1. 1 University of Oregon Investment Group

Presentation Date

Sector

Covering Analysts: Name

Investment Thesis

FMC’s transition from a diversified chemical company to a simpler, more

focused, agricultural, health and nutrition company will make them more

reliant on the performance of the agricultural industry.

FMC’s higher multiples relative to comparable peers suggest that it is

currently trading at a slight premium.

Larger debt positions and the increasing need for more investment research

and development to produce new technologies will limit the cash that is

available to shareholders.

High inflation and import restrictions in Argentina, combined with slowing

demand in China for high-end protein beverages, and the challenging

environment in the agricultural markets will reduce FMC’s earnings in the

next twelve months.

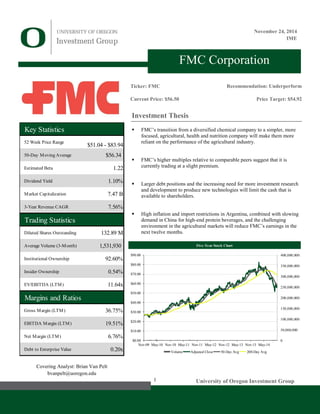

Five-Year Stock Chart

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

400,000,000

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

Nov-09 May-10 Nov-10 May-11 Nov-11 May-12 Nov-12 May-13 Nov-13 May-14

Volume Adjusted Close 50-Day Avg 200-Day Avg

FMC Corporation

Ticker: FMC

Current Price: $56.50

Recommendation: Underperform

Price Target: $54.92

Key Statistics

52 Week Price Range

50-Day Moving Average $56.34

Estimated Beta 1.22

Dividend Yield 1.10%

Market Capitalization 7.47 B

3-Year Revenue CAGR 7.56%

Trading Statistics

Diluted Shares Outstanding 132.89 M

Average Volume (3-Month) 1,531,930

Institutional Ownership 92.60%

Insider Ownership 0.54%

EV/EBITDA (LTM) 11.64x

Margins and Ratios

Gross Margin (LTM) 36.75%

EBITDA Margin (LTM) 19.51%

Net Margin (LTM) 6.76%

Debt to Enterprise Value 0.20x

$51.04 - $83.94

Covering Analyst: Brian Van Pelt

bvanpelt@uoregon.edu

November 24, 2014

IME

2. UOIG 2

University of Oregon Investment Group

Business Overview

John Bean founded FMC Corporation in 1883 in Los Gatos, CA under the name

Bean Spray Pump Company. The company’s first product was the piston pump,

which was used to spray insecticides on many of the fruit orchards in the area. In

1948, the company changed its name to Food Machinery and Chemical

Corporation following the acquisition of two canning machinery companies in

1928, and Bolens Lawn and Garden Equipment in 1946. Since then, FMC has

manufactured a wide variety of products including landing vehicle-tracked

vehicles (LVT’s), fire truck pumps and pumper bodies, cranes and excavators,

even Armored Personnel Carriers for the United States War Department during

WWII. Today, FMC is a diversified chemical company that operates in three

segments: FMC Agricultural Solutions, FMC Health and Nutrition, and FMC

Minerals. FMC serves customers in four geographic regions: North America,

Latin America, Europe, the Middle East and Africa (EMEA), and Asia Pacific.

It is headquartered in Philadelphia, PA and has approximately 5,600 employees.

Business Segment Analysis

FMC Agricultural Solutions

The FMC Agricultural Solutions segment, which accounted for approximately

55% of FMC’s 2013 revenue, is the company’s largest and fastest growing

segment. This segment develops, manufactures, markets, and sells a wide

variety of crop protection, pest control, and lawn and garden products. The FMC

Agricultural Solutions product portfolio is comprised of three major pesticide

categories: herbicides (protect crops from weed growth), insecticides (protect

crops from insects), and fungicides (protect fruits and vegetables from fungal

disease).

FMC Agricultural Solutions is the leading global supplier of technology-based

crop protection products that serve niche crop markets. FMC works closely with

customers to develop differentiated, technically superior products to meet

rapidly changing market needs. FMC then exclusively sells these products

through their global market access positions.

FMC Agricultural Solutions is global in scope but holds particular strength in

the Americas. They are able to access key markets across the globe through

their own sales and marketing organization, independent distributers, and joint

venture agreements.

Over the past five years, revenue in this segment has increase at a compound

annual growth rate (CAGR) of 15.33%. The majority of growth in recent years

has largely been driven by FMC’s expansion into South America, which

includes the large agricultural market of Brazil. Going forward, FMC expects to

maintain and enhance their access positions in key agricultural markets, and

continue to develop new high-margin niche products that will enable them to

compete effectively.

FMC Health and Nutrition

Source: FMC 10-K

33%

36%

18%

13%

North America

Latin America

Asia Pacific

EMEA

Figure 1: Revenue by Region - 2013

Source: FMC 10-K

24%

55%

15%

6%

North America

Latin America

Asia Pacific

EMEA

Figure 3: Agricultural Solutions Revenue by

Region - 2013

Source: FMC 10-K

Figure 2: Agricultural Solutions Revenue and

Operating Margin 2009 - 2013

$1,052 $1,242

$1,465

$1,764

$2,146

0%

10%

20%

30%

40%

50%

60%

$0

$500

$1,000

$1,500

$2,000

$2,500

2009 2010 2011 2012 2013

Revenue (millions) Operating Margin

3. UOIG 3

University of Oregon Investment Group

The FMC Health and Nutrition Segment focuses on high performance food

ingredients, nutraceuticals, pharmaceutical ingredients, and other specialty

consumer products to meet increasing global demand for nutritious and

convenient foods, effective pharmaceuticals, and beneficial nutrient

supplements. The segment consists of six naturally derived products:

microcrystalline cellulose (MCC) from specialty grades of wood pulp,

carrageenan and alginates from seaweed, natural colorants from plants and

select insect species, pectin from citrus fruit peels, and omega-3 from fish oil.

The primary focus of the Health and Nutrition segment is on food and

pharmaceutical markets, but FMC has worked to expand its presence in

nutraceuticals, cosmetics, and other related product categories. Product offerings

serving the food markets principally provide texture, structure, and physical

stability (TSPS) to stabilize and thicken certain food products. In the

pharmaceutical industry, products function as binders, disintegrants, control-

release compounds, and suspending agents for the production of both liquid and

solid pharmaceutical products.

Revenue in this segment accounted for approximately 20% of total revenue in

2013 and has increased at a 5.6% CAGR over the past five years. FMC Health

and Nutrition continues to strengthen its business in emerging markets,

particularly in Asia where demand for MCC used in foods and high-protein

beverages continues to rise. While in developed economies, FMC is continuing

to grow sales by enhancing color, texture, structure and stability in food

products.

FMC Minerals

The FMC Minerals segment is FMC’s least diverse segment and accounted for

approximately 25% of company revenue in 2013. This segment consists of only

two divisions: Alkali Chemicals and Lithium, which accounted for 77% and

23% of segment revenue in 2013, respectively.

The Alkali Chemicals division is the world’s largest producer of natural soda

ash, a primary ingredient used to produce glass. Historically, the large cash

proceeds generated by this division helped cover the operational expenses of

other divisions within the company. However, in September FMC announced

that it plans to sell the Alkali Chemicals division midway through 2015 to help

leverage the acquisition of Cheminova A/S.

Thus, going forward the FMC Minerals segment will only consist of the lithium

business. FMC extracts lithium from its lithium brines in Argentina. Lithium is

used for batteries, polymers, pharmaceuticals, greases and lubricants, glass and

ceramics, and other industrial uses. Although lithium can be sold into a variety

of different end markets, FMC has focused their strategy on energy storage,

polymer, and pharmaceutical uses.

Business Growth Strategies

Figure 5: Health and Nutrition Revenue by

Region - 2013

Source: FMC 10-K

32%

9%

25%

34%

North America

Latin America

Asia Pacific

EMEA

Figure 4: Health and Nutrition Revenue and

Operating Margin 2009 - 2013

Source: FMC 10-K

$580 $611

$654 $681

$762

0%

10%

20%

30%

40%

50%

60%

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

2009 2010 2011 2012 2013

Revenue (millions) Operating Margin

Figure 6: FMC Minerals Revenue and

Operating Margin 2009 - 2013

Source: FMC 10-K

$748 $837

$918

$966 $970

0%

10%

20%

30%

40%

50%

60%

$0

$200

$400

$600

$800

$1,000

$1,200

2009 2010 2011 2012 2013

Revenue (millions) Operating Margin

4. UOIG 4

University of Oregon Investment Group

In 2010, FMC presented its revised corporate strategy and business growth plan

for the next five years. This plan, named Vision 2015, focuses on driving sales

and earnings growth through organic growth, targeted acquisitions, and active

portfolio management. Vision 2015 has five key elements:

.

Growing Leadership Positions

FMC plans to continue to strengthen their market-leading positions primarily

through organic growth, which will be complemented by a focused external

growth strategy.

FMC Agricultural Solutions is focused on new product and market innovations

to drive organic growth. Organic growth in this segment comes from moving

into new crops or expanding solutions for existing crops. Growers are constantly

demanding new pesticides that increase crop yields, and over time certain

insects, weeds, and funguses develop immunities to certain crop protection

chemicals. Therefore, FMC’s growth in this segment will be dependent on their

ability to develop environmentally compatible and sustainable customer-based

solutions, and quickly bring them to market. FMC plans to compliment this

organic growth through targeted acquisitions, such as the acquisition of

Cheminova, which add new products and technologies to their portfolio, and

allow them to strengthen their market access and enter into adjacent spaces.

In FMC Health and Nutrition, new products and new applications for existing

products will drive organic growth in the upcoming years. The external growth

efforts in this segment are directed towards product and small company

acquisitions that complement existing supply chain competencies and serve

similar end markets as their current products (food ingredients, pharmaceuticals,

nutraceuticals, etc.).

The FMC Minerals segment is focused on growing their leadership positions

through organic growth that is driven by decreasing the unit cost production of

lithium. This segment evaluates acquisitions opportunistically and therefore

does not have an active external growth strategy.

Increasing Reach

Rapidly develop economies have been the main focus of FMC’s geographic

growth initiatives over the past couple years. FMC plans to further strengthen

their position in RDEs, particularly in Latin America and East Asia. Growth in

Latin America will depend on FMC’s ability to leverage their FMC Agricultural

Solutions leadership positions and expand into new markets such as Argentina

and Central America. In Asia, FMC is investing in human, scientific, and

technological resources across the region, such as their new MCC plant in

Thailand, to gain market access and increase their reach.

Capturing the Value of Common Ownership

FMC has gradually shifted their organizational structure from a decentralized

model to one that has both centralized and decentralized qualities, to better

leverage size and scale. The priority areas of this shift are procurement, global

supply chain, and RDE infrastructure. FMC believes that this balanced model

Figure 7: Vision 2015 Logo

Source: Google Images

Figure 9: FMC Asia Innovation Center –

Shanghai, China

Source: FMC Presentation

Source: FMC Presentation

Figure 8: Agricultural Innovation Focus

5. UOIG 5

University of Oregon Investment Group

will help them realize efficiencies, while maintaining strong accountability

across all their business units.

Proactive Management of the Business Portfolio

FMC is constantly assessing the performance of all of their business divisions

and product lines to make sure that all businesses are well positioned for

sustained economic growth. If FMC believes that a business or product line has

become non-core or lacks economical sustainability, it will take the appropriate

actions, such as the divestiture of the FMC Peroxygens segment in 2013, the exit

of the zeolites product line in 2012, and the exit of the sodium percarbonate

product line in 2011. A complete summary of FMC’s proactive portfolio

management can be found in Appendix 7.

Disciplined Cash Deployment

FMC’s external growth strategy is not expected to consume all the cash

available for deployment. Thus, the final element of FMC’s Vision 2015

strategic plan is to return a significant amount of cash to shareholders through

share repurchases and cash dividends. In April 2013, the board of directors

authorized the repurchase of up to $500 million of common shares. However,

FMC has not repurchased any shares in 2014.

Strategic Positioning

Since 2010, FMC has engaged in numerous acquisitions, strategic alliances,

collaborations, and dispositions of non-core businesses, as part of their proactive

portfolio management. This activity and corporate restructuring has resulted in a

business that looks significantly different than it did five years ago. Therefore, to

effectively analyze the strategic positioning of FMC, it is beneficial to look at

the strategic positioning of each individual segment.

FMC Agricultural Solutions

This segment has experienced the least amount of structural change over the past

five years. It continues to develop, manufacture, and sell pesticides to customers

globally, and is still the main driver of company revenue. Although FMC has

explicitly stated in the past that its external growth strategy excludes making

large-scale, transformational acquisitions, they made a splash in September with

the announcement to acquire Cheminova.

Cheminova is a privately owned Danish crop protection company that had $1.3

billion in revenues in 2013 (roughly 1/3 of FMC’s 2013 revenue). The deal will

transform FMC into much more of a pure play agrochemical company with

FMC Agricultural Solutions revenues projected to represent 77% of total

company revenue pro forma (up from 55% in 2013).

The Cheminova acquisition will significantly strengthen FMC’s market access

in Europe, as well as in Latin America, and select Asian countries. Cheminova

has an attractive portfolio of over 60 active ingredients, which will add to a

robust innovation pipeline and enhance FMC’s ability to deliver new and

differentiated products.

Figure 11: Cheminova Logo

Source: Google Images

Figure 10: Notable Acquisitions and Dispositions

Source: FMC Presentation

Proactive Portfolio Management

Dispositions:

Phosphates (2010)

SodiumPercarbonates (2011)

Zeolites / Silicates (2012)

Peroxygenst (2014)

Alkali Chemicals (2015 E)

Acquisitions:

Phytone (natural colorants) (2012)

Pectin Italia (2012)

Epax(omega-3) (2013)

Cheminova (2015 E)

6. UOIG 6

University of Oregon Investment Group

In addition to targeted acquisitions, FMC frequently enters into strategic

alliances and collaborations with other agrochemical companies to increase

market access and gain new technologies. In 2013, FMC entered into an

exclusive collaboration with Chr. Hansen, a leading global biosciences

company, which was complemented with the acquisition of the assets of the

Center for Agricultural and Environmental Biosolutions (CAEB). The two

separate transactions give FMC a strong foundation for developing biologically

based products that enhance farmer’s yields and respond to evolving pest

pressures and resistance.

As a result of their recent acquisitions and strategic alliances, FMC believes they

are well positioned to meet rapidly changing market demand for innovative and

technology based crop protection chemicals. They will continue to use active

ingredient innovation and formulation science to focus on higher-margin niche

crops and pockets of technical differentiation in row crops.

FMC Health and Nutrition

Formerly reported as the Specialty Chemicals segment, the FMC Health and

Nutrition segment was created in 2013 after the divestiture of the FMC

Peroxygens business. FMC Health and Nutrition has positioned itself to meet

growing demand in the food ingredient, pharmaceutical, and nutraceutical end

markets by expanding their natural product line through the acquisitions of Epax

(2013), Pectine Italia S.p.A (2012), and Phytone Ltd (2012).

Epax is a global supplier of omega-3 fatty acid concentrates derived from fish

oils. Going forward, FMC believes that its UK Seal Sands facility, which uses

advanced technology to manufacture high purity, high-concentration Omega-3

products, will enable cost-effective penetration into the pharmaceutical and

nutraceutical end markets.

Pectine Italia S.p.A produces pectin, a stabilizing and thickening agent derived

from citrus peels that is used in a variety of foods. Phytone Ltd. is a producer of

natural colorants that are used by customers in the food, beverage, and personal

care sectors. These acquisitions have provided FMC Health and Nutrition with a

diverse portfolio of biopolymers that serve multiple different end markets. As a

result, FMC Health and Nutrition is the FMC’s least cyclical business segment.

FMC Minerals

In September, FMC announced that it plans to sell the Alkali Chemicals division

to help leverage the acquisition of Cheminova. Therefore, the FMC Minerals

segment will just consist of the lithium business in the future.

FMC has focused their Lithium efforts on the energy storage, polymer, and

pharmaceutical markets. They have also invested heavily in manufacturing

additions in recent years to try and achieve what they refer to as “operational

excellence”. As a result, FMC has experience 12 consecutive months of

improved operations and record volumes at their lithium processing facility in

Figure 12: FMC’s Revenues Pro Forma

Source: FMC Earnings Call

77%

18%

5%

FMC Agricultural

Solutions

FMC Health and

Nutrition

FMC Minerals

Figure 13: 2015 Product Lines

Source: UOIG Spreads

Segment Products

Agricultural Soloutions Herbicides

Inseticides

Fungicides

Health andNutrition MCC

Carrageenans

Alginates

Natural Colorants

Pectin

Omega-3 EPA/DHA

Minerals Lithium

Soda Ash

Source: Google Images

Figure 14: Lithium Brines

7. UOIG 7

University of Oregon Investment Group

Argentina. Thus, FMC is well positioned to capitalize on increasing global

demand for lithium.

Industry

FMC is classified as operating in the diversified chemicals industry. However,

the industry is way too diverse and broad in scope to provide a meaningful

analysis for FMC. Therefore, it is better to look at the specialized industries in

which each FMC segment operates.

Pesticide Industry

The pesticide industry is a mature industry that consists of companies that

manufacture crop protection chemicals. Currently, there are fewer than 20 basic

manufacturers of pesticide chemicals (Fredonia Group). Since the pesticide

industry can increase crop yields and boost farm productivity, it is considered an

integral component of the agricultural sector and is heavily dependent on

agricultural production. IBISWorld projects the pesticide industry to grow at an

average annual rate of 3.4% from 2014-2019.

Aside from general factors such as local climate, soil conditions, and prevalence

of harmful agricultural pests, demand is mainly determined by farm incomes and

demand from crop production. Farm incomes can be influenced by a number of

factors, but are primarily driven by commodity prices and the level of

government subsidies available to farmers. Agricultural commodity prices are

measured by the Agricultural Price Index (API), which measures the costs of all

agricultural products. The API is projected to decrease in the upcoming years,

posing a threat to the pesticide industry.

Technological innovations in the agricultural industry are also posing a major

threat to the pesticide industry; the main one being the use of genetically

modified (GM) seeds. GM seeds typically produce greater farm yields and are

designed to be significantly more resistant to pests, thereby reducing the demand

for pesticides. Without widespread consumer concern and government

regulations dictating change, the commercial use of GM seeds is likely to

increase over the next 5-10 years.

Other external factors that could negatively impact the pesticide industry in the

immediate future include increasing health and environmental concerns about

the use of pesticides, and the resulting rise in environmental compliance costs.

Thus, continued product innovation will be a very important part of the industry

going forward as the demand for safer and more carefully designed chemicals

increases.

Despite having fewer than 20 basic manufacturers, competition in the pesticide

industry is relatively limited due to the highly differentiated nature of products.

The top six players in the industry account for approximately 65% of the

industry’s global sales. However, rather than competing with the industry

leaders in sales volume, FMC competes with the next tier of agrochemical

companies through unique technologies that focus on specific crops, markets,

and geographic regions.

Source: IBISWorld

Figure 15: Pesticide Industry Characteristics

Life Cycle Stage: Mature

Concentration Level: Medium

Competition Level: Low

Revenue Volatiliity: Medium

Capital Intensity: High

Technology Change: High

Regulation Level: Very High

Industry Assistance: Medium

Barriers to Entry: High

Industry Globalization: Medium

Pesticide Industry

Figure 16: Agricultural Price Index 2006-2020

Source: IBISWorld

Figure 17: Product and Services Segmentation

- 2014

Source: IBISWorld

60%20%

10%

10%

Herbicides

Insecticides

Fungicides

Other

8. UOIG 8

University of Oregon Investment Group

Organic Chemicals Industry

The organic chemicals industry is an extremely diverse industry with hundreds

of competing firms that produce thousands of various chemical products. Unlike

the agrochemical industry, concentration in the industry is low, with the top

players accounting for less than 5% of total industry revenue. The industry

experienced significant growth from 2009-2014 as the economy recovered from

the recession and industrial production increased. However, due its mature

nature, the organic chemicals industry is only expected to grow at an annual rate

of 3.1% from 2014-2019 (IBISWorld).

Much of the demand growth in the industry is driven by increasing demand in

downstream and end markets. In the case of FMC, growth within its Health and

Nutrition segment will result from growing demand in food ingredient,

pharmaceutical, and nutraceutical end markets. Demand in these end markets is

expected to increase as a result of new product innovations and increased

consumption of processed foods and pharmaceuticals in rapidly developing

economies, particularly in Asia.

Key external drivers of the organic chemical industry include consumer

spending, the world price of crude oil, and industrial production. Consumer

spending is expected to increase at an average annual rate of 2.6% over the next

five years (IBISWorld). This will increase demand in certain end markets, as

increased consumer spending will result in greater sales of consumer goods.

Just like the pesticide industry, increased regulation could significantly impact

the organic chemical industry in upcoming years, resulting in higher operational

costs for chemical manufacturers. However, FMC is not as sensitive to this risk

as other industry competitors because they do not have a product portfolio

consisting of environmentally hazardous or dangerous chemicals.

The market for food ingredients consists of a large number of competitors

because of the broad spectrum of chemistries employed. FMC’s main

competitors in the food ingredient industry include DuPont, Cargill, J.M. Huber

Corporation, and Kerry Group plc. Competitors in the pharmaceutical and

nutraceutical ingredient markets tend to be grouped by chemistry. For example,

FMC’s main MCC competitors include Ming Tai Chemical Co., Ltd, and

Blanver Farmoquimica Ltda, whereas in omega-3, FMC’s main competitors are

BASF AG, DSM and Croda International. Thus, industry participants focus less

on other competitors, and more on developing innovative new products and

finding new applications for existing products.

Lithium

There are currently only three key producers of lithium compounds in the world:

FMC, Rockwood Holdings, Inc., and Sociedad Química y Minera de Chile S.A.

Lithium is extracted from the water of brine deposits. The electrochemical

properties make it an ideal material for portable energy storage in applications

such as smart phones, laptops, tablets, hybrid electric vehicles, and other next

generation energy storage technologies.

Figure 20: Lithium Demand 2002 - 2012

Source: 2015 Tru Group Research

Life Cycle Stage: Mature

Concentration Level: Low

Competition Level: Low

Revenue Volatiliity: High

Capital Intensity: High

Technology Change: Low

Regulation Level: Very High

Industry Assistance: Low

Barriers to Entry: Medium

Industry Globalization: High

Organic Chemicals Industry

Figure 19: Organic Chemicals Industry

Characteristics

Source: IBISWorld

Figure 18: Pesticide Industry Growth Rate

2015 - 2020

Source: IBISWorld

0%

1%

2%

3%

4%

5%

6%

2015 2016 2017 2018 2019 2020

9. UOIG 9

University of Oregon Investment Group

Demand for lithium is expected to grow at compound annual growth rate of

10.1% from 2011-2025 driven primarily by energy storage used in hybrid and

electric vehicles (Tru Group Inc.)

Management and Employee Relations

Pierre Brondeau – Chairman, President and CEO

Brondeau joined FMC on January 1st

, 2010, as President and Chief Executive

Officer. He holds a Ph.D. in Biochemical Engineering from INSA in Toulouse,

France, and also holds a master’s degree in Food Sciences from the University

of Montpellier, France. Before coming to FMC he was the President and COO

of Rohm and Haas, which was acquired by Dow Chemical in 2009. Mr.

Brondeau also serves on the Board of Directors of Tyco Electronics and

Marathon Oil Corporation, and is Chairman of the Board of the American

Chemistry Council.

Paul Graves – Vice President and CFO

Graves joined FMC on October 1st

, 2012, as Executive Vice President and Chief

Financial Officer. He earned a bachelor of arts in Accounting and Finance from

Nottingham Trent University in 1993. Before joining FMC Graves served as

managing director and partner in the Investment Banking Division of Goldman

Sachs Group in Hong Kong. He brings over 19 years of international banking

and accounting experience, with a specialized focus in chemicals and

agriculture.

Management Guidance

Historically, management has been reasonably accurate with their guidance.

Every quarter they provide revised low-end and high-end estimates on EPS,

sales, and other line items. They have beat EPS guidance by an average of 1.3%

over the past three years. However, in recent quarters they have missed the

average analyst estimates, but have only missed their low-end estimate once.

Portfolio Strategy

FMC is currently held in all three of our portfolios. The Tall Fir’s portfolio is

currently in-line in IME and overweight mid-cap. Svigal’s portfolio is currently

underweight in IME and overweight mid-cap. FMC currently represent 12.47 %

of the DADCO portfolio.

Recent News

“FMC Corporation Announces Lithium Carbonate and

Lithium Salts Price Increase”

November 4th

, 2014

FMC announced that effective December 1st

, 2014, it will increase global

pricing for all grades of lithium carbonate and lithium salts, including lithium

hydroxide, specialty salts and pharmaceutical carbonate by 10 percent. The

increases are necessary to offset the increasing operating and raw materials costs

at their Argentina processing facility.

Figure 21: FMC Headquarters

Source: 2015 Google Images

Figure 22: Mid-cap Allocation vs. Benchmark

Source: UOIG Spreads

23.90%

19.30%

20.81%

11.02%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Tall Firs Svigals'

Portfolio

Benchmark

10. UOIG 10

University of Oregon Investment Group

“FMC Corporation Executes Credit Agreements for $3.5

Billion”

October 14th

, 2014

FMC Corporation announced that it has executed $3.5 billion of unsecured

credit agreements with lenders to facilitate the agreement to acquire all the

outstanding equity of Cheminova A/S. The new credit agreements include a $2

billion term loan agreement that can be drawn to finance the acquisition. FMC

also amended and extended the term of its $1.5 billion revolving credit facility,

which now expires on October 10, 2019.

Catalysts

Upside

Better healthcare and greater access to pharmaceuticals in rapidly

developing economies will increase demand for FMC’s products

serving pharmaceutical end markets.

The acquisition of Cheminova will give FMC greater geographical

diversity, limiting the impact of unfavorable regional developments.

Hybrid electric vehicles (HEV’s) and other applications for portable

energy storage will increase demand for lithium.

Downside

Changes in the regulatory environment could impact FMC’s ability to

continue producing/selling certain products or could increase the cost

of doing so.

An increase in the costs of raw materials or energy, including natural

gas, could significantly affect FMC’s operating results and reduce

profitability.

The expiration of product patents will bring increased competition in

the agricultural chemical markets from generic suppliers of the same

pesticidal active ingredient.

Climate change.

Comparable Analysis

Comparable companies were screened and selected by comparing different

quantitative and qualitative metrics. Since companies within the diversified

chemical industry have highly unique and differentiated product mixes, selecting

good comparable companies was difficult. Qualitative metrics used focused on

finding companies with similar risk exposure, that serve similar end markets as

FMC, such as food ingredients, pharmaceuticals, and agricultural markets.

Companies were also evaluated based on the geographic regions they operate in

as well as the diversity of their product portfolio in comparison to FMC’s.

Quantitative metrics included finding companies comparable in size, with

similar growth rates, capital structures, and betas.

Ashland Inc. (ASH) – 30%

Ashland Inc. is a diversified chemical company that serves customers

worldwide. Ashland Inc. is divided into three segments: Ashland Specialty

Ingredients, Ashland Performance Materials, and Ashland Consumer markets.

Source: Google Images

Figure 25: Ashland Inc. Logo

Figure 23: One-year Stock Chart

Source: Yahoo Finance

One-Year Stock Chart

0

500000

1000000

1500000

2000000

2500000

3000000

3500000

4000000

$0.00

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

$80.00

$90.00

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14 Aug-14 Oct-14

Volume Adjusted Close 50-Day Avg 200-Day Avg

Figure 24: Comparable Analysis Multiples

Source: UOIG Spreads

Multiple Implied Price Weight

EV/Revenue 64.96 0.00%

EV/Gross Profit 85.43 0.00%

EV/EBIT 54.48 50.00%

EV/EBITDA 53.68 50.00%

EV/(EBITDA-Capex) 50.99 0.00%

Market Cap/Net Income = P/E 50.89 0.00%

Price Target $54.08

Current Price 56.50

Overvalued (4.28%)

11. UOIG 11

University of Oregon Investment Group

Ashland received the highest weighting because of its very similar EBITDA

growth rate, EBIT and EBITDA margins, market capitalization, and beta. In

addition, Ashland is exposed to many of the same market risks as FMC and has

a similar level of portfolio diversity.

Celanese Corporation (CE) – 25%

Celanese Corporation is a diversified chemical company that manufactures and

sells value-added chemicals and other chemical based products worldwide. The

company is divided into four segments: Advanced Engineered Materials,

Consumer Specialties, Industrial Specialties, and Acetyl Intermediaries. In

addition, the company also provides organic solvents and intermediates for

agricultural, pharmaceutical, and chemical products.

Celanese was deemed a good comparable company because it operates

internationally and produces a wide variety of chemicals and polymers used for

foods, beverages, and personal care products, thus sharing similar market risks

as FMC. It is also has a similar market capitalization and capital structure.

Eastman Chemical Co. (EMN) – 20%

Eastman Chemical Company is a diversified chemical company that

manufactures and sells specialty chemicals, fibers, and plastics. Eastman’s

products are divided into four segments: Additives & Functional Products,

Adhesives & Plasticizers, Advance Materials, Fibers, and Fluids &

Intermediaries.

Eastman was chosen as a comparable to FMC because it serves agricultural and

health end markets, and has similar EBIT and EBITDA margins. However,

Eastman received a slightly lower weighting because it has a much more

diversified product portfolio, higher market capitalization, and significantly

higher beta.

Rockwood Holdings (ROC) – 20%

Rockwood Holdings Inc. is a specialty chemical company that develops,

manufactures, and markets chemicals for industrial and commercial

applications. Rockwood Holdings Inc. is one of three key producers of basic

lithium compounds, which is used for glass and ceramics production,

performance greases, battery products, and pharmaceutical applications.

Although Rockwood holdings has significantly higher valuation multiples, It

was chosen as comparable company because it is one of FMC’s two direct

competitors in the lithium business and has a nearly identical capital structure.

Rockwood also has similar profitability margins as FMC, and a similar beta.

Monsanto Co. (MON) – 5%

Monsanto is a large-cap agricultural chemical company that operates in two

segments: Seed and Genomics, and Agricultural Productivity. The Agricultural

Productivity segment manufactures and sells herbicides for agricultural,

commercial, and industrial uses. Monsanto has operations in the United States,

Europe, Asia, Africa, Brazil, Mexico, and Argentina.

Figure 26: Celanese Logo

Source: Google Images

Source: Google Images

Figure 27: Eastman Chemical Co. Logo

Figure 28: Rockwood Holdings Logo

Source: Google Images

12. UOIG 12

University of Oregon Investment Group

Monsanto was added as a comparable because it is Agrochemical Company and

therefore shares many of the same risks as FMC, especially as FMC becomes

more of a pure play agricultural solutions company. However, due to the major

differences in size, capital structure, and growth, Monsanto only received a 5%

weighting.

Discounted Cash Flow Analysis

Revenue Model

Revenue growth was broken down into FMC’s three main business segments

and then was projected forward based on the key external drivers of each

segment and FMC’s strategic position to capitalize on those drivers. Revenue

growth is projected to peak in 2017 once all the revenues from Cheminova are

accretive, then gradually decline to 4.48% going into perpetuity.

FMC Agricultural Solutions

Agricultural Solutions is FMC’s biggest driver of revenue and was the most

challenging segment to predict because of the recent announcement that FMC

has agreed to acquire the Danish crop protection company Cheminova, which is

expected to close in early 2015.

The acquisition is expected to increase segment revenue from 55% of total

company revenue to 77% pro forma, with the majority of growth happening in

the first two years. Therefore, it was necessary to project out the revenues of

FMC’s other two business segments first, and then project Agricultural solutions

revenue through 2017 as a percentage of total company revenue.

From 2018-2022 revenue growth is expected to decrease slightly each year due

to a combination of external factors, such as the increased use of genetically

modified crops, increased regulation, and industry consolidation. However,

FMC’s unique focus on high-margin, technology-based solutions for niche crops

will allow them to outperform the industry by 300-500 basis points during those

years before dropping to 4% going into perpetuity.

FMC Health and Nutrition

Revenue growth in the FMC Health and Nutrition segment is projected decrease

to 6.00% in 2015 resulting from a slowdown in demand in China for MCC used

in high-end beverages. Even if economic growth in China remains stagnant,

FMC has positioned themselves nicely through their proactive portfolio

management to experience sustained revenue growth within this segment.

Demand in pharmaceutical end markets remains robust and is expected to

increase as rapidly developing economies gain more access to pharmaceuticals.

The number of FDA approvals for Omega-3 based products indicates growing

Omega-3 demand in the upcoming years, which FMC will be able to capitalize

on once they have more pharmaceutical customers and have developed the right

nutraceutical product.

With consumer spending expected to increase annually by 2.6% over the next

five years, and increasing global demand for beneficial supplements, effective

pharmaceuticals, and nutritious food ingredients, revenue growth in the non-

cyclical Health and Nutrition segment is projected to increase steadily from

2016-2022, before dropping to 5% in the terminal year.

Figure 29: Monsanto Logo

Source: Google Images

Figure 30: Segment Revenue (%) 2015 - 2023

Source: UOIG Spreads

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

FMC Agricultural Soultions FMC Health and Nutrition

FMC Minerals

Figure 31: Segment Revenue Growth 2014 -

2023

Source: UOIG Spreads

0%

5%

10%

15%

20%

25%

30%

2014E 2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

FMC Agricultural Solutions FMC Health and Nutrition

FMC Minerals

13. UOIG 13

University of Oregon Investment Group

FMC Minerals

FMC Minerals revenue is projected to increase from 8% in 2015 to 12.5% in

2020 as global demand for lithium continues to increase. After 2020, revenue

growth is projected to slightly decrease to 8% in the terminal year as new

producers enter the market and new technologies for energy storage emerge.

Discontinue Operations & Eliminations

FMC expects to sell their Alkali Chemicals division midway through 2015 to

leverage the acquisition of Cheminova. Thus, discontinued operations in 2015 is

projected as roughly half a year’s revenue for that segment.

Eliminations account for sales from one business segment to another. Due to

FMC’s more centralized organizational model, eliminations are not project in

the future.

Costs of Goods Sold (COGS)

COGS have remained at around 60% of total revenue over the past few years as

increased operational efficiencies in the FMC Minerals segment have been

offset by the high inflationary environment and impact of import restrictions in

Argentina. As management turns its focus towards achieving “Operational

Excellence” within the Health and Nutrition segment, and FMC capitalizes on

cost synergies and increased economies of scale from the acquisition of

Cheminova, COGS is likely to decrease. However, these cost reductions may be

partially offset by increasing energy costs and higher environmental compliance

costs due to increased regulation. Therefore, COGS is projected to decrease as a

percentage of revenue to 58.5% by 2017 and remain at that level going into

perpetuity.

Beta

FMC’s beta was determined by regressing the 3-year daily, 5-year daily, and-5

year monthly against the S&P 500. These regressions received weightings of

30%, 15%, and 20%, respectively. In addition, a 3 year HAMADA beta and a 3-

year Vasicek beta was used because of the major restructuring changes FMC has

gone through in the past three years.

Selling, General, and Administrative Expense

Selling, general and administrative expenses include sales and marketing costs,

accounting costs, fees associated with concluding acquisitions, and other

corporate expenses. SG&A expenses are projected to increase as a percentage of

revenue in 2015 and 2016 due to the transaction fees associated with the

Cheminova acquisition and the sale of their Alkali division, and then decrease

linearly as a percentage of revenue back to historical levels.

Depreciation and Amortization

Depreciation is provided on the straight-line basis over the estimated useful lives

of assets. Depreciation and Amortization was projected forward using the

percentage of Net PP&E Beginning. To account for the acquisition of

Cheminova, the approximate value of Cheminova’s net assets ($670 million)

was added to 2015 Net PP&E Beginning.

Research and Development

Figure 32: Beta Calculation

Source: UOIG Spreads

Beta SE Weighting

1-Year Daily 0.99 0.10 0.00%

3-Year Daily 1.20 0.03 30.00%

5-Year Daily 1.16 0.05 15.00%

3-Year Monthly 1.14 0.11 0.00%

5-Year Monthly 1.19 0.07 20.00%

3-Year Hamada 1.33 N/A 20.00%

3-Year Vasicek 1.20 0.05 15.00%

FMC Corp Beta 1.22

Figure 34: Long-lived Assets by Region - 2013

Source: FMC 10-K

43%

8%

15%

34%

North America

Latin America

Asia Pacific

EMEA

Figure 33: Beta Sensitivity Table

Source: UOIG Spreads

ImpliedPrice Undervalued/(Overvalued)

Terminal Growth Rate Terminal Growth Rate

55 2.0% 2.5% 3.0% 3.5% 4.0%

1.02 61.72 65.94 71.05 77.36 85.34

1.12 55.14 58.54 62.59 67.49 73.55

1.22 49.51 52.28 55.53 59.41 64.11

1.32 44.63 46.91 49.55 52.67 56.39

1.42 40.37 42.26 44.43 46.97 49.95

AdjustedBeta

14. UOIG 14

University of Oregon Investment Group

The Agricultural Solutions segment currently accounts for 85% of FMC’s total

R&D costs. Since FMC is transitioning into more of pure play agricultural

solutions company, and the industry has an increasing reliance on new

technologies and product innovation, R&D costs are projected to increase as a

percentage of revenue.

Restructuring and Other Charges

Restructuring and other charges consist of costs associated with restructuring

portions of FMC’s business such as severance benefits, and environmental

charges associated with environmental remediation at continuing operating sites.

Restructuring charges are very difficult to predict, but environmental charges are

likely to be recurring for chemical companies and may even increase. Thus,

restructuring and other charges were projected to remain in line with historical

levels, and decrease as a percentage of revenue.

Acquisitions

FMC complements its organic growth strategy with targeted acquisitions of new

products and technologies that add to their diverse portfolio. Since increasing

technological innovation and industry consolidation are two major themes of the

pesticide industry, it is likely that acquisitions will continue to be a major part of

FMC’s external growth strategy. Thus, acquisitions are projected to increase

each year, but remain steady as a percentage of revenue.

Capital Expenditures

Capital expenditures in 2014 have been significantly higher than historical levels

due to capital expansion projects in FMC Health and Nutrition and FMC

Minerals. Going forward capital expenditures are projected to increase year over

year, while marginally decreasing as a percentage of revenue.

Tax Rate

FMC’s historical effective tax rate has been roughly 25.5%. Starting in 2014,

Denmark’s corporate tax rate will decrease one percentage point per year

through 2016 when it will stop at 22%. It is likely that FMC will funnel income

through this subsidiary to achieve a lower effective tax rate. Thus, FMC’s tax

rate is projected to decrease linearly from 25.5% to 23.2% by 2020.

Recommendation

At current price of $56.50, valuation multiples suggest that FMC is currently

trading at a premium in comparison to its competitors. FMC has transitioned its

focus to the agrochemical industry, which is likely to be negatively impacted by

increased competition, stricter regulations, rising energy costs, and unfavorable

climatic conditions. Thus, I recommend a sell for all three equity portfolios.

Valuation Method Implied Price Weighting

Discounted Cash Flows Analysis 55.48 60%

Comparable Analysis 54.08 40%

Final Implied Price $54.92

Current Price 56.50

Overvalued (2.79%)

Final Price Target

$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2015E 2016E 2017E 2018E 2019E 2020E 2021E 2022E 2023E

R&D Capital Expenditures

Figure 35: Research and Development vs.

Capital Expenditures 2015 - 2023

Source: UOIG Spreads

Figure 36: Tax Rate Sensitivity Table

Source: UOIG Spreads

ImpliedPrice Undervalued/(Overvalued)

Terminal Growth Rate Terminal Growth Rate

55 2.0% 2.5% 3.0% 3.5% 4.0%

19.20% 49.12 51.85 55.05 58.86 63.48

21.20% 49.30 52.04 55.27 59.11 63.77

23.20% 49.47 52.24 55.48 59.36 64.06

25.20% 49.65 52.43 55.70 59.61 64.34

27.20% 49.83 52.63 55.92 59.86 64.64

TaxRate