QNBFS Daily Market Report December 07, 2016

•

1 like•49 views

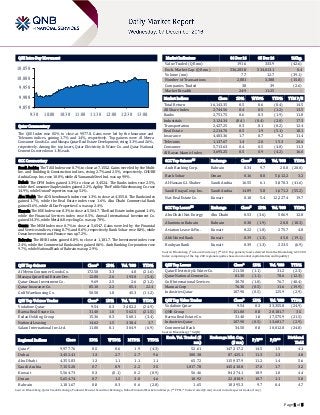

The QSE Index rose 0.5% to close at 9,977.8.

Recommended

More Related Content

Viewers also liked

Viewers also liked (10)

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

QNBFS Daily Market Report December 07, 2016

- 1. Page 1 of 5 QSE Intra-Day Movement Qatar Commentary The QSE Index rose 0.5% to close at 9,977.8. Gains were led by the Insurance and Telecoms indices, gaining 1.7% and 1.4%, respectively. Top gainers were Al Meera Consumer Goods Co. and Mazaya Qatar Real Estate Development, rising 3.3% and 2.6%, respectively. Among the top losers, Qatar Electricity & Water Co. and Qatar National Cement Co. were down 1.1% each. GCC Commentary Saudi Arabia: The TASI Index rose 0.7% to close at 7,155.2. Gains were led by the Multi- Inv. and Building & Construction indices, rising 2.7% and 2.5%, respectively. CHUBB Arabia Coop. Ins. rose 10.0%, while Al Yamamah Steel Ind. was up 9.9%. Dubai: The DFM Index gained 1.3% to close at 3,452.4. The Banks index rose 2.5%, while the Consumer Staples index gained 2.2%. Agility The Public Warehousing Co. rose 14.9%, while Union Properties was up 5.1%. Abu Dhabi: The ADX benchmark index rose 1.3% to close at 4,355.8. The Banks index gained 1.7%, while the Real Estate index rose 1.6%. Abu Dhabi Commercial Bank gained 3.6%, while Al Dar Properties Co. was up 2.4%. Kuwait: The KSE Index rose 0.3% to close at 5,564.7. The Real Estate index gained 1.4%, while the Financial Services index rose 0.5%. Amwal International Investment Co. gained 14.3%, while Metal & Recycling Co. was up 7.9%. Oman: The MSM Index rose 0.7% to close at 5,654.7. Gains were led by the Financial and Services indices, rising 0.7% and 0.6%, respectively. Bank Sohar rose 8.0%, while Oman Investment and Finance was up 7.2%. Bahrain: The BHB Index gained 0.8% to close at 1,181.7. The Investment index rose 2.4%, while the Commercial Banks index gained 0.6%. Arab Banking Corporation rose 9.7%, while National Bank of Bahrain was up 2.9%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Al Meera Consumer Goods Co. 172.50 3.3 4.0 (21.6) Mazaya Qatar Real Estate Dev. 12.80 2.6 193.0 (5.4) Qatar Oman Investment Co. 9.69 2.5 2.6 (21.2) Qatar Insurance Co. 85.10 2.2 85.1 22.4 Gulf Warehousing Co. 50.50 1.8 45.3 (11.2) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 9.54 0.3 3,482.2 (24.9) Barwa Real Estate Co. 31.40 1.0 562.5 (21.5) Ezdan Holding Group 15.36 0.3 560.1 (3.4) National Leasing 14.62 1.5 338.4 3.7 Salam International Inv. Ltd. 11.00 0.1 304.9 (6.9) Market Indicators 06 Dec 16 05 Dec 16 %Chg. Value Traded (QR mn) 191.6 333.9 (42.6) Exch. Market Cap. (QR mn) 536,283.8 534,013.1 0.4 Volume (mn) 7.7 12.7 (39.1) Number of Transactions 2,881 3,388 (15.0) Companies Traded 38 39 (2.6) Market Breadth 24:9 11:25 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 16,143.35 0.5 0.6 (0.4) 14.5 All Share Index 2,744.56 0.4 0.5 (1.2) 13.5 Banks 2,751.75 0.6 0.3 (1.9) 11.8 Industrials 3,124.34 (0.4) (0.4) (2.0) 17.3 Transportation 2,427.25 0.3 0.1 (0.2) 12.4 Real Estate 2,214.70 0.5 1.9 (5.1) 18.1 Insurance 4,403.36 1.7 0.7 9.2 11.4 Telecoms 1,137.67 1.4 2.0 15.3 20.6 Consumer 5,713.63 0.4 0.5 (4.8) 11.3 Al Rayan Islamic Index 3,695.25 0.5 0.9 (4.2) 16.0 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Arab Banking Corp. Bahrain 0.34 9.7 20.0 (20.0) Bank Sohar Oman 0.16 8.0 5,612.2 3.2 Al-Hassan G.I. Shaker Saudi Arabia 16.55 6.1 3,870.3 (41.6) Saudi Enaya Coop. Ins. Saudi Arabia 14.89 5.8 1,671.2 (55.2) Nat. Real Estate Co. Kuwait 0.10 5.4 12,227.4 19.7 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Abu Dhabi Nat. Energy Abu Dhabi 0.53 (3.6) 506.9 12.8 Aluminium Bahrain Bahrain 0.30 (1.9) 28.8 (18.3) Aviation Lease & Fin. Kuwait 0.22 (1.8) 275.7 4.8 Ahli United Bank Kuwait 0.39 (1.3) 45.0 (19.1) Boubyan Bank Kuwait 0.39 (1.3) 223.5 (6.9) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Electricity & Water Co. 211.50 (1.1) 31.2 (2.3) Qatar National Cement Co. 81.30 (1.1) 78.6 (12.3) Gulf International Services 30.70 (1.0) 76.7 (40.4) Mannai Corp 76.30 (0.5) 11.6 (19.9) Industries Qatar 107.90 (0.5) 125.9 (2.9) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Vodafone Qatar 9.54 0.3 33,355.8 (24.9) QNB Group 151.00 0.8 20,181.7 3.5 Barwa Real Estate Co. 31.40 1.0 17,575.9 (21.5) Industries Qatar 107.90 (0.5) 13,601.7 (2.9) Commercial Bank 34.50 0.0 10,012.8 (24.8) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,977.76 0.5 0.6 1.9 (4.3) 52.61 147,317.2 14.5 1.5 4.1 Dubai 3,452.41 1.3 2.7 2.7 9.6 300.38 87,425.1 11.3 1.3 4.0 Abu Dhabi 4,355.83 1.3 1.1 1.1 1.1 65.72 115,937.9 11.2 1.4 5.6 Saudi Arabia 7,155.20 0.7 0.9 2.2 3.5 1,817.78 445,410.8 17.0 1.7 3.2 Kuwait 5,564.73 0.3 (0.1) 0.2 (0.9) 56.46 84,374.1 18.9 1.0 4.4 Oman 5,654.74 0.7 1.2 3.0 4.6 10.92 22,818.9 10.7 1.1 5.0 Bahrain 1,181.67 0.8 0.3 0.6 (2.8) 1.65 18,395.3 9.7 0.4 4.7 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,850 9,900 9,950 10,000 10,050 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 5 Qatar Market Commentary The QSE Index rose 0.5% to close at 9,977.8. The Insurance and Telecoms indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari and GCC shareholders. Al Meera Consumer Goods Co. and Mazaya Qatar Real Estate Development were the top gainers, rising 3.3% and 2.6%, respectively. Among the top losers, Qatar Electricity & Water Co. and Qatar National Cement Co. were down 1.1% each. Volume of shares traded on Tuesday fell by 39.1% to 7.7mn from 12.7mn on Monday. Further, as compared to the 30-day moving average of 8.7mn, volume for the day was 11.7% lower. Vodafone Qatar and Barwa Real Estate Co. were the most active stocks, contributing 45.1% and 7.3% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 12/06 Germany Markit Markit Germany Construction PMI November 53.9 – 52.9 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar Qatar to spend QR46bn on major projects in 2017 – Qatar expects its economy to grow 3.4% in 2017 and plans investment up to QR46bn in major infrastructure projects as part of strategy to achieve sustainable development and economic diversification. Several measures, including efficiency enhancement in public spending, the financial sector growth and higher contribution of the private sector, would make Qatar achieve such a high growth. The Finance Minister stressed that the 2016 budget reinforces Qatar’s confidence for the future, with dedicated investment in healthcare, education and transportation – along with investment in infrastructure for the 2022 FIFA World Cup – all likely to have a positive effect on the national economy. The total budget committed for the development of key strategic megaprojects stands at QR374bn, with further QR46bn set to be invested in 2017. (Gulf-Times.com) ABank may become wholly-owned subsidiary of CBQK – Commercial Bank of Qatar (CBQK) which holds 75% shares in mid-sized Alternatifbank (ABank), said it has received approval from Qatari regulatory authorities enabling Anadolu Endüstri Holding (AEH) to exercise the put option, following which the Turkish lender will become its wholly-owned subsidiary. This approval completes all of the necessary authorizations for the exercise of put option. It is expected that the subsequent share transfer will be made in the second half of December 2016. In July this year, the Qatari lender had informed the Qatar Stock Exchange that it received a notice from AEH to exercise the put option with respect to 192.5mn or 25% of registered shares held by AEH in ABank under the shareholders’ agreement signed with Commercial Bank on July 18, 2013. Share sale value has been calculated at $222.5mn as of July 18, 2016 based on the base price method specified in the shareholders’ agreement. (Gulf- Times.com) QIIK EGM approves its agenda items – Qatar International Islamic Bank (QIIK) announced the results of its extraordinary general assembly meeting (EGM) dated December 5, 2016 where it approved the Amendment of Article 7 regarding the ownership ceiling limit signifying that shares shall be nominal and each share is indivisible in the face of the company, if a share is held by multiple persons, these persons have to choose someone to represent them in the use of the rights related to the share and these persons shall be jointly responsible for the liabilities arising from the ownership of the share. The EGM authorize QIIK Chairman/MD to sign the new Articles of Association after the new amendments and to complete all the procedures to publicize the new amendments. (QSE) QISI EGM approves its agenda items – Qatar Islamic Insurance Company (QISI) announced the results of the Extraordinary General Assembly Meetings held on December 5, where the resolutions passed were as follows: approved the amendment of Article (6) of Chapter II, approved the amendment of Article 13 of Chapter III, approved to add the following text to Article No. (13) of Chapter III where one - third of the members of the Board of Directors of the independent members experienced non- shareholders, and exempted them from owning equity requirement which mentioned in item (3) of this article and approved the amendment of Article 50 of Chapter VI. (QSE) Al Rayan Bank opens its first office in Scotland – Al Rayan Bank (UK), the UK subsidiary of Masraf Al Rayan (MARK), has opened an office in Scotland. The office was officially opened by Al Rayan Bank Chief Executive Officer Sultan Choudhury and Chief Commercial Officer Keith Leach, together with key members of the bank’s executive team. (Gulf-Times.com) Qatar well on track for its PPP legislative framework – Qatar Financial Centre (QFC) Authority CEO Yousuf Mohamed al-Jaida said that various stakeholders in the state are currently finalizing a legislative framework for public-private partnership (PPP) models in Qatar, a move that would further develop the country’s economy. Al-Jaida said Qatar’s entire LNG industry was built on a PPP model, adding that many GCC countries are looking into PPPs to diversify their economies. He said, “The country has built a successful model of partnership between the public and private sectors. The local industries have greatly developed throughout the past year and have benefited from partnerships with Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 29.39% 43.49% (27,013,097.83) Qatari Institutions 22.66% 17.82% 9,269,597.82 Qatari 52.05% 61.31% (17,743,500.01) GCC Individuals 0.35% 0.50% (297,323.70) GCC Institutions 7.68% 9.05% (2,629,453.23) GCC 8.03% 9.55% (2,926,776.93) Non-Qatari Individuals 8.66% 8.93% (515,272.42) Non-Qatari Institutions 31.26% 20.20% 21,185,549.36 Non-Qatari 39.92% 29.13% 20,670,276.94

- 3. Page 3 of 5 international companies. Whether it’s infrastructure or stadiums, a PPP structure is probably going to be the most successful model. A lot of economies regionally and globally have built their infrastructure based on a PPP model.” (Gulf-Times.com) Malaysia is eyeing Qatar investment for Langkawi Island tourism growth – Malaysia wants to infuse Qatari investments in various tourism-related projects in Langkawi Island, a vacation destination in the country’s State of Kedah, which has become popular among American and European tourists. Managing Director of Invest Kedah, Dato’ Ahmad Shukri Tajuddin, a ‘government-linked company’ formed to attract and support business in Kedah, was in Qatar to invite major players in Qatar’s public and private sector to explore investment opportunities in Langkawi. Tajuddin said Malaysia had recorded growth in tourist arrival from 16.4mn visitors in 2005 to 25.7mn in 2015. In 2015, Langkawi Island received 3.62mn tourists. (Gulf-Times.com) International US trade gap widens as exports of soybeans, other products drop – US trade deficit recorded its biggest increase in more than 1-1/2 years in October as exports of soybeans and other products fell, suggesting trade would be a drag on growth in 4Q2016. The Commerce Department said the trade gap rose 17.8%, the largest increase since March 2015, to $42.6bn. Higher imports due to rising domestic demand also contributed to the widening of the deficit. When adjusted for inflation, the deficit rose to $60.3bn from $54.2bn in September. Exports contributed 0.87 percentage point to the third quarter's 3.2% annualized rate of increase in gross domestic product. The jump in exports in 3Q2016 largely reflected a surge in soybean shipments to China after a poor harvest in Argentina and Brazil. (Reuters) US productivity in 3Q2016 fastest in two years – US worker productivity rebounded sharply in 3Q2016 as initially estimated, marking its quickest rate of growth in two years, but the trend remained weak. The Labor Department said that nonfarm productivity, which measures hourly output per worker, rose at an unrevised 3.1% annual rate. The increase ended three straight quarters of decline. Productivity fell at a 0.2% rate in 2Q2016 and was unchanged compared to 3Q2015. The government revised GDP data to show the economy growing at a 3.2% pace in 3Q2016 instead of the 2.9% rate it had previously reported. Output per worker in 3Q2016 jumped at a 3.6% rate, also the fastest pace since 3Q2014. (Reuters) UK narrows current account deficit after major data error – Britain appears to have relied slightly less on the kindness of strangers before the Brexit vote, after its statistics agency uncovered major errors in trade data that meant the current account deficit was narrower than first calculated. Bank of England Governor Mark Carney used the phrase in the run-up to June's referendum on EU membership, highlighting how Britain, to balance its books, needs tens of billions of pounds of foreign finance a year that could be placed in jeopardy. After the Office for National Statistics revised down the gap to 6.0% of gross domestic product from 7.0%, it turns out Britain no longer chalked up a record deficit in 4Q2015. The downward revision continued into 2016. The current account deficit for 2015, while cut from an earlier 5.4% of GDP, was still the largest on record at 5.0%. The gap for 2Q2016 was revised down to 5.4% from 5.9%. (Reuters) Household, government spending support Eurozone in 3Q2016 – Household and public sector spending supported Eurozone growth in 3Q2016 as the impact of foreign trade turned negative. Eurostat confirmed gross domestic product growth in the 19 countries sharing the Euro rose 0.3% QoQ. However, it revised up its figure for YoY growth to 1.7% from 1.6% it previously reported. The biggest contribution to growth came from household spending, which added 0.2 percentage points to the final result, with changes of inventories and public sector spending also each adding another 0.1 points. (Reuters) German industry orders post biggest rise for more than two years – German industrial orders rose in October at their fastest pace for more than two years, suggesting that the industrial sector will prop up growth in Europe's largest economy in the coming months. Factories saw demand climb 4.9% on the month despite bulk orders being lower than usual. That was the biggest increase since July 2014 and far above the Reuters consensus forecast for a 0.6% rise. (Reuters) Japan business mood brightens as yen weakens – Japanese manufacturers' confidence rose for a fourth straight month to a 16-month high in December and the service sector's mood also rose, a Reuters poll showed, with a weaker yen brightening prospects for exporters. The monthly Reuters Tankan - which tracks the Bank of Japan's key quarterly tankan - found sentiment at manufacturers and service-sector firms both up from three months ago, pointing to improvement in the central bank's survey out next week. In the poll of 531 large- and mid-sized firms, carried out between November 22 and December 2 and in which 268 responded, the sentiment index for manufacturers rose to 16 from 14 in November, driven by steel and transport equipment makers. It was the highest reading since August 2015, but it is expected to fall to 10 over the next three months. (Reuters) Regional Low wage growth expected for Gulf countries – Households in the Arabian Gulf are facing their weakest earnings growth prospects in a decade as low oil prices force employers to keep pay rises to a minimum. Real wages in the region will increase by just over 1% in 2017 a lower rise than most other regions except Latin America and Africa. Although headline pay increases in Arabian Gulf countries would average 4.2%, inflation will mean that real disposable incomes will rise by just 1.3%. UAE is expected to have the lowest real wage increases in the region, with average salaries rising by just 0.5% as slowing growth forces companies to tighten budgets. Employees in Saudi Arabia are expected to fare only slightly better, with real wages expected to increase by 0.8%. (GulfBase.com) KSA non-oil business activity buoyed by bond issue – According to a survey, growth in Saudi Arabia’s non-oil private sector picked up in November from a record low in October after a mammoth $17.5bn bond issue by the government improved sentiment in the business community. The seasonally adjusted Emirates NBD Saudi Arabia Purchasing Managers’ Index rose to 55.0 in November from 53.2 in October, which was the lowest level since the survey was launched in August 2009. A level above 50 means business is expanding. The bond sale in late October, Riyadh’s first overseas sovereign bond issue, eased fears about Saudi Arabia’s ability to finance itself in an era of low oil prices. It gave the government room to suspend domestic bond issues, causing money market rates to begin pulling back from multi-year highs. (GulfBase.com) Saudi Aramco cuts January oil price to Asia to four-month low – Saudi Aramco has cut the January price for its Arab Light crude for Asian customers to the lowest in four months as it holds to a strategy of preserving market share in the world's fastest-growing demand center. The price cuts are meant to ensure that Saudi Aramco can still sell more oil into Asia even after going along with the OPEC-Russia deal to cut output. Saudi Arabia has been struggling over the last two years to fight off increased competition from other producers in the Middle East, Russia and the Atlantic Basin. (Reuters) KSA’s Almarai recommends lower cash dividend for 2016 – Saudi Arabia's Almarai said that its board had recommended a cash

- 4. Page 4 of 5 dividend of SR0.9 per share for 2016. Almarai, the Gulf's largest dairy firm, paid a cash dividend of SR1.15 for 2015. (Reuters) Saudi Arabia ready for Saudi Aramco’s share sale in domestic market – According to the Vice Chairman of the Kingdom’s market regulator, Saudi Arabia is ready for the initial public offering of Saudi Arabian Oil Co. in the domestic market, with additional work needed if there is a decision to sell shares in more than one country. Saudi Aramco’s Chief Executive Officer, Amin Nasser said that Saudi Aramco plans to sell shares on the Saudi stock market and is also considering foreign bourses in London, Hong Kong and New York. Saudi Aramco’s plan to sell a stake of about 5% could value the company in trillions of dollars. (Bloomberg) Joint Kuwait-Saudi Arabia oil fields to stick to OPEC caps if restarted – Kuwait and Saudi Arabia agreed that any resumption of crude production from shared oil fields along their border won’t raise their output beyond limits set at the OPEC meeting last week. Saudi Arabia and Kuwait will cut output from their producing oil fields to allow for any increase from the Wafra and Khafji fields between the two countries, who asked not to be identified because the information isn’t public. The countries have yet to agree on a specific time to restart the shared fields. (Bloomberg) Saudi Investment Bank’s BOD recommends capital hike, cash dividends – Saudi Investment Bank board of directors recommended in the extraordinary general meeting (EGM) increasing the bank’s capital by 7.1% from SR7bn to SR7.5bn. The SR500mn capital hike will be financed from the retained earnings representing a distribution of 1 bonus share for every 14 shares, increasing the total outstanding shares from 700mn to 750mn. Saudi Investment Bank also announced, in a separate statement to the Saudi Stock Exchange (Tadawul), that the board of directors has recommended the distribution of cash dividends for the year 2016 at SR0.5 per share or 5% of capital. (Tadawul) Emirates Islamic Bank launches AED1.5bn dirham rights issue – Emirates Islamic Bank, the Shariah-compliant arm of Dubai’s largest lender, launched its AED1.5bn rights issue. Shareholders, who hold shares in the bank at the close of business, will be eligible to the subscription which begins on December 14, 2016 and ends on December 28, 2016. Allocation of the new shares will be made on December 29, 2016. (Gulf-Times.com) GFH Financial Group to inject cash in stalled Bahrain development – GFH Financial Group (GFH) has completed a debt-restructuring agreement with the developer of a long-delayed $700mn project in Bahrain. GFH said that under the new agreement it would fund the completion of the 35,900 square meters up market housing and hotel project by injecting cash up to $50mn. (GulfBase.com) GFH Financial Group close to completing Al Khair Bank acquisition, eyes another merger – GFH Financial Group hopes to largely complete the acquisition of Bahrain's Bank Al Khair in 1Q2017 and is at an advanced stage of exploring a merger with another Bahraini bank. (Reuters) CEO: Islamic bank Al Baraka eyes $300mn Tier 1 Sukuk issue in 1Q2017 – Chief Executive of the Bahrain-based Islamic lender, Al Baraka Banking Group is targeting the sale of capital-boosting Sukuk worth $300mn in 1Q2017, with operations in over a dozen countries. Al Baraka had a total capital adequacy ratio - a key indicator of a bank's financial health, which combines both Tier 1 and supplementary Tier 2 capital of 15.15% as of June 30, 2016. (Reuters)

- 5. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. WLL One Person Company Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. WLL One Person Company (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 5 of 5 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 80.0 100.0 120.0 140.0 160.0 180.0 Nov-12 Nov-13 Nov-14 Nov-15 Nov-16 QSEI ndex S& PPanA r ab S& PGCC 0.7% 0.5% 0.3% 0.8% 0.7% 1.3% 1.3% 0.0% 0.5% 1.0% 1.5% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,169.75 (0.1) (0.6) 10.2 MSCI World Index 1,727.82 0.6 1.1 3.9 Silver/Ounce 16.72 (0.2) (0.1) 20.7 DJ Industrial 19,251.78 0.2 0.4 10.5 Crude Oil (Brent)/Barrel (FM Future) 53.93 (1.8) (1.0) 44.7 S&P 500 2,212.23 0.3 0.9 8.2 Crude Oil (WTI)/Barrel (FM Future) 50.93 (1.7) (1.5) 37.5 NASDAQ 100 5,333.00 0.5 1.5 6.5 Natural Gas (Henry Hub)/MMBtu 3.71 3.0 8.9 60.4 STOXX 600 344.57 0.5 1.9 (7.1) LPG Propane (Arab Gulf)/Ton 62.00 (0.4) 1.6 58.5 DAX 10,775.32 0.3 2.8 (1.5) LPG Butane (Arab Gulf)/Ton 90.00 (1.1) 7.1 56.5 FTSE 100 6,779.84 0.1 0.6 (6.6) Euro 1.07 (0.4) 0.5 (1.3) CAC 40 4,631.94 0.7 2.6 (1.5) Yen 114.02 0.1 0.4 (5.2) Nikkei 18,360.54 0.0 (0.6) 2.1 GBP 1.27 (0.4) (0.4) (14.0) MSCI EM 861.49 0.9 1.0 8.5 CHF 0.99 (0.4) 0.0 (0.8) SHANGHAI SE Composite 3,199.65 (0.4) (1.3) (14.7) AUD 0.75 (0.1) 0.1 2.4 HANG SENG 22,675.15 0.7 0.5 3.4 USD Index 100.49 0.4 (0.3) 1.9 BSE SENSEX 26,392.76 0.6 1.1 (1.2) RUB 63.86 0.1 0.1 (11.9) Bovespa 61,088.25 2.6 3.0 63.5 BRL 0.29 0.4 2.1 16.2 RTS 1,059.97 (0.9) 0.9 40.0 116.0 105.1 101.1