Place of Supply Rules for IGST, CGST & SGST

•

2 likes•198 views

Place of Supply analyzed by CA. Jeevan Chandra

Recommended

Recommended

More Related Content

What's hot

What's hot (20)

Similar to Place of Supply Rules for IGST, CGST & SGST

Similar to Place of Supply Rules for IGST, CGST & SGST (20)

Recently uploaded

Recently uploaded (20)

Place of Supply Rules for IGST, CGST & SGST

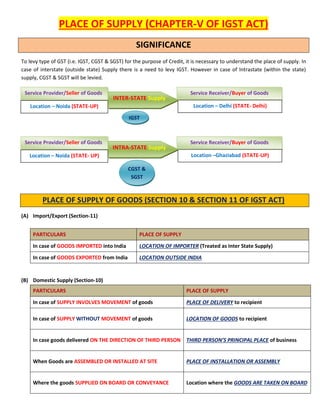

- 1. PLACE OF SUPPLY (CHAPTER-V OF IGST ACT) SIGNIFICANCE To levy type of GST (i.e. IGST, CGST & SGST) for the purpose of Credit, it is necessary to understand the place of supply. In case of interstate (outside state) Supply there is a need to levy IGST. However in case of Intrastate (within the state) supply, CGST & SGST will be levied. PLACE OF SUPPLY OF GOODS (SECTION 10 & SECTION 11 OF IGST ACT) (A) Import/Export (Section-11) PARTICULARS PLACE OF SUPPLY In case of GOODS IMPORTED into India LOCATION OF IMPORTER (Treated as Inter State Supply) In case of GOODS EXPORTED from India LOCATION OUTSIDE INDIA (B) Domestic Supply (Section-10) PARTICULARS PLACE OF SUPPLY In case of SUPPLY INVOLVES MOVEMENT of goods PLACE OF DELIVERY to recipient In case of SUPPLY WITHOUT MOVEMENT of goods LOCATION OF GOODS to recipient In case goods delivered ON THE DIRECTION OF THIRD PERSON THIRD PERSON’S PRINCIPAL PLACE of business When Goods are ASSEMBLED OR INSTALLED AT SITE PLACE OF INSTALLATION OR ASSEMBLY Where the goods SUPPLIED ON BOARD OR CONVEYANCE Location where the GOODS ARE TAKEN ON BOARD Service Provider/Seller of Goods Location – Noida (STATE-UP) Service Receiver/Buyer of Goods Location – Delhi (STATE- Delhi) INTER-STATE Supply IGST Service Provider/Seller of Goods Location – Noida (STATE- UP) Service Receiver/Buyer of Goods Location –Ghaziabad (STATE-UP) INTRA-STATE Supply CGST & SGST

- 2. PLACE OF SUPPLY OF SERVICES (SECTION 12 & SECTION 13 OF IGST ACT) (A) IMPORT/EXPORT of Services(Section-13) PARTICULARS PLACE OF SUPPLY Service provided to ANY PERSON OUTSIDE INDIA LOCATION OF RECIPIENT If LOCATION OF RECIPIENT IS NOT AVAILABLE LOCATION OF SERVICE PROVIDER (B) DOMESTIC SUPPLY of Services (Section-12) GENERAL RULE PARTICULARS PLACE OF SUPPLY Service PROVIDED TO REGISTERED PERSON LOCATION OF RECIPIENT Service PROVIDED TO UNREGISTERED PERSON ADDRESS OF RECIPIENT ON RECORD (if address on record exists) LOCATION OF SERVICE PROVIDER (in all other cases) SERVICES SPECIFIC RULES PARTICULARS PLACE OF SUPPLY In relation to IMMOVABLE PROPERTY (Architects, Renting of Immovable Property, Lodging in hotel rooms/party halls, Interior Decorators, Estate Agents etc.) LOCATION OF SUCH PROPERTY IF LOCATION of property is OUTSIDE INDIA, LOCATION OF RECIPIENT In case of RESTAURANT and Catering Services, Fitness & BEAUTY TREATMENT, HEALTH SERVICES including cosmetic and plastic surgery etc. Place where such Services ACTUALLY PERFORMED. In case of TRAINING & PERFORMANCE APPRAISAL -Where Supplied to a Registered Person, LOCATION OF SUCH PERSON -Supplied to any other person, WHERE SERVICES ARE ACTUALLY PERFORMED TRANSPORTATION OF GOODS, including by mail & courier -Where Supplied to a Registered Person, LOCATION OF SUCH PERSON -Supplied to any other person, LOCATION AT WHICH GOODS ARE HANDED OVER FOR TRANSPORTATION

- 3. PASSENGER TRANSPORTATION SERVICES - Where Supplied to a Registered Person, LOCATION OF RECIPIENT -Supplied to any other person, LOCATION FROM WHERE THE PASSENGER EMBARKS ON THE CONVEYANCE BANKING & OTHER FINANCIAL SERVICES including stock broking Address of recipient on record, however if address on record is not available, location of service provider. TELECOMMUNICATION SERVICES -FIXED TELECOMMUNICATION LINE, leased circuits, cable or dish antenna – Place WHERE INSTRUMENT has been INSTALLED for receiving service -POSTPAID MOBILE & Internet Services – BILLING ADDRESS on record of recipient of such service -PREPAID MOBILE, internet & DTH Service – (i) Sold through Selling Agent (Franchisee)/Distributor – Address of such seller on record at the time of supply (ii) Sold Directly at CSC Counter – Place where voucher sold (iii) Recharge through electronic mode – Address of recipient on record, however if address on record is not available, location of service provider. DISCLAIMER The interpretation has been made by me, as per my understanding & knowledge of the subject matter in the law. For the confirmation & explanation, we may refer to GST laws & rules thereof. PREPARED BY: CA. JEEVAN CHANDRA Assistant Manager (Taxation) BSNL Corporate Office, New Delhi Mobile: +91 - 9412085553