maintained for the exported items? 4.3 Describe the Company procedures that ensure the exported items have not been advanced in value or improved in condition by any manufacturing process or by other means while abroad. 4.4 Describe the Company procedures that ensure that Drawback has not been claimed for the exported items. Section 5 – Information about special classification provisions HTSUS Number 9802. 5.1 Describe the Company’s type of merchandise that is imported under HTSUS Number 9802. 5.2 What Company documentation or records are maintained for the exported items? 5.3 For items imported under HTSUS Number’s 9802.00.40 and 9802.0050: Identify the Company documentation or records that support the cost or value of the repair?

- 17. 5.4 Describe the Company procedures or methods (for example, unique identifiers) used to ensure the articles exported for repair or alterations are the same articles being re-imported. 5.5 For items imported under HTSUS Number’s 9802.00.40 and 9802.00.50: Identify the Company procedures that ensure the foreign operation (for example, repair or alteration process) does not result in the exported item becoming a commercially different article with new properties and characteristics. 5.6 Describe the Company procedures that ensure that Drawback has not been claimed for the exported items. Section 6 – Information about Generalized System of Preferences (GSP) / Free Trade Agreement (FTA). 6.1 If applicable, identify the Name and MID’s for all of the Foreign Vendors from whom items are imported under GSP/FTA.

- 18. 6.2 Describe any agreements with unrelated Foreign Vendors. Identify if the unrelated vendors are required to provide Cost and Production records to CBP, or instead, are legally prevented from releasing the records. 6.3 Describe the Company procedures used to ensure the origin of articles imported under GSP or the specific FTA is wholly the growth, product, or manufacture of one of the Beneficiary Developing Countries (BDC) or FTA Country? Identify whom at your Company performs the procedures, and when and how often the Company individual performs the procedures. 6.3.2 What Company documentation/records are verified? Identify if copies of the Company documentation/records are retained on file or can be obtained upon request. 6.4 Describe the Company procedures used to ensure the cost or value of the material produced in the BDC or FTA Country, plus the direct processing cost, is not less than 35 Percent of the appraised value of the articles at the time of entry into the United States? Identify all Company individuals and groups that perform the procedures, and when and how often the Company individuals and groups perform the procedures.

- 19. 6.4.1 What Company documentation/records are verified? Identify if copies of the Company documentation/records are retained on file or can be obtained upon request. 6.5 What Company documentation is maintained on file showing the articles are shipped directly from the BDC or FTA Country to the United States without passing through the territory of any other country, of if passing through the territory of any other country, that the articles did not entry the Retail Commerce of the other country? Section 7 – Information about North American Free Trade Agreement (NAFTA). 7.1 Whom at your Company is responsible for maintaining the certificates of origin from NAFTA Vendors? 7.2 Describe the Company procedures used to ensure the imported items are eligible for NAFTA? Section 8 – Information about Anti-Dumping (AD) / Countervailing Duties (CVD). 8.1 Whom at your Company determines that items may be subject to AD/CVD? Identify when and how often items are reviewed.

- 20. 8.1.1 What information is used to determine whether items may be subject to AD/CVD? Identify all Company individuals, groups, and departments that provide information and the documentation/records used. 8.2 Describe the Company procedures used to ensure the correct country of origin is identified for items subject to AD/CVD. 8.3 Describe the Company procedures used to ensure the correct AD/CVD Case Numbers are identified on the entry. Section 9 – Information about Intellectual Property Rights (IPR). 9.1 Identify all imported items for which your Company has authorizations from the IPR holders (for example, trade names, trademarks, or copyrights). Describe the item and identify the IPR type. 9.2 Whom at your Company determines that an imported item may have IPR belonging to other entities? Identify when and how often items are reviewed.

- 21. When is it decided that an imported item may have IPR belonging to other entities? What information is used to determine the items have IPR belonging to other entities? Identify all Company individuals, groups, or departments that provide information as well as the documentation/records used. 9.3 Describe the Company procedures used to ensure there is a valid Authorization/Agreement between your Company and the Owner of the trade name, trademark, copyright, or patent prior to the importation of the items? 9.4 What Company accounts are used to record royalties, proceeds, and indirect payments related to the use of the IPR?

- 22. CBP PRE-ASSESSEMENT IMPORT AUDIT DOCUMENTATION CHECKLIST Presented by Brent Claypool, LCB/CCS Related to the CBP Pre-Assessment Import Audit Questionnaire, and in case CBP requests it, American Importers should have the following Company Documentation of one copy each, both in PDF file format and also a printed hard copy. Item No. Documentation Description 1 Organizational Chart 2 Import Compliance Manual 3 Current General Ledger Working Trial Balance For the Previous Quarter 4 Written Accounting Procedures 5 Current notarized Import Customs Powers of Attorney