QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

20121126 efar eurozone update_vs05

1. QNB Economics

economics@qnb.com.qa

30 November 2012

Eurozone sovereign debt crisis to last a number of years

Despite a recent agreement by the Eurogroup and the The buyback programme accounts for a large

IMF on releasing further assistance for Greece under proportion of Greece’s planned debt reduction and is

its bailout programme, the outlook for Eurozone therefore central to its success. If the buyback fails to

economies remains weak and the region’s sovereign meet expectations, another round of bailout

debt crisis is likely to stay with us for a number of negotiations and adjustments would probably need to

years, according to QNB Group. be made to the bailout package, according to QNB

Group. The persistent failure of bailout packages could

On November 27th, after a number of attempts, eventually lead to official creditors (the European

Eurozone finance ministers along with the IMF finally Commission (EC), the ECB and even the IMF) being

agreed to a series of measures that aim to reduce forced to take a haircut on Greek debt some time in

Greek debt from current levels of close to 200% of 2014-15 to make Greek debt sustainable.

GDP to 124% by 2020, and lower than 110% by 2022.

The measures involved: cutting interest rates on In any case, alongside debt forgiveness and favourable

bailout loans; extending maturities of loans; returning bailout loan terms, Greece still needs to boost

profits made by the European Central Bank (ECB) on economic growth to ensure it can manage its debt.

the purchase of Greek bonds to Greece; and buybacks Real GDP is expected to contract by 6.0% in 2012 and

of Greek debt by the Eurozone from the private sector. by 4.2% in 2013, held back by spending cuts and tax

increases. As long as Greece remains in recession,

The agreement cleared the way for the release of which is likely in the short to medium term, it will

€34.4bn in bailout funds in mid December, €23.8bn of continue to need further external support. Included in

this is for bank recapitalisation and €10.6bn for the bailout package is a tough programme of economic

financing the Greek budget. The funds were originally reforms aimed at making the economy more

scheduled to be released in May and Greece has been competitive and boosting growth.

kept afloat by emergency loans since then. However,

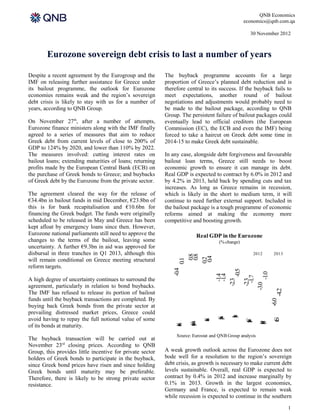

Eurozone national parliaments still need to approve the Real GDP in the Eurozone

changes to the terms of the bailout, leaving some (% change)

uncertainty. A further €9.3bn in aid was approved for

disbursal in three tranches in Q1 2013, although this 2012 2013

0.8

0.8

0.4

will remain conditional on Greece meeting structural

0.2

0.1

reform targets.

-0.4

-0.5

-1.0

-1.4

-1.4

-1.7

A high degree of uncertainty continues to surround the

-2.3

-2.3

-3.0

agreement, particularly in relation to bond buybacks.

-4.2

The IMF has refused to release its portion of bailout

funds until the buyback transactions are completed. By

-6.0

buying back Greek bonds from the private sector at

prevailing distressed market prices, Greece could

y

a

I

avoid having to repay the full notional value of some

l

t

S

n

p

a

G

i

F

n

C

e

c

a

c

e

r

u

p

y

r

s

r

P

m

g

u

o

G

a

r

of its bonds at maturity.

l

t

E

y

n

a

e

n

o

u

e

z

r

r

Source: Eurostat and QNB Group analysis

The buyback transaction will be carried out at

November 23rd closing prices. According to QNB

Group, this provides little incentive for private sector A weak growth outlook across the Eurozone does not

holders of Greek bonds to participate in the buyback, bode well for a resolution to the region’s sovereign

since Greek bond prices have risen and since holding debt crisis, as growth is necessary to make current debt

Greek bonds until maturity may be preferable. levels sustainable. Overall, real GDP is expected to

Therefore, there is likely to be strong private sector contract by 0.4% in 2012 and increase marginally by

resistance. 0.1% in 2013. Growth in the largest economies,

Germany and France, is expected to remain weak

while recession is expected to continue in the southern

1

2. QNB Economics

economics@qnb.com.qa

30 November 2012

economies with the most severe sovereign debt issues outlook for the economy and an expected increase in

(Spain, Italy, Cyprus, Portugal and Greece). debt to GDP levels.

There have been recent indications of a weakening in Furthermore, Spain’s financing needs are likely to

the largest Eurozone economy, Germany, where: GDP force it to ask for international aid in early 2013.

slowed to 0.4% year-on-year in Q3 2012, down from Additionally, Cyprus requested a bailout in November,

1.7% in Q1; the German Ifo Business Climate Index, which is expected to total up to €17.5bn, but the exact

which measures expectations for the next six months, package is still being finalised.

was 101.4 on November 24 th, down from 108.3 in

January; and the German Manufacturing Purchasing In summary, the outlook for the Eurozone is poor with

Manager’s Index was 46.8 in November, a level that downside risks. New countries are likely to ask for

indicates contraction. bailouts and existing bailout programmes are on shaky

ground. The bailout programmes and pressures from

France has also faced a deteriorating outlook. It was investors or rating agencies are likely to lead to greater

downgraded by one notch from AAA by Moody’s fiscal austerity, dampening economic growth, which is

rating agency in November, having been downgraded already feeble. Without growth, sovereign debt is only

by Standard and Poor’s in January. Public debt has likely to become less sustainable. Therefore, according

reached 90% of GDP while rising labour costs (owing to QNB Group, it is going to take several years before

to high employment taxes and an inflexible labour the Eurozone will be truly rid of its sovereign debt

market) are leading to declining competitiveness and issues and growth returns to full potential.

economic growth remains slow. Reforms have been

perceived as insufficient, leading to a worsening

2