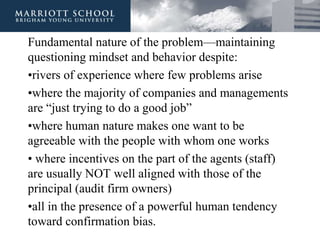

Doug Prawitt discusses maintaining professional skepticism in auditing. Some challenges to skepticism include confirmation bias and misaligned incentives between auditors and clients. There is also a "two-way hindsight problem" where regulators criticize lack of skepticism for problems found post-audit but auditors are not rewarded for extra work without findings. Potential solutions include incentivizing skeptical behaviors, developing ways to document skepticism, aligning auditor and client goals, emphasizing skeptical mindsets, and focusing standards on skepticism over simple compliance. Documentation of skepticism is important but hard to balance with pressures for less subjective judgment.