1. MauriceB@bacs.co.il

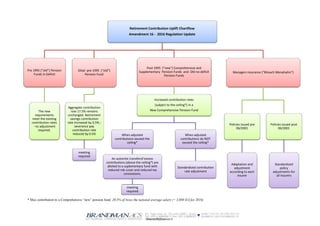

* Max contribution to a Comprehensive “new” pension fund: 20.5% of twice the national average salary (= 3,880 ILS for 2016)

Retirement Contribution Uplift Chartflow

Amendment 16 - 2016 Regulation Update

Pre 1995 ("old") Pension

Funds In Deficit

The new

requirements

meet the existing

contribution rates

- no adjustment

required.

Gilad pre-1995 ("old")

Pension Fund

Aggregate contribution

rate 17.5% remains

unchanged. Retirement

savings contribution

rate increased by 0.5% ;

severance pay

contribution rate

reduced by 0.5%

meeting

required

Post 1995 ("new") Comprehensive and

Supplementary Pension Funds and Old no-deficit

Pension Funds

Increased contribution rates

(subject to the ceiling*) in a

New Comprehensive Pension Fund

When adjusted

contributions exceed the

ceiling*

An automtic transferof excess

contributions (above the ceiling*) are

alloted to a suplementary fund with

reduced risk cover and reduced tax

concessions.

meeting

required

When adjusted

contributions do NOT

exceed the ceiling*

Standardized contribution

rate adjustment

Managers insurance ("Bituach Menahalim")

Policies issued pre

06/2001

Adaptation and

adjustment

according to each

insurer

Policies issued post

06/2001

Standardized

policy

adjustments for

all insurers