THE SILVER-COPPER SUPER-CYCLE: SilverSqueeze NOW CopperCrunch NEXT

MMG_030506

1. May 6, 2003

THE SOURCE OF INDEPENDENT EQUITY RESEARCH™

Analyst: Chris Rockingham, M.Sc., P. Geo.

Independent Equity Research Corp. 130 Adelaide St. W, Suite 2215, Toronto Ont., Canada M5H 3P5, www.eresearch.ca

MacMillan Gold Corp.

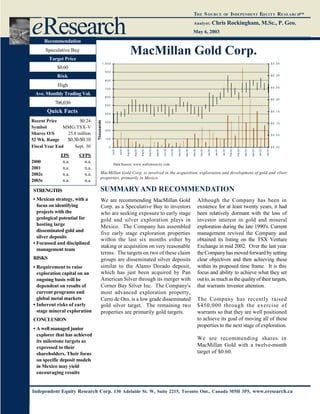

Recent Price $0.24

Symbol MMG:TSX-V

Shares O/S 25.8 million

52 Wk. Range $0.30-$0.10

Fiscal Year End Sept. 30

EPS CFPS

2000 n.a. n.a.

2001 n.a. n.a.

2002e n.a. n.a.

2003e n.a. n.a.

eResearch

Data Source: www.wallstreetcity.com

Recommendation

Speculative Buy

Target Price

$0.60

Risk

High

Ave. Monthly Trading Vol.

706,030

Quick Facts

STRENGTHS

• Mexican strategy, with a

focus on identifying

projects with the

geological potential for

hosting large

disseminated gold and

silver deposits

• Focussed and disciplined

management team

RISKS

• Requirement to raise

exploration capital on an

ongoing basis will be

dependent on results of

current programs and

global metal markets

• Inherent risks of early

stage mineral exploration

CONCLUSION

• A well managed junior

explorer that has achieved

its milestone targets as

expressed to their

shareholders. Their focus

on specific deposit models

in Mexico may yield

encouraging results

We are recommending MacMillan Gold

Corp. as a Speculative Buy to investors

who are seeking exposure to early stage

gold and silver exploration plays in

Mexico. The Company has assembled

five early stage exploration properties

within the last six months either by

staking or acquisition on very reasonable

terms. The targets on two of these claim

groups are disseminated silver deposits

similar to the Alamo Dorado deposit,

which has just been acquired by Pan

American Silver through its merger with

Corner Bay Silver Inc. The Company's

most advanced exploration property,

Cerro de Oro, is a low grade disseminated

gold silver target. The remaining two

properties are primarily gold targets.

Although the Company has been in

existence for at least twenty years, it had

been relatively dormant with the loss of

investor interest in gold and mineral

exploration during the late 1990's. Current

management revived the Company and

obtained its listing on the TSX Venture

Exchange in mid 2002. Over the last year

theCompanyhasmovedforwardbysetting

clear objectives and then achieving these

within its proposed time frame. It is this

focus and ability to achieve what they set

outto,asmuchasthequalityoftheirtargets,

that warrants investor attention.

The Company has recently raised

$450,000 through the exercise of

warrants so that they are well positioned

to achieve its goal of moving all of these

properties to the next stage of exploration.

We are recommending shares in

MacMillan Gold with a twelve-month

target of $0.60.

SUMMARYAND RECOMMENDATION

MacMillan Gold Corp. is involved in the acquisition, exploration and development of gold and silver

properties, primarily in Mexico.

0

1 0 0

2 0 0

3 0 0

4 0 0

5 0 0

6 0 0

7 0 0

8 0 0

9 0 0

1 , 0 0 0

Jul-02

Jul-02

Aug-02

Aug-02

Aug-02

Sep-02

Sep-02

Oct-02

Oct-02

Nov-02

Nov-02

Dec-02

Dec-02

Jan-03

Jan-03

Jan-03

Feb-03

Feb-03

Mar-03

Mar-03

Apr-03

Apr-03

Thousands

$ 0 . 0 0

$ 0 . 0 5

$ 0 . 1 0

$ 0 . 1 5

$ 0 . 2 0

$ 0 . 2 5

$ 0 . 3 0

$ 0 . 3 5

2. eResearch MacMillan Gold Corp.

2 May 6, 2003

THE COMPANY

MacMillan Gold Corp. is a Toronto based exploration company that has recently been

revived from a period of relative inactivity. Current management took over the Company

in 2001 with the objective of obtaining a TSX Venture Exchange listing. To this end

they raised the required working capital in the first quarter of last year, commissioned

the required independent third party report on their property of merit in Peru, and

achieved the desired listing by mid 2002. At this time the Company took the opportunity

to restructure the Board of Directors and review its overall strategy. Based partially on

the success of Corner Bay and its discovery of a relatively low grade, but metallurgically

attractive, disseminated silver deposit, management concluded that these targets were

worth exploring for, and that Mexico was an attractive environment. Since that decision

management has engaged experienced and respected people from the Mexican mining

community to act as local representatives and an experienced and capable geologist/

exploration manager to serve as Vice President, Exploration.

This combination has led to the examination of numerous properties with very specific

selection criteria. Five of the examined properties have now been acquired and the

Company is ready to move to the next stage. Concurrent with these activities the Company

has raised capital through a series of inexpensive private placements at or above the

current market price at the same time as it has minimized administrative costs.

During this quarter the Company plans to file an Annual Information Form. This will

allow it to have shorter time restrictions on future financings, as well as providing

much more technical information to shareholders.

MacMillan Gold Corp.

Mr. George Brown

36 Blue Jays Way

Suite 528

Toronto, ON

M5V 3T3 Canada

Phone: 416-867-1101

Fax: 416-867-1222

www.macmillangold.com

3. eResearchMacMillan Gold Corp.

3May 6, 2003

PROJECTS

Cerro de Oro Project (Figure 1)

Figure 1. Property Location Map

Source: Company reports

Figure 2. Cerro de Oro, Geological Setting

Source: Company reports

4. eResearch MacMillan Gold Corp.

4 May 6, 2003

The property is located 90 km south west of Saltillo in the northern part of the state

of Zacatecas, Mexico and eight km west south-west of the Concepcion del Oro base

and precious metal mine. Concepcion del Oro has been operating for many years and

produced over 40 million tons of base and precious metal mineralization. Current

reserves are a further eight million tons of lead zinc and silver mineralization and 40

million tons of gold and copper skarn type mineralization. The Cerro de Oro property

(2,263 hectares) is held through a number of agreements with various parties. The

largest land package is an Option held through Peñoles, one of Mexico's largest mining

companies. The agreement calls for exploration expenditures of US$ 500,000 and

option payments of US$ 70,000 over a four year period in order to earn 100% subject

to a 3% Net Smelter Return. The largest work commitments and payments are in the

latter years by which time the Company should have a good idea if its exploration

concept was valid and whether or not there is any kind of economic resource. Two

other smaller parts of the property were held by the estate of the former miner and

current ranchers. MacMillan Gold has been able to acquire rights to these for combined

option payments of US$ 21,000 over four years. At the same time the Company has

entered into a land use agreement with the owner of the surface rights, something

that is not always easy to conclude in Mexico.

Geologically the property is centered on a 3.5 km wide Eocene (33-55 million years

old) rhyodacite complex that has at least four phases with differing composition and

varying degrees of alteration and brecciation. This is younger than and different from

the rocks at the nearby Concepcion del Oro and Providencia mines, but is the same

age and rock type as the rocks at Penasquito deposit. The complex is extensively

altered and where sampled contains disseminated gold and silver mineralization. The

precious metal grades range from anomalous to what would be ore grade in a bulk

tonnage deposit. The complex is also anomalous in base metals, arsenic, antimony

and locally mercury, the so-called pathfinder elements for many epithermal gold and

silver deposits. Evidence of a mineralizing process on the property is also indicated

by the Santa Rosa Mines, a series of veins, replacement, and breccia deposits on the

eastern part of the property that are reported to have produced about 50,000 tonnes

of high grade gold and silver with associated base metals.

The intriguing part of the exploration model is that as much as three kilometres of the

northern prospective contact between the intrusive and the sedimentary rocks is

covered by alluvium (sands and gravels). It should be noted that many of the recently

discovered deposits in Mexico and the south-western United States have been located

under alluvium. The discoveries have usually involved a similar situation to this, a

known past producing but relatively small mine working or mineralized outcrop in a

mining district with much of the prospective geological terrain obscured by alluvium.

In and of itself, the mineral showing is not economically important but it demonstrates

that the mineralizing process was active. The Penasquito discovery fits this pattern

as it is almost entirely covered by alluvium, yet there is one outcrop in the vicinity that

indicates the possibility of what may be discovered.

Work by Peñoles, MacMillan Gold, and an independent consultant have verified the

presence of strongly anomalous gold and silver values along with a suite of associated

metals (zinc, lead, arsenic, antimony and mercury) along the three exposed contacts

of the caldera complex. These geochemical associations suggest two possible target

types, either a skarn as described above or a breccia pipe. A breccia pipe, in this

context, is a rock composed of rock fragments between which there is space for the

deposition of economic minerals particularly disseminated gold and silver. Penasquito,

In general the Cerro de

Oro target is similar to

Penasquito but seems to

be a larger intrusive

complex with a higher

gold to silver ratio

The intrusive complex

is extensively altered

with anomalous gold,

silver and the

“pathfinder elements”

5. eResearchMacMillan Gold Corp.

5May 6, 2003

30 km to the northwest is an example of this style of deposit. Western Silver (formerly

Western Copper) has recently announced an indicated resource of 118 million tonnes

with grades of 41.8 g/t Ag, 0.36 g/t Au, 0.38% Pb and 0.89% Zn with an additional

inferred resource of 58 million tonnes at slightly lower grades1

.

Drilling at Cerro de Oro is expected to start within the next month or two, now that

permits have been received, when the appropriate geophysical and more detailed

geochemical surveys have been completed.

Tetasiari Gold / Silver Project

Tetasiari is located 15 km south southwest of the Alamo Dorado property that

motivated Pan American Silver to merge with Corner Bay Silver Inc. With a proven

reserve of 35.5 million tonnes of 68 g/t silver and 0.26 g/t gold, the Feasibility Study

for Alamo Dorado indicated an operating cost of $3.25 per ounce of silver and total

costs of $4.13 per ounce silver. The calculated Internal Rate of Return is 17-33%

after tax, depending on the debt - equity mix. Based on 100% equity financing the

project has a Net Present Value of $19.1 million dollars. Another such find would be

an attractive project to the small to mid-tier silver producers and would certainly be

material for a company such as MacMillan Gold.

Tetasiari is a 724-hectare property that MacMillan Gold has optioned by payment of

US$1,000, issuance of 100,000 shares and a Net Smelter Return of 2.5%, 1% of

which may be purchased at MacMillan Gold's discretion for $1,000,000. Geologically

the property was selected for its similarities to the Alamo Dorado project, both with

respect to the overall potassic and silicic alteration, and its position with respect to

the Sinaloa Batholith. Within the core of brecciated and silicificed metasediments are

alluvial gold workings that indicate the potential for a bedrock source that is as yet

undiscovered. Initial rock and soil sampling confirms the presence of anomalous

gold and silver. Geological mapping indicates that the 500 metre thick package of

altered and brecciated rocks can be traced over a three-kilometre strike length.

MacMillan Gold plans a program of geological mapping, soil and rock sampling as

well as trenching in order to define diamond drill targets.

La Violetta Silver Project

La Violetta is a 524-hectare property, approximately 12 km northeast of the Alamo

Dorado, and like Tetasiari was acquired for its geological similarities to Alamo Dorado

and reported high-grade gold silver quartz veins. MacMillan Gold was able to stake

this property for its own account and no underlying agreements apply. A program

similar to that on Tetasiari is planned for the coming year.

1

Investors should note that discovery of this type of deposit can drive share appreciation by almost an

order of magnitude. One year ago prior to the discovery of Penasquito Western Silver shares were priced

at $0.60 compared to today’s price of $3.50, current market capitalization of $116 million, and a 52

week high of $4.74.

Alluvial gold workings

indicate the potential

for a bedrock source, as

yet undiscovered

Drilling at Cerro de Oro

is expected to start

within the next month

or two

6. eResearch MacMillan Gold Corp.

6 May 6, 2003

Figure 3. Tetasiara, Alamo Dorado and La Violetta Geology Map

Source: Company reports

Jalisco State Projects

Fiebre de Oro and El Soccorro

Both of these projects are located in south central Mexico between Mexico City and

the Pacific Coast. Both were acquired by staking, subject to a finder's fee and a Net

Smelter Return which the Company has an option to purchase outright at its election.

Fiebre de Oro is a gold silver prospect that covers an area of high-grade veins and

mineralized breccias within Tertiary rhyolite (silica rich) domes. These domes overlie

older andesitic (less siliceous and more iron rich) sequences that have been intruded

by quartz monzonite intrusives (granite like intrusions). Although this is a new discovery

the setting is similar to other gold and silver showings and mines within the productive

Sierra Madre Occidental that hosts most of Mexico's significant historic and current

silver mines. MacMillan Gold's initial work has confirmed the higher grade nature of

the veins with samples up to 20 g/t gold across a half to two metres. More importantly

its work has also indicated that the much wider breccias (50-125 metres) have gold

values from half a gram to almost five grams along the almost two kilometres of

strike that has been mapped out during their initial evaluation. This exciting target will

be evaluated through a program of detailed prospecting, soil geochemistry, mapping,

trenching and channel sampling. This target is adequately protected by the 1,700-

hectare claim.

El Soccorro is a silver target in a district that dates back to pre-revolutionary times.

MacMillan Gold acquired this property as its initial examination noted silver

mineralization in several different settings, namely as disseminations, veins and breccias

within argillites (very fine grained sedimentary rocks) and sandstones along with

barite (barium sulphate), quartz and carbonate minerals. The exposed occurrences

are up to six metres wide, however the alteration and colour anomalies suggest

widespread mineralization over a 200 metre by one kilometre long area. This area will

be further evaluated through a program similar to that at Fiebre de Oro, namely more

detailed rock and soil sampling prior to trenching with the specific aim of defining

drilling targets for subsequent programs.

Initial work has

indicated the presence

of gold in the breccias

as well as the high-

grade veins

The initial examination

noted silver in several

settings and the

alteration and colour

anomaly suggest the

presence of widespread

mineralization

7. eResearchMacMillan Gold Corp.

7May 6, 2003

Peruvian Properties

Minas Santa Rosa and Aquila Pit

These properties formed an integral part of the Company's ability to get re-listed on

the TSX-Venture Exchange. These properties had previously been optioned to one of

the world largest mining companies, Rio Tinto Mining and Exploration Ltd. Over

several years Rio Tinto spent US$ 1,500,000 on exploration and drilling and a further

US$ 170,000 on option payments to MacMillan Gold. When Rio Tinto withdrew

from the project in 1999 the Company regained 100% interest in these properties. In

March of 2000 MacMillan Gold optioned the adjoining ground (Pasacancha Concession)

from Inca Pacific Resources Inc. as the Company feels that the known mineralization

on the Santa Rosa / Aquila may extend onto the neighbouring ground. With results

from Rio Tinto's work that include 400.5 metres of 0.63% copper and 0.04 %

molybdenum and 270.2 metres of 0.44% copper and 0.02% molybdenum, there is

clearly a mineral deposit of some size here. The Company plans a modest four-to-six

hole drill program on these properties. Drilling within the Aquila pit would be to audit

and confirm historical data in government files. Drill holes on the Pasacancha

Concession would be to investigate the potential for an extension onto Pasacancha that

would increase the size of the mineralized system. As these properties are not central to

MacMillan Gold's strategy, management will joint venture this to another company

with a copper and / or a Peruvian strategy and focus, if there is any success in this

drilling.

DIRECTORS AND MANAGEMENT

Mr. George A. Brown, BBA, President

George has provided financial services to a number of mineral exploration and mining

companies over his 20-year career in the mining sector. Most notable among these

are Campbell Resources Inc., Cullaton Lake Gold Mines and Boulder Mining

Corporation. Most recently he was Treasurer of Corner Bay Silver Inc. during the

time of their Alamo Dorado discovery and of the feasibility study, which led to the

subsequent merger with Pan American Silver Inc. This background provides solid

experience with which to advance MacMillan and its new Mexican gold and silver

focus.

Mr. David Bending, M.Sc. Vice President Exploration

David has worked as an exploration geologist and manger with several large mining

companies. Most recently he was with Homestake, prior to their merger with American

Barrick, as Exploration Manager for Northern Latin America. David is fluent in Spanish

and has extensive experience working in Mexico. He is responsible for managing and

directing all Mexican exploration as well as evaluating future projects and opportunities.

Mr. Pedro Sanchez Majorada, M.I.M., B. Ap.Sc.

Mr. Majorado is a professional mining and metallurgical engineer with extensive

experience in Mexico both with the government and with some of Mexico's largest

mining companies. Most recently, and for the last ten years he was president of

Industrias Peñoles S.A. de C.V. As one of Mexico's most respected senior mining

executives he brings considerable influence and respectability to MacMillan Gold's

efforts in Mexico.

Drilling on the

Pasacancha Concession

will investigate the

possibility of a much

larger mineralized

system than that

currently identified

8. eResearch MacMillan Gold Corp.

8 May 6, 2003

Mr. Ross Lawrence, P. Eng., M. Commerce, Director

Ross has served as Vice Chairman of the well established and respected geological

consulting firm, Watts, Griffis & McOuat. With over 35 years experience in the

mining industry he will provide insight into many aspects of the mining industry.

Mr. Greg Van Staveren, C.A., C.M.A. and C.P.A. Director, CFO

Greg has been a partner with in one Canada's largest accounting firms and has extensive

experience with all aspects of corporate reporting within the mining and junior resource

sectors. As CFO he will be involved in all financial aspects of the company's activity

both in Canada and Mexico.

Mr. Geoffery Burns, B.Sc., M.B.A. Director

Geoff is one of two newly elected directors. He has over twenty years of industry

experience ranging from field geologist to senior vice president and C.F.O. of a major

international primary silver producer.

Mr. David Loder, P.Eng., Director

David has over forty years experience in the mining business from surveyor through

to senior management. Most recently he was vice president and general manager of

the Santa Gertrudis open pit mine in northern Mexico.

FINANCIAL FORECAST AND VALUATION

The company has 25.8 million shares outstanding (28.0 million fully diluted) with

management ownership of 20 %. At recent share prices of $0.25 - $0.27 this is a

market capitalization of $6.5 to $7.0 million. This is within the rather broad range of

its peer group of companies that are in the early stages of exploration and do not have

any indicated or inferred reserves or resources. Working capital has recently increased

to approximately $450,000 with the exercise of 100% of the warrants on March 7,

2003. This is adequate for the proposed program that will be particularly focussed on

the Cerro de Oro project. Management is keenly aware of both the need to minimize

administration expenses and the need to raise additional funding for ongoing work on

all of the properties.

We have valued the Company at C$0.60 within the next twelve months based on the

potential for discovery through drilling at Cerro de Oro, or through prospecting and

trenching, at one of the other four properties.

9. eResearchMacMillan Gold Corp.

9May 6, 2003

CONCLUSIONS

MacMillan Gold has identified and acquired five early stage gold and silver projects

on very reasonable terms or by staking. Its particular emphasis on disseminated gold

and silver, while not unique among exploration companies, places it in a smaller pool

of companies competing for these types of properties. The experience of management

and some of the key shareholders, with past successes such as the Alamo Dorado

deposit will give the Company a competitive advantage in this area. This particular

focus will also attract the segments of the retail market who are particularly interested

in silver plays. Although Cerro de Oro is the current focus of attention and the flagship

property we anticipate some very positive results from at least one of the other four

properties. These factors along with the experience and goal oriented nature of the

management warrants investor attention.

12. For further informations

and subscription contact:

Independent Equity

Research Corp.

130 Adelaide St. W,

Suite 2215, Toronto Ont.,

Canada M5H 3P5

Toll-free: 1-866-854-0765

Our research is accessible on:

www.eresearch.ca

Price

Single Report $29*

Annual Subscription $99*

(full service)

Annual Subscription $50*

(single company)

* plus applicable tax

DisclosureStatement

eResearch accepts fees from the companies it researches (the “covered companies”) and from major financial

institutions. The sole purpose of this policy is to defray the cost of researching small and medium capitalization stocks

which otherwise receive little research coverage. In this manner,eResearch can minimize fees to its subscribers.

To ensure complete independence and editorial control over its research, eResearch followscertainbusinessprac-

tices and compliance procedures. Among other things, fees from covered companies are due and payable prior to the

commencement of research and, as a contractual right, eResearch retainscompleteeditorialcontrolovertheresearch.

eResearch analysts are compensated on a per-company basis and not on the basis of his/her recommendations.

Analysts are not allowed to solicit prospective covered companies for research coverage byeResearch and are not

allowed to accept any fees or other consideration from the companies they cover for eResearch .Analystsarealsonot

allowed to trade in the shares, warrants, convertible securities or options of companies they cover for eResearch .

In addition, eResearch , its officers and directors cannot trade in shares, warrants, convertible securities or options

of any of the covered companies. eResearch accepts payment for research only in cash and will not accept payment

in shares, warrants, convertible securities or options of covered companies. eResearch will not conduct investment

banking or other financial advisory, consulting or merchant banking services for the covered companies. eResearch is

not a brokerage firm and does not trade in securities of any kind.

eResearch’s sole business is in providing independent equity research to its institutional and retail subscribers.

No representations, express or implied are made by eResearch as to the accuracy, completeness or correctness of

its research. Opinions and estimates expressed in its research representeResearch’s judgment as of the date of its

reports and are subject to change without notice and are provided in good faith and without legal responsibility. Its

research is not an offer to sell or a solicitation to buy any securities. The securities discussed may not be eligible for

sale in all jurisdictions. Neither eResearch nor any person accepts any liability whatsoever for any direct or indirect

loss resulting from any use of its research or the information it contains. This report may not be reproduced, distrib-

uted or published without the express permission of eResearch .

eResearch Recommendation System

Buy: Expected total return within the next 12 months is at least 20%

Speculative Buy: Expected total return within the next 12 months is at least 40%. Risk is High (see

below)

Hold: Expected total return within the next 12 months is between 20% and the T-Bill rate

Sell: Expected total return within the next 12 months is less than the T-Bill rate

eResearch Risk Rating System

A company may have some but not necessarily all of the following characteristics of a specific risk

rating to qualify for that rating:

High Risk: Financial - Little or no revenue and earnings, limited financial history, weak bal-

ance sheet, negative free cash flows, poor working capital solvency, no dividends.

Operational - Weak competitive market position, high cost structure, industry con-

solidating, business model/technology unproven or out-of-date.

Medium Risk: Financial - Several years of revenue and positive earnings, balance sheet in line

with industry average, positive free cash flow, adequate working capital solvency,

may or may not pay a dividend.

Operational - Competitive market position and cost structure, industry stable,

business model/technology is well established and consistent with current state

of industry

Low Risk: Financial - Strong revenue growth and earnings over several years, stronger than

average balance sheet, strong positive free cash flows, above average working capi-

tal solvency, company may pay (and stock may yield) substantial dividends or com-

pany may actively buy back stock.

Operational - Dominant player in its market, below average cost structure, com-

pany may be a consolidator, company may have a leading market/technology posi-

tion.