Alpha and Beta -Listed and Private Real Estate

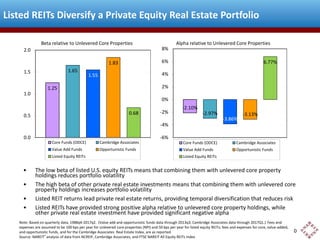

This chart shows beta and alpha (net of fees) for four types of real estate investment in the U.S. relative to an unlevered portfolio of core property investments (as measured by the NCREIF Property Index), calculated using quarterly net total returns data from NCREIF and from the FTSE NAREIT All Equity REITs Index. For an institutional investor that already has a portfolio of unlevered core properties, adding investments in private equity real estate funds has provided no real estate portfolio diversification benefit regardless of whether the new funds follow a core, value-add, or opportunistic strategy. Beta > 1 means that real estate portfolio volatility increases when any of those strategies is added to an existing portfolio of unlevered core properties, because private equity funds simply increase portfolio leverage; meanwhile, alpha>0 means that real estate portfolio returns decline on a risk-adjusted basis. In contrast, adding listed equity REIT investments reduces real estate portfolio volatility and increases risk-adjusted portfolio returns, with beta = 0.68 and (annualized) alpha = +6.77%. Measured returns to private real estate investments lag behind listed REIT returns by 4-5 quarters, so combining listed REITs with a private portfolio creates a "temporal diversification" benefit. Questions? Contact me at bcase@nareit.com.

Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

Alpha and Beta -Listed and Private Real Estate

- 1. Listed REITs Diversify a Private Equity Real Estate Portfolio Beta relative to Unlevered Core Properties 2.0 1.8 8% 1.83 1.6 4% 1.2 1.19 2% 0.8 0% 0.6 0.62 0.4 Core Funds (ODCE) Opportunistic Funds • • -2.13% -3.85% -3.13% -6% 0.0 • -2% -4% 0.2 • 8.41% 6% 1.55 1.4 1.0 Alpha relative to Unlevered Core Properties 10% Value Add Funds Listed Equity REITs Core Funds (ODCE) Opportunistic Funds Value Add Funds Listed Equity REITs The low beta of listed U.S. equity REITs means that combining them with unlevered core property holdings reduces portfolio volatility The high beta of other private real estate investments means that combining them with unlevered core property holdings increases portfolio volatility Listed REIT returns lead private real estate returns, providing temporal diversification that reduces risk Listed REITs have provided strong positive alpha relative to unlevered core property holdings, while other private real estate investment have provided significant negative alpha Note: Based on quarterly data, 1988q4-2013q3. Fees and expenses are assumed to be 100 bps per year for unlevered core properties (NPI) and 50 bps per year for listed equity REITs; fees and expenses for core, value-added, and opportunistic funds are as reported. Source: NAREIT® analysis of data from NCREIF and FTSE NAREIT All Equity REITs Index 0