Lack of flood insurance leaves homeowners with financial toll after hurricane florence

•

0 likes•4 views

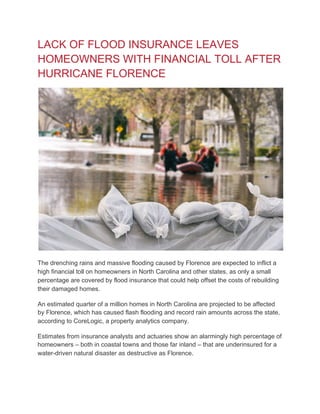

The drenching rains and massive flooding caused by Florence are expected to inflict a high financial toll on homeowners in North Carolina and other states, as only a small percentage are covered by flood insurance that could help offset the costs of rebuilding their damaged homes. An estimated quarter of a million homes in North Carolina are projected to be affected by Florence, which has caused flash flooding and record rain amounts across the state, according to CoreLogic, a property analytics company.

Recommended

More Related Content

What's hot

What's hot (18)

Similar to Lack of flood insurance leaves homeowners with financial toll after hurricane florence

Similar to Lack of flood insurance leaves homeowners with financial toll after hurricane florence (20)

More from HaulTail

More from HaulTail (20)

Recently uploaded

Recently uploaded (20)

Lack of flood insurance leaves homeowners with financial toll after hurricane florence

- 1. LACK OF FLOOD INSURANCE LEAVES HOMEOWNERS WITH FINANCIAL TOLL AFTER HURRICANE FLORENCE The drenching rains and massive flooding caused by Florence are expected to inflict a high financial toll on homeowners in North Carolina and other states, as only a small percentage are covered by flood insurance that could help offset the costs of rebuilding their damaged homes. An estimated quarter of a million homes in North Carolina are projected to be affected by Florence, which has caused flash flooding and record rain amounts across the state, according to CoreLogic, a property analytics company. Estimates from insurance analysts and actuaries show an alarmingly high percentage of homeowners – both in coastal towns and those far inland – that are underinsured for a water-driven natural disaster as destructive as Florence.

- 2. Only 10 percent to 20 percent of coastal homeowners in the hard-hit eastern part of North Carolina, for example, have coverage through the government’s National Flood Insurance Program (NFIP), and only 1 percent to 3 percent of homes in inland counties have flood policies, according to estimates from John Rollins, an actuary at consulting firm Milliman. Statewide, roughly 3 percent of the homes in North Carolina have flood coverage and 8 percent of homeowners are covered in South Carolina, Rollins said. “Obviously, that leaves a lot of people uninsured,” says Rollins. The numbers of those covered are low, he said, because people think that because their home isn’t in a high-risk zone designated by the government that there’s “zero risk” of a flood. “But that’s not true,” Rollins says. Many also don’t realize their basic homeowners policy doesn’t cover flood damage, while others overestimate the disaster aid they will get from the government. Unfortunately, standard homeowners insurance won’t cover any flooding-related issues. The estimated insured losses from Florence are in the range of $3 billion to $5 billion, according to CoreLogic. Goldman Sachs, a Wall Street bank, said they could go as high as $10 billion to $20 billion. Insurers should have no problem being able to pay out claims to policy holders because the industry has cash reserves of roughly half a trillion dollars, according to Matt Carletti, senior insurance analyst at JMP Securities. The problem for homeowners is that insured losses generally are only about one-third of total economic losses, which puts them on the hook financially for a more sizable part of their home rebuilds if losses are due to uncovered flood costs, Carletti said. To get flood coverage, homeowners must buy a separate policy. Most purchase this extra coverage from the government-backed NFIP program, which is designed to restore your home to its preflood condition and replace your possessions. NFIP policies, which carry average premiums of about $600 to $700 a year but can run into the thousands of dollars in high-risk zones, cover up to $250,000 for a home’s structure and up to $100,000 for personal possessions. Homeowners not covered for flood damage can seek federal disaster assistance in the form of grants from the Federal Emergency Management Agency or apply for a loan from the Small Business Administration, said Steve Bowen, meteorologist for Aon Benfield’s Impact Forecasting division. FEMA may provide up to $33,000 in assistance

- 3. for home repair, although the average for Superstorm Sandy in 2012 was about $8,000 and roughly $7,100 for Hurricane Katrina in 2005. At the end of July, there were 134,306 active NFIP flood policies in place in North Carolina, Bowen said. That’s only 3 percent of the estimated 4.62 million housing units in the state, he said, citing U.S. Census Bureau data. Damage to homes caused by floods tend to be costly. The estimated potential loss for a 1,000-square-foot, single-story home with possessions worth $20,000 that is inundated with just 1 inch of interior water can run as high as $11,000, according to FEMA data, and the estimated loss for 5 inches of water climbs to more than $18,000. Given the fact that many parts of North Carolina have received rain totals of 2 feet or more, many homeowners will be facing high rebuild costs they may not be able to afford. “You are looking at a lot of homeowners that will have out-of-pocket costs that could easily be five figures, or more than $10,000,” said Cathy Seifert, an insurance analyst at CFRA, a Wall Street research firm.