Andheri Call Girls In 9825968104 Mumbai Hot Models

jaya.docx

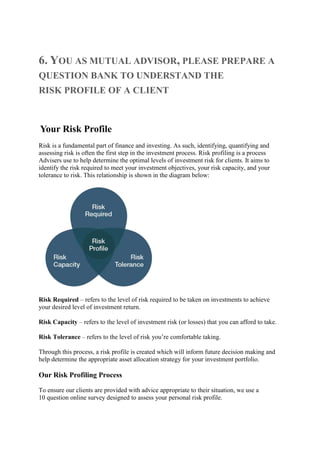

1. 6. YOU AS MUTUAL ADVISOR, PLEASE PREPARE A

QUESTION BANK TO UNDERSTAND THE

RISK PROFILE OF A CLIENT

Your Risk Profile

Risk is a fundamental part of finance and investing. As such, identifying, quantifying and

assessing risk is often the first step in the investment process. Risk profiling is a process

Advisers use to help determine the optimal levels of investment risk for clients. It aims to

identify the risk required to meet your investment objectives, your risk capacity, and your

tolerance to risk. This relationship is shown in the diagram below:

Risk Required – refers to the level of risk required to be taken on investments to achieve

your desired level of investment return.

Risk Capacity – refers to the level of investment risk (or losses) that you can afford to take.

Risk Tolerance – refers to the level of risk you’re comfortable taking.

Through this process, a risk profile is created which will inform future decision making and

help determine the appropriate asset allocation strategy for your investment portfolio.

Our Risk Profiling Process

To ensure our clients are provided with advice appropriate to their situation, we use a

10 question online survey designed to assess your personal risk profile.

2. On completion, clients are provided with an outline of their assigned risk profile and a sample

portfolio of growth and income assets appropriate to this profile type.

Our Risk Profiles

We've adopted six distinctive risk profiles, ranging from conservative to very aggressive. A

conservative profile would likely seek to conserve wealth rather than aim for capital growth,

while an aggressive profile may seek financial gain despite the risks associated with the

investments. Those with a shorter investment horizon or lower levels of capital may be on the

more conservative end of the spectrum, while those with longer investment horizons and

larger capital reserves may find larger levels of risk appropriate.

Our 6 risk profiles are described below:

Conservative

Defensive 85% / Growth 15%

This suits investors with a minimum two-year timeframe or those that seek a portfolio

invested predominantly in interest bearing assets, with a small proportion of growth assets.

This portfolio also suits investors who give a high priority to the preservation of capital and

are therefore willing to accept lower potential investment performance, hence the 85 percent

exposure to income assets (cash and fixed interest).

3. Moderate

Defensive 70% / Growth 30%

This suits investors with a minimum three-year timeframe or those who seek a portfolio with

an emphasis on interest bearing assets, with some exposure to growth asset classes. This

portfolio also suits investors seeking a lower level of investment value volatility, and

therefore willing to accept lower potential investment performance, hence the 70 percent

exposure to income assets (cash and fixed interest).

Balanced

Defensive 50% / Growth 50%

This suits investors with a minimum five-year timeframe. This portfolio also suits investors

who desire a modest level of capital stability but are willing to accept moderate investment

value volatility in return for commensurate potential investment performance, hence the 50

percent exposure to growth assets (shares, listed property and infrastructure) and 50 percent

exposure to income assets (cash and fixed interest).

4. Growth

Defensive 30% / Growth 70%

This suits investors with a minimum seven-year timeframe or those who are willing to accept

higher levels of investment value volatility in return for higher potential investment

performance. Some exposure to interest bearing assets is still desired, but the primary

concern is a higher return, hence the 70 percent exposure to growth assets (shares, listed

property and infrastructure).

Aggressive

Defensive 15% / Growth 85%

5. This suits investors with a minimum nine-year timeframe or those who are willing to accept

high levels of investment value volatility in return for high potential investment performance.

The 85 percent exposure to growth assets (shares, listed property and infrastructure) means

that capital stability is only a minor concern.

Very Aggressive

Defensive 0% / Growth 100%

This suits investors with a minimum ten-year timeframe or those who are willing to accept

very high levels of investment value volatility to maximise potential investment performance.

The 100 percent exposure to growth assets (shares, listed property and infrastructure) means

that capital stability is not a consideration.

How We Use Your Risk Profile

A risk profile should not be viewed as a check-box exercise which is completed and

forgotten. Nor should it be seen as a simple way of grouping clients together and quickly

designing portfolios. The real value of a risk profile is as a strategic document to refer back to

over time that helps keep you on track to achieving your goals. In addition, it should be used

as a tool to initiate deeper conversations between you and your Adviser.

15 Financial Advisor Questions to Ask Your Clients

6. Here are 15 open-ended questions an advisor should ask to create better financial plans for

clients. Try asking these important questions during your next consultation and see if they

help you get a clearer view of what your client needs on their financial plan.

1. What are your current financial concerns?

Most new clients start looking for a financial planner after they notice a problem with their

financial situation.

The answer to this question is why you got hired in the first place, so whatever the client says

here should be your main focus. Knowing the most pressing issues they have at the moment

will help you figure out what they value most and what they want out of the relationship.

2. What are your short- and long-term financial goals?

Assuming what your client needs without clear communication is one of the most common

mistakes financial advisors can make.

True, your job is to give direction and plan your client’s milestones, but at the end of the day,

what they want and how they want to grow their money is up to your client. It’s important to

know your client’s long- and short-term goals so you can create a financial plan that suits

them best.

For example, your client might want to retire in a quiet European city or make enough money

so their children won’t have to work ever again. The plan will be different for each of those

cases, and their financial goals will point you toward the best course of action.

3. What do you hope to gain from financial planning?

If your client has worked with a financial advisor before, they will certainly have

expectations. Asking this question helps you uncover what kind of results or experience

they’re looking for in your advisor-client relationship.

Even if they’ve never worked with an advisor before, they might still have expectations based

on research they may have done previously.

Either way, it’s a great opportunity to explain briefly and simply what it is that you do. For

some clients, the experience may be confusing or intimidating. Having knowledge of these

concerns can help start on the same page as your client.

4. What is the latest update on your current financial situation?

Clients are typically asked to share at least some of this information during intake. However,

asking them this question might uncover some important information that they forgot to

include. Confirming that the data you have is up to date is necessary to make sure that the

advice and plan you come up with are relevant to their present situation.

7. Beyond just updating the information, the answer might open other topics, such as recent life

events that caused a recent financial change — which might cause other changes that your

client isn’t aware of yet.

5. Who are you financially responsible for?

Knowing who your client is financially responsible for is some of the most important

information you can ask for during your consultation. Advice for someone with a spouse and

a child to take care of will be vastly different from the advice you should give to someone

whose only financial responsibility is themselves.

6. Are there any major life changes you predict for the future?

Most of your clients don’t even realize that you need to know about future changes to make a

more robust plan. After all, these changes haven’t even happened yet.

Being warned of any surprises that might throw off your client’s financial plan makes it easy

for you to accommodate those changes in their financial plan. For example, if they’re

planning on moving, welcoming a new family member, receiving a promotion within the

year, or retiring soon, their financial plan may change.

Everyone’s lives are constantly changing. While we can’t predict these changes, your client

might have plans or expect significant changes to happen in their life in the future. It’s

important to be aware of them beforehand, as it puts you in a better position to plan and

prepare for your client.

7. Do you have an attorney, accountant, or insurance agent?

Collaborating with people your client works with gives you a clearer view of their financial

status. Knowing who to contact to ask additional questions is necessary if you’d like someone

to share in-depth information with you.

While your client might inform you of what these professionals said, they might not be

interested in the technical details and nuances of these changes. Knowing how to reach the

source and verifying the details on your own is necessary sometimes.

8. What are you passionate about in life?

Understanding a client’s passions will help you create advice and plans that are more aligned

with their interests and lifestyle. If you’ve had some time to build your relationship, you may

even want to try probing further and find out whether there are certain things — besides

money — that they value highly.

If they’re keen to answer, really listen. This will make your client feel valued and give you

insight that will improve your ability to plan according to their interests. This is how you can

make the most impact on their quality of life as a financial advisor.

9. What has your relationship with money been like?

8. It’s unwise to assume that everyone adopts a similar outlook as you do. People see and

handle money differently — some scrimp, and others are big spenders. Knowing how your

client sees their money helps you understand where they are coming from and therefore aids

you in how to best formulate a plan that resonates with them.

10. What type of investment portfolio loss would make you nervous?

Asking this question will tell you how much of a risk appetite your client has. Knowing how

much they could stand to lose helps you plan an investment strategy that’s more aligned with

what they are comfortable with.

For example, you can steer conservative (risk-averse) clients who are not comfortable with

taking volatility and huge losses towards mutual funds, REITs, and stock indices. Clients

with higher risk tolerance, on the other hand, might prefer high-risk-high-reward investments

like cryptocurrencies and start-ups.

11. Do you currently live off a set budget?

Having an insight into their current budget helps you understand where they are spending

their money. Hearing your client talk about their budget might also help you understand what

kind of priorities they have, so you can make a plan that caters to this.

To help your clients, you need to know how they spend their money. This question gives you

insight into how they handle both income and expenses, which in turn will help you

understand what's important to them. If they have no budget, then that may be one of the first

tasks you have to tackle.

12. Are you invested in the stock market?

Knowing where all your client’s assets are is essential if you’d like to provide relevant

advice. Having this information also lets you factor in your client’s assets in the stock market.

Additionally, knowing your client’s investment philosophy allows you to prepare a backup

plan that will help you advise your clients on how they should manage their finances in case

the market crashes.

13. What stressors keep you up at night?

Money can’t buy happiness, but a lack of money causes problems for most.

Asking this question lets you understand where to focus your client’s finances to help you

alleviate this pain.

For example, your client might be worried about the possibility of being laid off in the

coming months. In this case, what they’re actually worried about might be not only being

able to keep up with their living expenses. Maximizing their emergency fund and reassuring

them that they’d at least be able to dig into it for a few months helps you alleviate that stress

for them.

9. 14. What does retirement look like to you?

A prequel to the popular question, “What will be your monthly expenses in retirement?” This

question makes it easy for clients to envision the kind of environment they’d like to live in as

retirees.

Asking for a budget might give you material for a more concrete plan, but rephrasing it

makes it easier to create a plan that’s more flexible and aligned with your client’s life goals

after retirement.

15. What legacy would you like to leave?

This question is especially necessary if you’re doing retirement planning for your clients. The

legacy they’d like to leave behind is part of the end goal of your financial planning journey.

This information will help you when you’re discussing changes in their life plan, such as

insurance, retirement funds, or adding a new family member.