1. Para

No.

Commissio

nerate

Name of the

Unit M/s

Ministry's Further comments Vetting comments of O/o PDA (C),

Bangalore

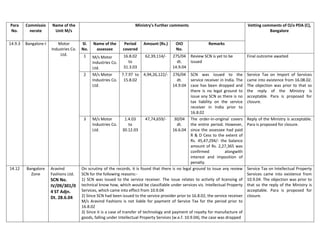

14.9.3 Bangalore-I Motor

Industries Co.

Ltd.

Sl.

No.

Name of the

assessee

Period

covered

Amount (Rs.) OIO

No.

Remarks

1 M/s Motor

Industries Co.

Ltd.

16.8.02

to

31.3.03

62,39,114/- 275/04

dt.

14.9.04

Review SCN is yet to be

issued

Final outcome awaited

2 M/s Motor

Industries Co.

Ltd.

7.7.97 to

15.8.02

4,94,26,122/- 276/04

dt.

14.9.04

SCN was issued to the

service receiver in India. The

case has been dropped and

there is no legal ground to

issue any SCN as there is no

tax liability on the service

receiver in India prior to

16.8.02

Service Tax on Import of Services

came into existence from 16.08.02.

The objection was prior to that so

the reply of the Ministry is

acceptable. Para is proposed for

closure.

3 M/s Motor

Industries Co.

Ltd.

1.4.03

to

30.12.03

47,74,659/- 30/04

dt.

16.6.04

The order-in-original covers

the entire period. However,

since the assessee had paid

R & D Cess to the extent of

Rs. 45,47,294/- the balance

amount of Rs. 2,27,365 was

confirmed alongwith

interest and imposition of

penalty.

Reply of the Ministry is acceptable.

Para is proposed for closure.

14.12 Bangalore

Zone

Aravind

Fashions Ltd.

SCN No.

IV/09/301/0

4 ST Adjn.

Dt. 28.6.04

On scrutiny of the records, it is found that there is no legal ground to issue any review

SCN for the following reasons:-

1) SCN was issued to the service receiver. The issue relates to activity of licensing of

technical know how, which would be classifiable under services viz. Intellectual Property

Services, which came into effect from 10.9.04

2) Since SCN had been issued to the service provider prior to 16.8.02, the service receiver

M/s Aravind Fashions is not liable for payment of Service Tax for the period prior to

16.8.02

3) Since it is a case of transfer of technology and payment of royalty for manufacture of

goods, falling under Intellectual Property Services (w.e.f. 10.9.04), the case was dropped

Service Tax on Intellectual Property

Services came into existence from

10.9.04. The objection was prior to

that so the reply of the Ministry is

acceptable. Para is proposed for

closure.

2. Dy. Director/RA-Central

Aravind

Fashions Ltd.

OIO No.

299/04 dt.

24.9.04

Though it was reported earlier that the review SCN is under process, on scrutiny of

records, it is reported that there is no legal ground to issue any review SCN for the

reason that it is a case of transfer of technology and payment of royalty for manufacture

of goods. Such activity would not come within the purview of Consulting Engineer

Services, but Intellectual Property Services (w.e.f. 10.9.04)

Service Tax on Intellectual Property

Services came into existence from

10.9.04. The objection was prior to

that so the reply of the Ministry is

acceptable. Para is proposed for

closure.

Banner

Pharma Caps

India Ltd.

On scrutiny of records, it is found that there is no legal ground to issue any review SCN

for the following reasons:-

i) SCN was issued to the service receiver. The case is not a sale of technical knowhow,

but only licencing thereof and the amount paid was the royalty of the manufacture of

goods. Such activity would not come under the perview of Consulting Engineer Services

ii) Prior to 16.8.02, foreign service provider was liable for payment of service tax.

Service Tax on Import of Services

came into existence from 16.08.02.

The objection was prior to that so

the reply of the Ministry is

acceptable. Para is proposed for

closure.

Bio-Con India

Ltd.

Review SCN is being issued Finality of Adjudication of SCN is

awaited.

L & T,

Komatsu

SCN was issued to M/s Komatsu, Japan and not to M/s L & T Komatsu (Indian Co.). On

scrutiny of records, it is reported that there is no legal ground to issue any review SCN

for the following reasons:-

i) Service rendered outside India will not be liable to Service Tax, which has been clarified

by circular 36/04/2001 dt. 8.10.01. Further, the notice being a foreign service provider,

the Board is examining the issue of notification under Sec. 11C for waiver of tax liability.

Decision of the Board to issue

notification for waiver of tax

liability u/s 11C is awaited

Goetze India

Ltd.

Appeal against OIA 193/04 dated 15.12.04 pending in CESTAT Final outcome of the appeal

pending at CESTAT is awaited

Kirloskar

Electric Co.

It has been reported that the said Service charges, were in the nature of reimbursement

of travel expenses towards deputation of assessee's personnel to site and hence do not

fall under the category of Consulting Engineer and therefore does not attract Service Tax

Reply of the Ministry is acceptable.

Para is proposed for closure.

Kirlosker

Batteries

No further comments desired ------