1. Date: August 19, 2010

Canadian Composite Index of Leading Indicators

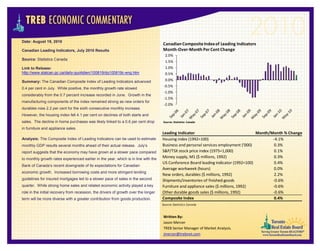

Canadian Leading Indicators, July 2010 Results Month-Over-Month Per Cent Change

2.0%

Source: Statistics Canada

1.5%

Link to Release: 1.0%

http://www.statcan.gc.ca/daily-quotidien/100819/dq100819c-eng.htm 0.5%

Summary: The Canadian Composite Index of Leading Indicators advanced 0.0%

-0.5%

0.4 per cent in July. While positive, the monthly growth rate slowed

-1.0%

considerably from the 0.7 percent increase recorded in June. Growth in the

-1.5%

manufacturing components of the index remained strong as new orders for

-2.0%

durables rose 2.2 per cent for the sixth consecutive monthly increase.

However, the housing index fell 4.1 per cent on declines of both starts and

sales. The decline in home purchases was likely linked to a 0.6 per cent drop Source: Statistics Canada

in furniture and appliance sales.

Leading Indicator Month/Month % Change

Analysis: The Composite Index of Leading Indicators can be used to estimate Housing index (1992=100) -4.1%

monthly GDP results several months ahead of their actual release. July’s Business and personal services employment ('000) 0.3%

report suggests that the economy may have grown at a slower pace compared S&P/TSX stock price index (1975=1,000) 0.1%

to monthly growth rates experienced earlier in the year, which is in line with the

Money supply, M1 ($ millions, 1992) 0.3%

US Conference Board leading indicator (1992=100) 0.4%

Bank of Canada’s recent downgrade of its expectations for Canadian

Average workweek (hours) 0.0%

economic growth. Increased borrowing costs and more stringent lending

New orders, durables ($ millions, 1992) 2.2%

guidelines for insured mortgages led to a slower pace of sales in the second Shipments/inventories of finished goods -0.6%

quarter. While strong home sales and related economic activity played a key Furniture and appliance sales ($ millions, 1992) -0.6%

role in the initial recovery from recession, the drivers of growth over the longer Other durable goods sales ($ millions, 1992) -0.6%

term will be more diverse with a greater contribution from goods production. Composite Index 0.4%

Source: Statistics Canada

Written By:

Jason Mercer

TREB Senior Manager of Market Analysis.

jmercer@trebnet.com