How to Get Started in Social Media for Art League City

Myths and Facts.pdf

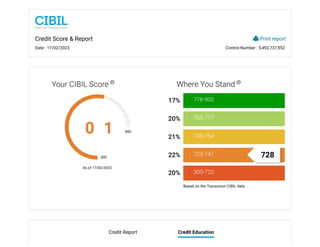

1. Credit Score & Report

Date : 17/02/2023 Control Number : 5,492,737,952

Print report

As of 17/02/2023.

Your CIBIL Score

300

900

0 1

Based on the Transunion CIBIL data

Where You Stand

778-900

17%

765-777

20%

748-764

21%

723-747

22%

300-722

20%

728

Credit Report Credit Education

2. 1. MYTH- CIBIL maintains list of defaulters only and having your name in CIBIL is bad.

FACT- If you have ever taken a loan or credit card from any bank or financial institution then your information is most likely

with CIBIL. So your name will be with CIBIL even if you are paying all your obligations on time. RBI has mandated banks

and financial institutions to submit monthly repayment data pertaining to those customers who have taken a loan or

credit card with them to a Credit Bureau. CIBIL collects and maintains these records of such individual's payment across

institutions. This data is then used by financial institutions to sanction loans and credit cards. How your CIBIL Score and

Report is interpreted by respective bank or financial institution depends on their credit policy. CIBIL does not classify an

individual as a defaulter.

2. MYTH- If you check your CIBIL Score and Report, your credit score will go down.

FACT- Whenever your CIBIL Report is accessed by banks, it reflects as an "enquiry" on your credit report. An enquiry

indicates that you are seeking new credit. However, when you check your own credit score and report directly for CIBIL

this "enquiry" will not reflect in the CIBIL Report and has absolutely no impact on your credit score. It is a good practice to

review your credit report periodically. Click here to get started.

3. MYTH- It is better to use cash than credit cards or loans.

FACT- It is always better to use credit (loan or a credit card) than cash when you have never availed any credit till date and

want to build a credit history. Having a credit history enables a lender to assess your credit-repayment capabilities by

Myths and Facts

What is CIBIL Score and how to improve it?

How to read and interpret your Credit Information Report?

Things to do while preparing for a Loan Application

Myths and Facts

3. determining whether you have managed your credit responsibly. Your credit history helps the bank to assess your ability

to service any additional debt that you may require. If you don't have any loan or credit card and solely rely on cash or a

debit card then the bank does not have any reference to check your payment track record and will solely rely on other

factors such as income and demographics to evaluate your loan application. Having a good credit history will ensure

faster loan approval and disbursals, maybe even better terms.

However, it is advisable to use cash if you have a tendency to overspend on your credit card. Credit Cards charge very high

interest rates. If you don't pay your entire credit card spend each month you will be charged 24% to 36% p.a. on the unpaid

balance. This causes the amount due to grow in to a large amount very quickly and any default on repayments may lead

to an inability to secure loans for other purposes (car and home purchases) in the future. Alternatively, if you have good

financial discipline, credit cards help you build credit history and allow you to take advantage of reward programs such as

fuel cash back, air miles and a host of other giveaways.

4. MYTH- CIBIL is an organization meant ONLY to help banks and financial institutions.

FACT- The objective of CIBIL is to not only help banks and financial institutions make financially sound lending decision

but also empower consumers by enabling them to become more credit disciplined which can help them with faster loan

approvals and sometimes better terms on their loans. In a nutshell, we help you understand how a lender evaluates your

loan application so that you can apply only when your chances of an approval are high and hence, avoid the unnecessary

embarrassment of a loan rejection.

5. MYTH- CIBIL has the authority to make corrections in my credit report directly.

FACT- CIBIL is not authorized to make any changes in your report directly. Any change that needs to be carried out has to

be initiated/approved by the respective bank or financial institution. Only then CIBIL can make any changes to your CIBIL

Report. However, CIBIL can help facilitate this process.

6. MYTH- A low CIBIL Score means I will never get a loan or credit card.

FACT- There is a lender for every borrower. Having a low credit score may close doors to some banks but there are lenders

who are willing to extend credit to such individuals. However, the interest rates and charges may be higher as the

perceived risk associated with a low credit score is higher.

7. MYTH- My assets, income, investments; all have an impact on my CIBIL Score.

FACT- Your CIBIL Report contains details pertaining only to loans and credit cards. It does not take in to account the

balance in your savings or current account, investments or assets such as mutual funds, shares etc. Hence, these

numbers don't impact your CIBIL Score.

8. MYTH- A bounced cheque will lead to a lower credit score of the cheque issuer.

FACT- Since your savings or current account details are not a part of the CIBIL Report, a bounced cheque does not impact

your credit score. However, if you have missed an EMI or credit card payment it will have an impact on your CIBIL Score.

Disclaimer : All information contained in this credit report has been collated by TransUnion CIBIL Limited (TU CIBIL) based on information

provided/ submitted by its various members("Members"), as part of periodic data submission and Members are required to ensure accuracy,

completeness and veracity of the information submitted. The credit report is generated using the proprietary search and match logic of TU

4. CIBIL. TU CIBIL uses its best efforts to ensure accuracy, completeness and veracity of the information contained in the Report, and shall only be

liable and / or responsible if any discrepancies are directly attributable to TU CIBIL. The use of this report is governed by the terms and

conditions of the Operating Rules for TU CIBIL and its Members

How to correct mistakes on your Credit Information Report

Debt Trap: What to look out for if you have a Credit Card

How CIBIL makes your loan search easier

COPYRIGHT 2023 TRANSUNION CIBIL. ALL RIGHTS RESERVED.