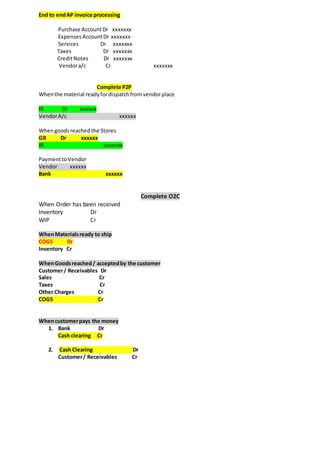

1. End to endAP invoice processing

Purchase AccountDr xxxxxxx

Expenses AccountDr xxxxxxx

Services Dr xxxxxxx

Taxes Dr xxxxxxx

CreditNotes Dr xxxxxxx

Vendora/c Cr xxxxxxx

Complete P2P

Whenthe material readyfordispatchfromvendorplace

IR Dr xxxxxx

VendorA/c xxxxxx

Whengoods reached the Stores

GR Dr xxxxxx

IR xxxxxxx

PaymenttoVendor

Vendor xxxxxx

Bank xxxxxx

Complete O2C

When Order has been received

Inventory Dr

WIP Cr

WhenMaterialsready to ship

COGS Dr

Inventory Cr

WhenGoodsreached/ acceptedby the customer

Customer/ Receivables Dr

Sales Cr

Taxes Cr

Other Charges Cr

COGS Cr

Whencustomerpays the money

1. Bank Dr

Cash clearing Cr

2. Cash Clearing Dr

Customer/ Receivables Cr

2. R2R Domain

Introduction :

Reconciliation means in ordinary meaning Understanding, Resolving, Reunion,

Comparing and / or equalizing the two set of data or two sets of reports. Identifying

the areas causing imbalance & substantiating the Variance causing the difference.

Exploring the ideas & ways to resolve the variance with a proper document support

for such variance to substantiate.

R2R is a skill of presenting or reporting the Reconciliations in a systematic way

which will contribute to the management decision making in the simplified and skillful

artistic manner. It may be redesigning the or reformatting the reporting structure or

upgrading to simplify the data presentation skills or any other skills contributing the

ease of managerial decision making.

Process Check in Point

The Reconciliation activity starts only after the transaction posting activity ceases.

The books of accounts closes for a particular period on/or after ending of the

transactions being posted in to books of Accounts. So that the end balances will be

uploaded to the reconciliation platform database. (it’s an Website)

The activity of closing posting the accounting entries is called as Period Closure in

accounting terminology.

The process indicators / Legends

The person performs or analyses the recon activity is called as Reconciliation

Analyst.

The base data to perform the reconciliation is called as Ledger Balances/ Account

Balance / GL Balances.

The transactions which are found active on the GL account and subject to be

reconciled are called as Open Items.

This GL balances being reconciled with the supportable balances.

Supportable balances means the sum of transactions for the particular period for

which the proper supporting docs available to substantiate / ratify / defend/ support

the transactions recorded on the books with adequate documentation with proper

approval levels and those are complied with Accounting policies & procedures and

Accounting practices are within the ambit / in accordance with the accounting

principles as whole.

The Reconciliation statement is being executed on MS-Excel Spread sheet and

subject to be uploaded on the GL Recon platform website with required comments

and explanations.

Reclassification means passing the necessary corrections on the books in terms of

3. principles and doc proof available and ensure that those are at par with the

document proof of such transaction recorded.

The variances means the disputed balances comprising the transactions which are

out of the scope of Accounting policies & procedures and out of the accounting

practices or these transactions does not / may not comply with the the accounting

proper accounting principles

Process in detail

The Balance sheet Accounts (GL Accounts) are subject to be reconciled.

.the end balances (period end balances) are reflected on the BS sheet GL Accounts

which will be carried forward for the next financial period. (Assets & Liabilities).

1. The end balances being reflected on the GL Reconciliation platform website.

2. The Reconciliation Analyst will ascertain & categorizes the end balances

according to the nature & feature of the GL account, such as AP GL accounts

/ AR GL Accounts / Assets GL Account / Liabilities GL Account The Asset &

Liabilities is meant in broader sense comprising all types of Asset & Liabilities

Account including for prepaid expenses, Outstanding Expenses and revenue

recognition accounts including payroll related accrual accounts.

3. Download YTD statement of GL Account from SAP at the transaction level by

enlisting all the document numbers on the particular GL account from

beginning till the end of the particular accounting period.

4. Check the each transaction recorded by cross verifying those with the copy of

the invoice / debit /credit notes / payment advice / copy of the receipt or any

other document proof upon which the particular transaction has been

recorded.

5. Verify the authenticity of each transaction in terms of approval / validity of the

transactions upon its compliance with the company’s policies & accounting

procedures & guidelines.

6. Validate the accounting principles as to the nature & features of the GL

Account on which the particular transaction has been recorded.

7. In case of need as per the accepted guidelines advice the necessary

rectification entries from the operational executive concerned.

8. Identify whether the features & nature of GL account complies with the nature

& feature transactions recorded in it. Or vice versa including the accounting

principles as well. Check whether the debits & credits recorded are

appropriate.

4. 9. In case the transactions deviating the any of points explained above. List

them out separately. Such transactions become variants & need to show them

as variances.

10.Perform the account clear for the completed transactions means where the

debit transaction is available for a credit or vice versa. Ensure that these

transactions also comply with all the above check points.

11. Once the supportable balance ascertainment task is completed. Cross verify

the end balances listed on the recon platform website, with the GL Account

closing balances available on SAP. Ensure that the month end balances and

GL balances at the period end as per SAP agrees with a zero output.

12.In case any of the GL account balances found variance explore the reason for

such variance explain them with proper reasons

13. Age the variances as per the aging buckets 30 / 60 / 90/ 180 / 360 / above

and show the action plans as per the company’s GL account recon guidelines

provided by the Finance controller or the Corporate Accounting Head (CFO).

14.The explanation need to be provided for each variances at the GL account

level on the recon platform website.

15.In case the supportable documents not available for any of the transactions of

a particular GL Account, need to show that as Un-Reconciled

16. Perform the thorugh check on each GL account level as to GL of the

reconciliation activity has been completed in all respect for each of the GL

Account. Ensure that the required parameters have been complied the

supportable balance availability, showing the variances, clearing the

variances if any. Explaining the variances, Aging action plan and the other

information if any and as per the case may be.

17.At the end forward each of the recons to the supervisor / TL / Manager / next

level of approver at each GL Account level after all the recon statements have

been uploaded on the website including comments & remarks for each of the

GL account found on the Recon platform.

Post Reconciliation activity

Follow-up with the required operational executory point s or the escalation points as

per recon guidelines provided by the client or clients corporate Accounting team or

5. by any the officer deligated to do act upon as authrised by the client head. (CFO /

Head of )Corporate Accounting Team.

Organise the meetings and set up the telephone calls to resolve the variance in

stipulated time as per open item aging.

Escalate to the higher level as per the guidelines on the escalation matrix.

Endeavor & take ownership

Undertake all types of genuine actions and try a max to clear the open items and

keep the each account in tact in all respects within ambit of client’s corporate

accounting & reconciliation policy. Watch the ammendments to the corporate

accounting policies guidelines, notifications or circulars which will be amended on

frequent intervals.

The End

~~~~~~~*******~~~~~~~