1. 1

International Accounting

Summer 2021

Final Exam (150 points) – A

Intake 60 Student order #: __14__ Student ID #: ___11186267____________

Name:_____Vu Thuy Duong_____

Last Name) (First Name)

Notes:

1. Please, “print” your name.

2. You MUST sign on the following statements.

“I verify that this exam contains entirely my own work. I have not inappropriately

consulted with any other person or unapproved materials in completing this exam.”

Signature: ___Vu Thuy Duong________ Date:___11/6/2021_______

3. Exam time is 120 minutes. The completed exam must be uploaded to the LMS

by 3:00 PM.

4. Keep your computer camera ON during the exam so that the professor(s) can

proctor the exam effectively.

5. For the multiple choice questions, please choose the one BEST answer on the

answer sheet below.

6. For the problem type questions, please answer clearly and legibly. (please

PRINT your answers)

7. This exam consists of 10 pages. Before solving the problems, please make sure

your exam contains all the pages.

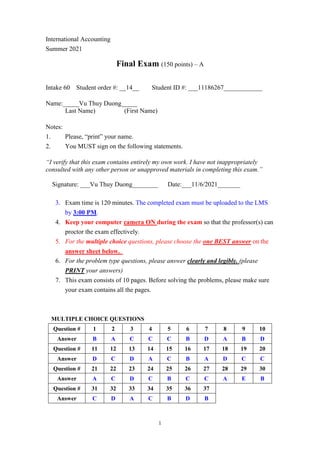

MULTIPLE CHOICE QUESTIONS

Question # 1 2 3 4 5 6 7 8 9 10

Answer B A C C C B D A B D

Question # 11 12 13 14 15 16 17 18 19 20

Answer D C D A C B A D C C

Question # 21 22 23 24 25 26 27 28 29 30

Answer A C D C B C C A E B

Question # 31 32 33 34 35 36 37

Answer C D A C B D B

2. 2

MULTIPLE CHOICE QUESTIONS (3 points each)

1. The term "provision" as it is used in IAS 37, is most closely related to what term in U.S.

GAAP?

A. Contingent liability, where the outflow of resources is "remote."

B. Contingent liability, where the outflow of resources is "probable."

C. Current liability, where the outflow is difficult to measure.

D. Reserve for bad debt, where the amount recoverable is "uncertain."

2. According to IAS 37, how should contingent assets be recognized?

A. They should be disclosed in the notes to the financial statements if the inflow of resources is

probable.

B. They should be recognized like any other asset, with a debit to "contingent assets."

C. They should not be disclosed anywhere in the financial statements due to their uncertainty.

D. They should only be disclosed in the notes to the financial statements if the inflows of

resources are virtually certain.

3. Under IAS 37, inflows of resources that are "virtually certain" to be received should be:

A. disclosed as contingent assets in the notes to the financial statements.

B. undisclosed until management is absolutely certain that resources will be received.

C. recognized as assets.

D. reported only in the cash flow statement.

4. Which of the following methods for translating foreign currency financial statements is

required under IAS 21?

A. Current rate method.

B. Temporal method.

C. Current rate method or temporal method, depending on the functional currency of the

subsidiary.

D. Current rate method or temporal method must be chosen by management of the parent.

5. How does IFRS require the past (or prior) service cost related to retirees to be recognized?

A. Don't recognize at all

B. Amortize over the average remaining working lives of active employees

C. Amortize over remaining expected life of the retirees

D. Recognize immediately

6. Under IASB standard, on which of the following dates is a public entity required to measure

the cost of employee services in exchange for an award of equity interests, based on the fair

market value of the award?

A. Date of vesting

B. Date of grant

C. Date of restriction lapse

D. Date of exercise

7. Which of the following represents a difference in the classification of current liabilities

between IFRS and U.S. GAAP?

A. Refinanced short-term debt

B. Amounts payable on demand due to violation of debt covenants

C. Bank overdrafts

D. All of the above

3. 3

8. Which of the following is a difference between IAS 37 and U.S. GAAP with respect to

restructuring provisions?

A. U.S. GAAP does not allow recognition of a restructuring provision until a liability has been

incurred.

B. There is no difference between IAS 37 and U.S. GAAP with respect to restructuring

provisions.

C. IAS 37 does not allow recognition of a restructuring provision until a liability has been

incurred.

D. A restructuring provision and related loss is more likely to occur later under IAS 37 than

under U.S. GAAP.

9. Under IFRS 2, Share-based Payment, what approach is used to account for the transaction?

A. Comparable transaction approach

B. Fair value approach

C. Market approach

D. Notional value approach

10. How does U.S. GAAP differ from IFRS with respect to cash-settled share-based payments?

A. U.S. GAAP always treats such payments as a liability.

B. U.S. GAAP offers the option to treat such payments as either a liability or equity.

C. IFRS and U.S. GAAP follow the same approach with respect to such payments.

D. U.S. GAAP, under certain circumstances, may treat such payments as equity.

11. The FASB requires that compensation expense be measured using one of several option

pricing models that deal with the following factors. Which of the following factors has inverse

relation with the fair value of stock option?

A. Expected term of the option.

B. Current market price of the stock.

C. Expected risk-free rate of return.

D. Exercise price of the option.

E. Expected volatility of the stock.

12. White Company is a calendar-year firm with operations in several countries. At January 1,

2013, the company had issued 160,000 executive stock options permitting executives to buy

80,000 shares of stock for $25. The vesting schedule is 20% the first year, 30% the second year,

and 50% the third year (graded-vesting). The fair value of the options is estimated as follows:

Under the graded-vesting method, what is the compensation expense related to the options to be

recorded in 2014? https://brainly.com/question/15822316

A. $96,000

B. $192,000

C. $256,000

D. $280,000

E. $512,000

13. Under IAS 12, Income Taxes, which of the following issues are covered?

A. Temporary differences

B. Operating loss carry forwards

C. Tax credit carry forwards

D. All of the above

4. 4

14. Under IAS 12, current and deferred taxes are measured on the basis of:

A. rates that have been enacted or substantively enacted by the balance sheet date.

B. current rates and rates anticipated when temporary differences reverse.

C. rates anticipated when temporary differences reverse.

D. rates prevailing when the entity provided goods or services.

15. What kinds of temporary differences related to income taxes can arise under IFRS that don't

occur under U.S. GAAP?

A. Book and tax differences related to the amortization of property, plant, and equipment for

book purposes and cost method for tax purposes.

B. Book and tax differences related to the calculation of impairments for book purposes with

adjustment for tax purposes.

C. Book and tax differences related to the revaluation of property, plant, and equipment for

book purposes and cost method for tax purposes.

D. Book and tax differences related to the calculation of contingent liability for book purposes

with no like adjustment for tax purposes.

16. Under IAS 1, Presentation of Financial Statements, how must deferred taxes be classified on

the balance sheet?

A. As either a current asset or a current liability

B. As always a noncurrent asset or a noncurrent liability

C. As either a current or noncurrent asset or liability based on the expected timing of realization

D. As a separately stated positive or negative component of equity

17. Under IFRS 15, which of the following is NOT a condition that must be met in order for

revenue from the sale of goods to be recognized?

A. There must be a binding, written contract between the seller and the buyer.

B. The significant risks and rewards of ownership of the goods have been transferred to the

buyer.

C. The amount of revenue can be measured reliably.

D. Neither continued managerial involvement normally associated with ownership nor effective

control of the goods is retained.

18. Under IFRS 15, which of the following is an example of retention of significant risks and

rewards by the seller?

A. The buyer has no right to rescind the purchase.

B. The seller is under no obligation for satisfactory performance not covered by normal

warranties.

C. Goods are sold subject to installation, but installation is not a significant part of the contract

and has not yet been completed.

D. Receipt of revenue by the seller is contingent on the buyer generating revenue through its

sale of the goods.

19. What is true about both IFRS and U.S. GAAP with respect to service contracts?

A. IFRS and U.S. GAAP both allow the use of the percentage-of-completion method.

B. Neither IFRS, nor U.S. GAAP allows the use of the percentage-of-completion method.

C. IFRS allows the use of the percentage-of-completion method while U.S. GAAP does not.

D. U.S. GAAP allows the use of the percentage-of-completion method while IFRS does not.

20. IAS 32 defines a financial instrument as:

A. the currency of a foreign country in which the enterprise does business.

B. a certified check.

C. any contract that gives rise to a financial asset of one entity and a financial liability or equity

instrument of another entity.

D. a recognized stock exchange.

5. 5

21. Under IAS 39, Financial Instruments: Recognition and Measurement, which of the

following is NOT a category into which a financial asset must be classified?

A. Property, plant, and equipment

B. Held-to-maturity investments

C. Loans and receivables

D. Available-for-sale financial assets

22. Under U.S. GAAP, a deferred tax asset must be realized when:

A. realization is probable.

B. realization is possible.

C. realization is more likely than not.

D. realization is greater than 75% likely.

23. Why is investing in foreign companies an effective way to diversify an individual's

investment portfolio?

A. Foreign economies are stronger than the Vietnamese economy.

B. Foreign stocks are less risky than the stocks of Vietnamese corporations.

C. Stock returns of companies in foreign companies are highly correlated with stock returns of

Vietnamese companies.

D. Returns on foreign company stocks do not always change in the same direction as returns on

Vietnamese stocks.

24. Which is NOT one of the basic steps in financial statement analysis?

A. Prospective analysis

B. Accounting analysis

C. Translation analysis

D. Financial analysis

25. Which of the following is true about financial statement disclosure?

A. When account balances are aggregated, the analyst has the greatest amount of information.

B. The amount and types of financial statement disclosure vary widely from one country to

another.

C. The concept of full disclosure has been universally adopted around the world.

D. An analyst can always disaggregate financial statement disclosures to obtain needed

information.

26. What is the best short-term solution to alleviate problems of financial statement analysis

arising from international differences in accounting terminology?

A. Require all countries to conform to IASB standards.

B. Create standard financial statement terminology for all companies around the world.

C. Analysts should carefully read the notes to financial statements and learn about the business

environments of countries they analyze.

D. Convert all financial statements into English.

27. On what SEC form must foreign corporations with shares listed on U.S. stock exchanges

present a reconciliation of net income and stockholders' equity to U.S. GAAP?

A. Form 10-Q

B. Form 10-K

C. Form 20-F

D. Form 8-Q

28. How is preferred stock reported for IFRS when it is redeemable at the option of the

shareholders?

A. As a liability

B. As equity

C. As mezzanine equity

6. 6

D. As temporary equity

E. None of the above

29. Compared to balance sheet information, income statement information has been relatively

more important and informative in

A. France

B. Mexico

C. Japan

D. Germany

E. United States

30. The corporate social reporting (CSR) theory that environmental disclosures are made in

response to a demand for environmental and social information is called the:

A. legitimacy theory.

B. stakeholder theory.

C. superfund theory.

D. depletable resource theory.

31. Triple bottom line (TBL) reporting is prepared on the basis of the following three bottom

limes EXCEPT:

A. Economic bottom line

B. Environmental bottom line

C. Accounting bottom line

D. Social bottom line

32. All of the following data may be needed to determine the fair value of a forward contract at

any point in time except

A. A discount rate.

B. The forward rate when the forward contract was entered into.

C. The current forward rate for a contract that matures on the same date as the forward contract

entered into.

D. The future spot rate.

E. All of the above data needed determine the fair value of a forward contract

33. Car Corp. (a U.S.-based company) sold parts to a Japanese customer on December 1, 2020,

with payment of 10 million Japanese yen to be received on January 31, 2021. The following

exchange rates applied:

Assuming a forward contract was entered into, what would be the net impact on Car Corp.'s

2020 income statement related to this foreign currency transaction? Assume an annual interest

rate of 12% and a fair value hedge. The present value for one month at 12% is .9901.

A. $ 295.05 (loss).

B. $ 300 (gain).

C. $ 300 (loss).

D. $ 700 (gain).

E. $ 700 (loss).

Forward

Spot Rate

Date Rate To 01/31/21

December 1, 2020 $ .00090 $ .00093

December 31, 2020 .00092 .00098

January 31, 2021 .00095 .00095

7. 7

34. What is a "strike price?"

A. The exchange rate that is used to buy a foreign currency today

B. The price that will be paid for goods in a forward contract

C. The exchange rate that will be used if a foreign currency option is executed

D. The difference between the wholesale rate and the retail rate for foreign currency exchange

35. What is the primary difference between a cash flow hedge and a fair value hedge?

A. The fair value hedge must completely offset the variability in the cash flow from the foreign

currency receivable or payable.

B. The cash flow hedge must completely offset the variability in cash flow from the foreign

currency receivable or payable.

C. The cash flow hedge can only be used to offset potential foreign currency losses on accounts

receivable.

D. The fair value hedge can only be used to offset the variability in cash flow from long-term

fixed assets related to foreign currency fluctuations.

36. Which of the following methods for translating foreign currency financial statements

attempts to produce consolidated financial statements as if a foreign subsidiary had actually

used the parent company's currency for all its transactions?

A. Current/Noncurrent method

B. Monetary/Nonmonetary method

C. Current rate method

D. Temporal method

37. IFRS defines functional currency as:

A. the currency of the parent company.

B. the currency of the primary economic environment in which the subsidiary operates.

C. the currency of the primary economic environment in which the parent operates.

D. the currency used by a subsidiary for its financial reporting.

8. 8

PROBLEMS

38. As of December 31, 20X9, Foresyte Corp. holds an asset with a cost of 140 and accumulated

depreciation of 56 for book and 98 for tax. The asset has been revalued to 100 for book purposes and

the following journal entry has been recorded. 105 chap 5

Accumulated depreciation 56

Plant 40

Equity – Asset revaluation surplus 16

No adjustment has been made for deferred tax during the current year. As of December 31, 20X8, a

deferred tax liability of 6.3 had been recorded.

a. Determine the appropriate journal entry to record the income tax effect for US GAAP, using the

tax rate of 30%. (5 points)

Book base: 84 (140-56)

Tax base: 42 (140-98)

Temporary difference: 42 (84-42)

42 book/ tax difference x30% = 12.6 deferred tax liability

12.6 deferred tax liability - 6.3 recorded at the beginning of the year

= 6.3 adjustment to be recorded to deferred tax liability

Journal entry

Income tax expense 6.3

Deferred tax liability 6.3

b. Determine the appropriate journal entry to record the income tax effect for IFRS, using the tax

rate of 30%. (5 points)

Entry to asset revaluation surplus account could be the net of tax 16 x 30%=4.8

Book base (after revaluation): 100

Tax base: 42 (140-98)

Temporary difference: 58 (100-42)

58 book/ tax difference x30% = 17.4 deferred tax liability

17.4 deferred tax liability - 6.3 recorded at the beginning of the year

= 11.1 adjustment to be recorded to deferred tax liability

11.1 adjustment to be recorded to deferred tax liability- 4.8 (16x30%) adjustment to

revaluation surplus during the year

= 6.3 entry to income tax expense

Journal entry

Equity- Asset revaluation surplus 4.8

9. 9

Income tax expense 6.3

Deferred tax liability 11.1

39. Northridge Inc, sells $2,700,000 face value of convertible bonds at a price of 101. Northridge realizes

proceeds of $2,727,000. The ten-year bonds carry an interest rate (coupon rate) of 6% with interest paid

semi-annually. The market rate for equivalent non-convertible bonds is 8%. The convertibility feature is

not separable from the bonds. The fair value of the bond component is $2,333,062 determined as follows:

PV of principal repayment $ 1,232,245

PV of interest payments $ 1,100,817

Fair Value of bond at 8% $ 2,333,062

a. Show the journal entry to record the issuance of the convertible bonds under the US GAAP.

(5 points)

128 ch 5

Cash $2,727,000

Convertible bonds payable $2,700,000

Premium on CB payable $27,000

b. Show the journal entry to record the issuance of the convertible bonds under the IFRS.

(5 points)

Cash $2,727,000

Convertible bonds payable $ 2,333,062

Premium on convertible features (equity) $393,938

40. On 12/1/21, Northridge Co., a U.S. machine manufacturer, sells machines to York Co., a British

company, for 100,000 British Pound (£) on credit. Payment is due in 90 days (March 1, 2022). The

current exchange rate is £1 = $1.60 on 12/1/21. Northridge Co. signs a 90-day forward contract with

Wells Fargo Bank to deliver £100,000 and the 90-day forward rate is £1 = $1.50 on 12/1/21.

10. 10

On Northridge Co’s fiscal year ends, 12/31/21, spot rate is £1 = $1.70 and available forward rate to

March 1, 2022 is £1 = $1.65. Northridge Co. uses a 12% discount rate. On 3/1/22, both the original

receivable and the forward contract come due. The exchange rate is £1= $1.40 on 3/1/22.

Using Cash Flow Hedge method, prepare Northridge Co.’s all journal entries for 12/1/21, 12/31/21, and

3/1/22. (19 points)

Accounts Receivable Forward Value

Spot Rate (£1) Value Changes Forward rate FV Changes

12/1/2021 $1.60 $160,000 $160,000 $1.50 0 0

12/31/2021 $1.70 $170,000 $10,000 $1.65 ($14,704) ($14,704)

3/1/2022 $1.40 $140,000 ($30,000) $1.40 $10,000 $24,704

21 chap 6

12/1/21

Accounts Receivable (£) $160,000

Sales $160,000

12/31/21

Accounts Receivable (£) $10,000

Foreign Exchange Gain $10,000

Loss on Forward Contract $10,000

AOCI $10,000

(Accumulated Other Comprehensive Income)

AOCI $14,704

Forward Contract $14,074

Discount Expense $3,405

AOCI $3,405

(r= 1- 3√ (150000/160000)

= 0.0212831

$160,000×0.0212831=$3,405)

3/1/22

Foreign Exchange Loss $30,000

Accounts Receivable (£) $30,000

AOCI $30,000

Gain on Forward Contract $30,000

Forward Contract $24,704

AOCI $24,704

Discount Expense $6,667

AOCI $6,667

Foreign Currency (£) $140,000

Accounts Receivable (£) $140,000

Cash $150,000

Foreign Currency (£) $140,000

Forward Contract $10,000