Slideshow: Analysis of Tax Provisions in the Grand Bargain

•

0 likes•121 views

A short presentation on why cutting the tax rate on pass-through income is misguided that further explains the issues raised in OCPP's issue brief "A Grandly Flawed Bargain"

Recommended

Recommended

More Related Content

What's hot

What's hot (19)

Viewers also liked

Viewers also liked (13)

Similar to Slideshow: Analysis of Tax Provisions in the Grand Bargain

Similar to Slideshow: Analysis of Tax Provisions in the Grand Bargain (20)

Recently uploaded

Recently uploaded (14)

Slideshow: Analysis of Tax Provisions in the Grand Bargain

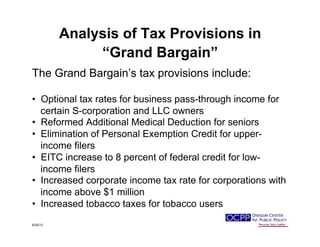

- 1. Analysis of Tax Provisions in “Grand Bargain” The Grand Bargain’s tax provisions include: • Optional tax rates for business pass-through income for certain S-corporation and LLC owners • Reformed Additional Medical Deduction for seniors • Elimination of Personal Exemption Credit for upper- income filers • EITC increase to 8 percent of federal credit for low- income filers • Increased corporate income tax rate for corporations with income above $1 million • Increased tobacco taxes for tobacco users 9/25/13

- 2. Will the tax provisions of the proposed Grand Bargain cover the costs for the proposed new investments in education, mental health care, and services for seniors? 9/25/13

- 3. Revenue to Pay for New Investments Shrinks After Current Budget $189 $50 $24 $0 $50 $100 $150 $200 $250 2013-15 2015-17 2017-19 Projected new revenue 9/25/13 Inmillions $201 million in new investments Source: Oregon Legislative Revenue Office

- 4. Business Pass-Through Income Subsidy is More Costly After Current Biennium -$38 -$205 -$239 -$300 -$250 -$200 -$150 -$100 -$50 $0 2013-15 2015-17 2017-19 9/25/13 ProjectedCostofSubsidyinmillions Source: Oregon Legislative Revenue Office

- 5. How do Oregonians at different levels of the income scale fare under the combined personal income tax (PIT) provisions of the proposed Grand Bargain tax changes? 9/25/13

- 6. Beneficiaries of Tax Cuts Are Roughly Evenly Distributed; Tax Increases Mainly Impact Higher End of Income Scale 0% 20% 40% 60% 80% 100% Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 Share with Tax Increase Share with Tax Cut Combined Impact of All PIT Provisions

- 7. Lion’s Share of the Tax Cut Goes to Some of the Top 1 Percent 0% 20% 40% 60% 80% 100% Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 Share of Tax Increase Share of Tax Cut Combined Impact of All PIT Provisions

- 8. For Top 1 Percent, Average Tax Cut Dwarfs Average Tax Increase $51 $27 $152 $328 $357 $573 $745 -$31 -$60 -$67 -$108 -$99 -$726 -$9,246-$10,000 -$8,000 -$6,000 -$4,000 -$2,000 $0 $2,000 Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 Average Increase for Those with Increase Average Cut for Those with Tax Cut

- 9. The Overall Average Tax Change is Negligible for All Except the Windfall for the Top 1 Percent -$8 -$15 -$16 $21 $49 $149 -$2,694-$3,000 -$2,000 -$1,000 $0 $1,000 Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 AverageTaxChange–AllTaxpayers Combined Impact of All PIT Provisions

- 10. Who benefits from the Grand Bargain’s business pass- through income tax subsidy? 9/25/13

- 11. Business Pass-Through Income Subsidy Is Mainly for Some at the Top 0% 20% 40% 60% 80% 100% Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 Optional Rates for Business Pass-Thru Income SharewithTaxCut

- 12. Average Savings for Someone in the Top 1 Percent Getting a Subsidy Is Over $6,000 $0 -$46 -$71 -$53 -$75 -$458 -$6,011 -$10,000 -$8,000 -$6,000 -$4,000 -$2,000 $0 Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 AverageCutforThoseReceivingaSubsidy Optional Rates for Business Pass-Thru Income

- 13. Most of the Total Tax Cut Goes to a Portion of the Top 1 Percent 0% 20% 40% 60% 80% 100% Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 Optional Rates for Business Pass-Thru Income ShareofTaxCut

- 14. Top 1 Percent Saves, on Average, about $3,300 $0 $0 -$3 -$3 -$8 -$113 -$3,298 -$10,000 -$8,000 -$6,000 -$4,000 -$2,000 $0 Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Source: Institute on Taxation and Economic Policy, September 2013 AverageTaxChange–AllTaxpayers Optional Rates for Business Pass-Thru Income

- 15. How would Oregonians at different levels of the income scale fare under the combined PIT provisions if the Grand Bargain did not include the business pass-through income tax subsidy? 9/25/13

- 16. Without Pass-Through Subsidy, Plan More Fair: Tax Increases Concentrated at the Top, Tax Cuts for Some Low- & Middle-Income Families 0% 20% 40% 60% 80% 100% Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Impact of PIT provisions, excluding pass-through business income rates. Source: Institute on Taxation and Economic Policy, September 2013 Share with Tax Increase Share with Tax Cut

- 17. Without Pass-Through Subsidy, Tax Changes Would Be More Closely Based on Ability to Pay 0% 20% 40% 60% 80% 100% Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Share of Tax IncreaseShare of Tax Cut Impact of PIT provisions, excluding pass-through business income rates. Source: Institute on Taxation and Economic Policy, September 2013

- 18. Without Pass-Through Subsidy, the Tax Cuts & Increases Are Fairly Modest for Everyone $51 $27 $153 $328 $357 $607 $629 -$31 -$60 -$64 -$118 -$140 -$153 $0 -$500 -$250 $0 $250 $500 $750 $1,000 Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 Average Increase for Those with Increase Average Cut for Those with Tax Cut Impact of PIT provisions, excluding pass-through business income rates. Source: Institute on Taxation and Economic Policy, September 2013

- 19. Without Pass-Through Subsidy, Average Overall Change Would Be Based on Ability to Pay -$8 -$15 -$13 $24 $58 $284 $614 -$500 -$250 $0 $250 $500 $750 $1,000 Lowest 20% Second 20% Middle 20% Fourth 20% Next 15% Next 4% Top 1% 9/25/13 AverageTaxChange–AllTaxpayers Impact of PIT provisions, excluding pass-through business income rates. Source: Institute on Taxation and Economic Policy, September 2013

- 20. Conclusion In its current form, after the current biennium the Grand Bargain’s tax package won’t deliver the money needed to pay for the proposed new investments in education, mental health care, and services for seniors. The cause of the sharp drop in revenue is the ballooning costs of business pass-through income provision, a subsidy that by-and- large only benefits some of Oregon’s wealthiest 1 percent. Eliminating the business pass-through income provision would retain revenue to pay for the new investments and make the package more equitable. 9/25/13