CFA RESEARCH CHALLENGE REPORT FINAL (Feb 9,2014)-TEAM G(1)

Cooper_Research_Notes

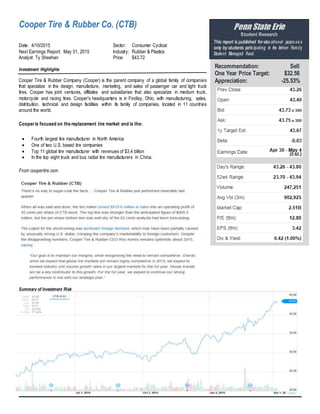

1. Cooper Tire & Rubber Co. (CTB)

Date: 4/10/2015 Sector: Consumer Cyclical

Next Earnings Report: May 01, 2015 Industry: Rubber & Plastics

Analyst: Ty Sheehan Price: $43.72

Investment Highlights

Cooper Tire & Rubber Company (Cooper) is the parent company of a global family of companies

that specialize in the design, manufacture, marketing, and sales of passenger car and light truck

tires. Cooper has joint ventures, affiliates and subsidiaries that also specialize in medium truck,

motorcycle and racing tires. Cooper's headquarters is in Findlay, Ohio, with manufacturing, sales,

distribution, technical and design facilities within its family of companies, located in 11 countries

around the world.

Cooperis focused on the replacement tire market and is the:

Fourth largest tire manufacturer in North America

One of two U.S. based tire companies

Top 11 global tire manufacturer with revenues of $3.4 billion

In the top eight truck and bus radial tire manufacturers in China.

From coopertire.com

Summary of Investment Risk

Penn State Erie

Student Research

This report is published foreducational purpose s

only by students participating in the Intrieri Family

Student Managed Fund.

Recommendation: Sell

One Year Price Target: $32.56

Appreciation: -25.53%

2. Penn State Erie - TheBehrend College 2

Cooper tires is a risky investment because the industry has so many large competitors as well as a high number of threats in terms of their revenue

stream that could really drive down their earnings. Manufacturing complexity is identified as a potential risk. With the overall health of people and the

world as a whole now being a priority to many people, it could impose some hard times for cooper and cost them a high amount of revenue. The all

time high stock price for Cooper over the last year was at $43.94 and it appears to continue this trend. Their performance has been on the rise for

some time now, but the future does not look as promising as the stock has been depreciating, which is why I recommend to sell.

Company Description

Management Credibility and Compensation

SUMMARY OF DISCOUNTED DIVIDEND /

EARNINGS VALUATION MEASURES

DDM with PE

Terminal Value $32.68

H-Model $39.40

Average $36.04

SUMMARY OF DISCOUNTED CASHFLOW

VALUATION MEASURES

Model Intrinsic Value

FCFE Two Stage $39.59

FCFE Two Stage

Declining $36.45

Average $38.02

SUMMARY OF COMPARABLES (RELATIVE)

VALUATION MEASURES

Industry Ration

Average $31.08

Industry PEG $ 16.13

Average $23.61

RECOMMENDATION Sell

Valuation Metrics: Summary from Valuation

Spreadsheets

Source: Yahoo Finance

3. Penn State Erie - TheBehrend College 3

Industry Overview and Competition

Cooper Tire & Rubber is really not a big player in this industry and is really behind the ball in terms of market share. Almost all ratios are very low

when staked up against the key competitors. The P/E ratio, P/B ratio, and P/S ratio are all above the industry average and the P/E ratio is almost

twice the industry average. Interest coverage, D/E, and med Oper. Margin % also show positive outcome. Overall, Cooper is not a very big player in

the market and serious changes need to be made if they want to be considered one of the top companies in the industry.

Investment Summary

4. Penn State Erie - TheBehrend College 4

The international operations, which were a notable disappointment during the fourth quarter, should remain a weak spot through 2015. Indeed,

overseas results will likely be hampered by volume softness in Western Europe, heightened volatility in Russia and Eastern Europe, and the loss of

key business in China, where the tire maker recently divested a large joint venture interest. These pressures from abroad ought to weigh on the top

line in the coming periods,

Offsetting modest growth in North America. The Americas segment is benefiting from higher sales of truck and bus radial tires, and from solid

demand for new, high-margined light truck products. And the improving macroeconomic backdrop is helping matters. Below the top line, meanwhile,

we see share net getting a boost from favorable raw material inputs—prices for oil, natural rubber, and synthetic rubber are all down markedly on a

year-over-year basis—and further stock repurchases. (Cooper’s board has just approved another $200 million for buybacks; under the previous $200

million repurchase plan, the company bought back 6.4 million shares at an average price of $31.49.) Thus, while a sales retreat in the high single-

digits is probable in 2015, we look for earnings to climb 15%, to around $2.90 a share. Next year, aided by a return to growth in the Asia/Pacific

region, the momentum should persist, with share net apt to reach the $3.30 level. The company intends to expand its Asian operations

aggressively in the years ahead. The Asian tire market is expected to increase nicely through late decade, so Cooper plans to go after this

business, even though its former joint venture in China performed unevenly and proved difficult to manage. This gives us reason to believe that

annual earnings growth of almost 10% is achievable out to the 2018-2020 period. Coopershares remain a timely (2) selection. Long-term

investors may wish to defer commitments, however, since the market already seems to be discounting much of the growth we envision here.

From Value Line