1

PRESENTED BY:

Using homeequity to close the

retirement income gap

Bruce E. Simmons, CRMP

Reverse Mortgage Manager, NMLS ID License #409914

2.

22

“I want toretire and

stay in my home, but I

need a new roof, new

windows and an

updated kitchen.”

“I have several

high interest

credit cards and

an auto loan. I

wish I could

reduce my

monthly bills.”

“Making that

monthly

mortgage

payment is tough

sometimes.”

“I’m looking to

move but am not

sure if I will qualify

for a mortgage

now that I’m

retired.”

“I would love a

safety net – a

line of credit to

use in case of

emergencies.”

3.

3

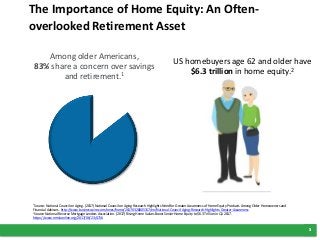

The Importance ofHome Equity: An Often-

overlooked Retirement Asset

3

Among older Americans,

83% share a concern over savings

and retirement.1

1Source: National Council on Aging. (2017) National Council on Aging Research Highlights Need for Greater Awareness of Home Equity Products Among Older Homeowners and

Financial Advisors. http://www.businesswire.com/news/home/20170328005317/en/National-Council-Aging-Research-Highlights-Greater-Awareness

2Source: National Reverse Mortgage Lenders Association. (2017) Rising Home Values Boost Senior Home Equity to $6.3 Trillion in Q1 2017.

https://www.nrmlaonline.org/2017/06/23/4716

US homebuyers age 62 and older have

$6.3 trillion in home equity.2

4.

4

Three Ways toAccess Home Equity

1.Sell the House and Move

– Downsize or rent and use the equity

– Cost = approx. 10% of home value

(sales commission, moving expenses)

– Can be disruptive

2.Traditional Home Equity Line or Loan

– Monthly repayments are required

– Draw periods are limited

3. Home Equity Conversion Mortgage (HECM)

– Designed specifically for homeowners age 62+

– Commonly known as a reverse mortgage

– If you’re living in the “right” home and you plan to

stay, or want to buy a different home

– A highly flexible loan option

– FHA-insured*

*This material has not been reviewed, approved or issued by HUD, FHA or any government agency. The company is not affiliated with or acting on

behalf of or at the direction of HUD/FHA or and other government agency.

5.

5

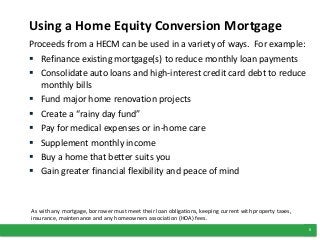

Using a HomeEquity Conversion Mortgage

Proceeds from a HECM can be used in a variety of ways. For example:

Refinance existing mortgage(s) to reduce monthly loan payments

Consolidate auto loans and high-interest credit card debt to reduce

monthly bills

Fund major home renovation projects

Create a “rainy day fund”

Pay for medical expenses or in-home care

Supplement monthly income

Buy a home that better suits you

Gain greater financial flexibility and peace of mind

As with any mortgage, borrower must meet their loan obligations, keeping current with property taxes,

insurance, maintenance and any homeowners association (HOA) fees.

6.

6

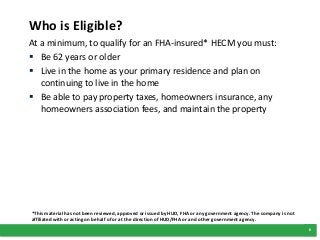

Who is Eligible?

Ata minimum, to qualify for an FHA-insured* HECM you must:

Be 62 years or older

Live in the home as your primary residence and plan on

continuing to live in the home

Be able to pay property taxes, homeowners insurance, any

homeowners association fees, and maintain the property

*This material has not been reviewed, approved or issued by HUD, FHA or any government agency. The company is not

affiliated with or acting on behalf of or at the direction of HUD/FHA or and other government agency.

7.

7

What Types ofHomes Are Eligible?

Single-family homes

FHA-approved* condominiums

Townhouses or Planned Unit Developments (PUDs)

Two- to four-family homes

Manufactured homes meeting HUD guidelines

*This material has not been reviewed, approved or issued by HUD, FHA or any government agency. The company is not

affiliated with or acting on behalf of or at the direction of HUD/FHA or and other government agency.

8.

8

Options for ReceivingYour Funds

Lump Sum - Draw all the available funds at closing. The only

option available on fixed-rate loans.

Line of Credit - Allows you to draw funds at your discretion

when you want or need them

Tenure - Equal monthly installments for as long as you live in

the home.

Term - Equal monthly installments over a fixed period of time.

Or a combination of the above

You can also change how you receive any remaining funds in

the future

Borrowers who elect a fixed rate loan will receive a single disbursement lump sum payment. Other payment

options are available only for adjustable rate mortgages.

9.

9

Case Study 1:Dramatically Reduce

Mortgage Payments

Mary, age 67

Burdened by monthly mortgage payments

Refinances with a HECM

Benefits:

Payment flexibility: No minimum monthly mortgage payment

This frees up funds for other things

As with any mortgage, she must meet her loan obligations,

keeping current with property taxes, insurance, maintenance and

any homeowners association (HOA) fees

Loan does not have to repaid until she sells the home, passes

away or moves out

10.

10

Case Study 2:Consolidate Debt to Reduce

Monthly Bills

Jenny, age 63

Has an existing mortgage, plus $50,000 in credit card and auto loan debts

Consolidates her debts by refinancing them into a HECM

Benefits:

Eliminates credit card and auto loan payments

Greatly improves monthly cash flow

Monthly principal and interest payments are optional — greater

financial flexibility

As with any mortgage, she must meet her loan obligations: keeping

current with property taxes, insurance, maintenance, and any

homeowners association fees

After paying off her existing debts, has enough left to create a line of

credit that will grow over time* and will be there as a source of future

funds

*If part of the loan is held in a line of credit upon which the borrower may draw, then the unused portion of the line of credit will grow in size

each month. The growth rate is equal to the sum of the interest rate plus the annual mortgage insurance premium rate being charged on the

loan.

11.

11

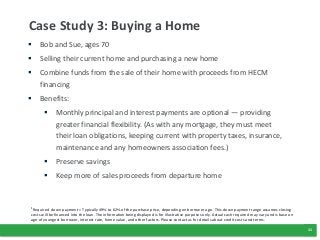

Case Study 3:Buying a Home

Bob and Sue, ages 70

Selling their current home and purchasing a new home

Combine funds from the sale of their home with proceeds from HECM

financing

Benefits:

Monthly principal and interest payments are optional — providing

greater financial flexibility. (As with any mortgage, they must meet

their loan obligations, keeping current with property taxes, insurance,

maintenance and any homeowners association fees.)

Preserve savings

Keep more of sales proceeds from departure home

1Required down payment = Typically 49% to 62% of the purchase price, depending on borrower age.. This down payment range assumes closing

costs will be financed into the loan. The information being displayed is for illustrative purposes only. Actual cash required may vary and is base on

age of youngest borrower, interest rate, home value, and other factors. Please contact us for details about credit costs and terms.

12.

12

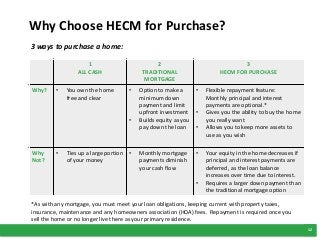

1

ALL CASH

2

TRADITIONAL

MORTGAGE

3

HECM FORPURCHASE

Why? • You own the home

free and clear

• Option to make a

minimum down

payment and limit

upfront investment

• Builds equity as you

pay down the loan

• Flexible repayment feature:

Monthly principal and interest

payments are optional.*

• Gives you the ability to buy the home

you really want

• Allows you to keep more assets to

use as you wish

Why

Not?

• Ties up a large portion

of your money

• Monthly mortgage

payments diminish

your cash flow

• Your equity in the home decreases if

principal and interest payments are

deferred, as the loan balance

increases over time due to interest.

• Requires a larger down payment than

the traditional mortgage option

*As with any mortgage, you must meet your loan obligations, keeping current with property taxes,

insurance, maintenance and any homeowners association (HOA) fees. Repayment is required once you

sell the home or no longer live there as your primary residence.

3 ways to purchase a home:

Why Choose HECM for Purchase?

13.

13

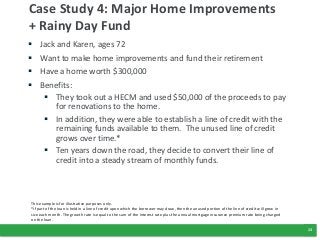

Case Study 4:Major Home Improvements

+ Rainy Day Fund

Jack and Karen, ages 72

Want to make home improvements and fund their retirement

Have a home worth $300,000

Benefits:

They took out a HECM and used $50,000 of the proceeds to pay

for renovations to the home.

In addition, they were able to establish a line of credit with the

remaining funds available to them. The unused line of credit

grows over time.*

Ten years down the road, they decide to convert their line of

credit into a steady stream of monthly funds.

This example is for illustrative purposes only.

*If part of the loan is held in a line of credit upon which the borrower may draw, then the unused portion of the line of credit will grow in

size each month. The growth rate is equal to the sum of the interest rate plus the annual mortgage insurance premium rate being charged

on the loan.

14.

14

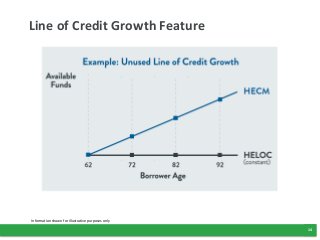

Line of CreditGrowth Feature

Information shown for illustrative purposes only

15.

15

Contact me atanytime to learn more:

Bruce E. Simmons, CRMP

Reverse Mortgage Manager,

NMLS #409914

American Liberty Mortgage, Inc.

1932 W 33rd Ave.

Denver, CO 80211

Branch NMLS #1462

303-467-7821

bruce@almortgageinc.com

Questions?

This material has not been reviewed, approved or issued by HUD, FHA or any government agency. The company is not affiliated with or acting on behalf of or at the direction of

HUD/FHA or any other government agency.

American Liberty Mortgage, Inc., 1932 W. 33rd Ave., Denver, CO 80211, NMLS #1462. Regulated by the Colorado Division of Real Estate..

L1526-Exp122018