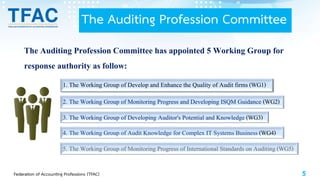

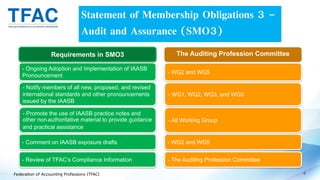

The Auditing Profession Committee oversees standards for the auditing profession in Thailand. It has appointed 5 working groups to carry out its responsibilities: 1) develop and enhance audit firm quality, 2) monitor ISQM guidance, 3) develop auditor potential and knowledge, 4) audit knowledge for complex IT systems, and 5) monitor progress on international auditing standards. The committee adopts and implements IAASB pronouncements, notifies members of changes, comments on exposure drafts, and reviews Thailand's compliance with SMO3 on auditing and assurance. It follows a due process to approve Thai auditing standards, including public exposure, hearings, and TFAC board approval. Recent actions include standards on quality management and revisions