Why Glencore’s assets will fail to realize its true value

•Download as DOCX, PDF•

0 likes•263 views

Glencore is desperate to sell its assets and vowed to reduce net debt by $10bn. However, who will and at what price? A look into Glencore's Xstrata acquisition gives us some glimpse of what Glencore's assets are actually worth.

Recommended

More Related Content

Viewers also liked

Viewers also liked (16)

Similar to Why Glencore’s assets will fail to realize its true value

Similar to Why Glencore’s assets will fail to realize its true value (20)

More from Walter Hin

More from Walter Hin (8)

Recently uploaded

Recently uploaded (20)

Why Glencore’s assets will fail to realize its true value

- 1. Why Glencore’s assets will fail to realize its true value Prologue The company made headlines on Monday (28/09/15)when its shares fell by 30%. Management made assurances to investors they are raising cash and selling assets to reduce its gross debt of $50bn, which is more than the company’s market capitalisation. More:If you want to read my analysis on Glencore,the company, click on the link HERE. But today, we will be discussing Glencore biggest acquisition: Xstrata. Before we begin, here is some background on Glencore. Who is Glencore? A business that trade hard and softcommodities, it also mined natural resources and in 2013 merged with Xstrata at a costof $30bnfor the 66% stake Glencore doesn’t own. So on a 100% equity basis, Glencore values Xstrata’s stake at $44.6bn. Today, the market value of Glencore and Xstrata is valued at $26bn. Why have investors diluted the value of Glencore? At the time of acquisition, Ivan Glasenberg says operational cost-saving would be $2bn. But Glencore impaired $7.5bnof its assets and made a loss of $7.4bnin 2013.Also, the company paid out an extra $600m in interest costs from the previous year. Gross debt in 2013 jumped to $55bnfrom $35bn.

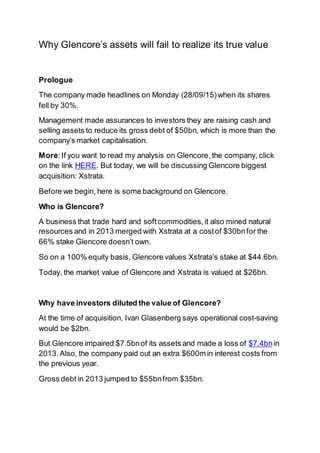

- 2. It means that Glencore’s debtto equity is exceeding 100%,which adds financial risk if company’s profits can’t covertheir capex, dividends and debt repayments. Glencore’s Xstrata problem However, Glencore’s management is no better than (previous) management at BHP Billiton and Rio Tinto. Both of which did acquisitions and share buyback at the wrong business cycle. For example, Rio bought Alcan for $38.1bnin 2008 but was forced to write off $25bnof its Alcan’s assets! At the time of the purchase, Alcan had revenue of $30bnin revenue and $2bn of earnings. BHP Billiton made the same mistake in 2011 when it bought Petrohawk (a gas company) for $12bn(debt + cash offer).In the end, they had to write-off $5.8bnof Petrohawk’s assets. At the time, BHP was paying 18 times Petrohawk’s EBITDA. Both Rio and BHP has written down between 66% and 48% of its investments respectively. Meanwhile, Glencore has written off 17% of Xstrata’s assets. But, will there be further writedowns from Xstrata? Xstrata – the business Xstrata’s four main commodities:Coal, copper,nickel and zinc accounts for 75% of its revenue. Let see the performance ofthese commodities.

- 3. Source:Xstrata annual report Coal has played a major role in contributing to Xstrata’s revenue while nickel and zinc stayed on the back foot.Copper stays on as the biggest contributor. By analysing Xstrata’s commodities EBIT marginvs. the commodity market price, we get the sense of direction of where the EBIT margin is heading. 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 2006 2007 2008 2009 2010 2011 2012 ($m) Xstrata's revenue breakdown Coal Copper Nickel Zinc

- 4. Source:Xstrata annual report Copper’s margins were falling even though the average selling price is high, meaning fixed operational costs have increased substantially since 2006.From 2012 onwards, the copperprice has dropped by27.3%. 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000 0 5 10 15 20 25 30 35 40 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 ($/TONNE) (%) Xstrata's copper EBIT margin Copper (%) Copper ($/tonne) 0 20 40 60 80 100 120 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 40.0 45.0 50.0 ($/TON) (%) Xstrata's coal EBIT margin Coal (%) S.A. thermal coal price ($/ton) Australian thermal coal price ($/ton)

- 5. Source:Xstrata annual report The EBIT margin for coal is even worse when prices touched their all- time high! This kind of situation happens because capacity utilisation has not reached its optimal level, especiallywhen the company is adding to capacity. Meaning that coal’s EBIT margin has to compensate forthe spare ‘unused’ capacity. Now, that coal prices have dropped onaverage by 40%, the EBIT margin will be significantly reduced. Source:Xstrata annual report 0 5,000 10,000 15,000 20,000 25,000 30,000 35,000 40,000 -5 0 5 10 15 20 25 30 35 40 45 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 ($/TONNE) (%) Xstrata's nickel EBIT margin Nickel (%) Nickel ($/ton)

- 6. Source:Xstrata annual report Both Nickel and Zinc plays a supporting role; nickel margin is likely to fall further, after the Glencore’s acquisition. But the margin on zinc is likely to be maintained, given its price resilience. Investors need to rememberthat heavily capital intensive industry needs to make a decentmargin if they are going to rely on internal funds to repay debtand pay a ‘sustainable’ level of dividends. More importantly, to maintain productionlevel, these types of businesses needto reinvest their ‘surplus’ capital. To know how much capital is required, one should look at their depreciationand amortisation (D + A) expenses peryear. If the company invest the equivalent of its (D + A), then they have maintained its production levels. For Xstrata, if we ignore net interest costs and corporate taxes, the amount of EBIT (earnings before tax and interest) it makes each year barely cover their Capital expenditure (see below): 0 500 1,000 1,500 2,000 2,500 3,000 3,500 0 5 10 15 20 25 30 35 40 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 ($/TON) (%) Xstrata's zinc EBIT Zinc (%) Zinc ($/ton)

- 7. Source:Xstrata annual report People would bash me for not including depreciationand amortisation charges. However, the above illustration should make retail investors that a highly capitalised business needs to make a decent margin to cover their CAPEX! Secondly,investors should be careful if businesses (especiallyhighly capitalized ones) talk about expansion. -2000 -1000 0 1000 2000 3000 4000 5000 2006 2007 2008 2009 2010 2011 2012 ($m) Xstatra's EBIT minus CAPEX breakdown Coal Copper Nickel Zinc

- 8. Source:Xstrata annual report In the case of Xstrata, it manages to double revenue in the last six years; however operating cash flow and net profit did not double! Lesson:If businesses rely on market prices for their fortune, it doesn’t possess any competitive advantages, apart from being labelled the ‘lowest costs producers’. Therefore,when management decides to expand the size of its operations, make sure that cash profit grows at the same pace as revenue. If we look at the free cash flow of Xstrata and compare this alongside its net operating cash flow and total debt we get this: 0 5 10 15 20 25 30 35 40 2006 2007 2008 2009 2010 2011 2012 ($bn) Revenue vs. net profit vs. cash profit Revenue Operating cash flow Net profit

- 9. Source:Xstrata annual report The chart tells us two things about Xstrata: 1. ‘Net operating cash flow’ from 2006 to 2012 ranges from $4bn-$9bn per annum equivalent to 20% to 35% of its revenue. And free cash flow after capex, acquisitions and disposalis negative! 2. Total debt increases when free cash flow is negative, exceptfor 2008/09 becausethey raised $5.7bnfrom shareholders.Otherwise, total debt would be $22bn, instead of $17bn. Will there be a further write down in Xstrata’s assets? Furthermore, Glencore will need to write down it’s Xstrata stake because margins would have deteriorated further as commoditiesprices dropped a further 30-40% (exceptzinc), since 2012. 0 2,000 4,000 6,000 8,000 10,000 12,000 14,000 16,000 18,000 -20,000 -15,000 -10,000 -5,000 0 5,000 10,000 15,000 2006 2007 2008 2009 2010 2011 2012 ($m) ($m) Xstrata's FCF vs. OCF Free cash flow ($m) Net operating cash flow ($m) Total debt ($m, RHS)

- 10. Glencore values its Xstrata stake at 13 times net earnings (Xstrata’s average net earnings is $3.53bnfrom 2006-2012),or 32 times 2012’s earnings. Giving the prolonged and persistentweakness in commodities prices,a write down of 50% of Xstrata's assets is appropriate. Because Glencore is desperate to raise cash from selling its assets to reduce its ‘mammoth’ $50bnof debt. Also, with weak persistentcommoditiesprices,assets held by miners will be less valuable. My conclusion on Glencore’s Xstrata stake would be a further write down of between$7bn and $15bn. However, the company has indicated they will be selling assets to raise cash, and it will be interesting how much they will get for their asset vs. how much they have valued it in their books!! Disclosure:I do not own any Glencore shares, but this could change if certain events occurred!