Distribution of profits by joint stock companies

•

0 likes•106 views

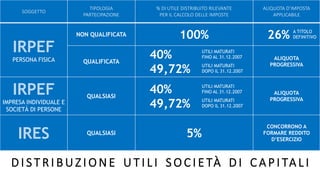

This document outlines the Italian tax treatment of distributions of profits by capital companies based on the type of recipient. For individuals, 100% of profits distributed are taxed at 26% for non-qualified shareholders, and 40% is taxed at progressive IRPEF rates for qualified shareholders. For sole proprietorships and partnerships, 40% of distributions are taxed at progressive IRPEF rates. For corporations, 5% of distributions contribute to taxable income with profits earned before December 31, 2007 taxed at the applicable IRES rate and profits earned after taxed at the regional tax on productive activities rate.

Recommended

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

Distribution of profits by joint stock companies

- 1. D I S T R I B U Z I O N E U T I L I S O C I E TÀ D I C A P I TA L I SOGGETTO TIPOLOGIA PARTECIPAZIONE % DI UTILE DISTRIBUITO RILEVANTE PER IL CALCOLO DELLE IMPOSTE ALIQUOTA D’IMPOSTA APPLICABILE IRPEF PERSONA FISICA NON QUALIFICATA 100% 26% QUALIFICATA 40% 49,72% ALIQUOTA PROGRESSIVA IRPEF IMPRESA INDIVIDUALE E SOCIETÀ DI PERSONE QUALSIASI 40% 49,72% ALIQUOTA PROGRESSIVA IRES QUALSIASI 5% CONCORRONO A FORMARE REDDITO D’ESERCIZIO UTILI MATURATI FINO AL 31.12.2007 UTILI MATURATI DOPO IL 31.12.2007 UTILI MATURATI FINO AL 31.12.2007 UTILI MATURATI DOPO IL 31.12.2007 A TITOLO DEFINITIVO