Alkyl Amine: The Making of a Multibagger

•Download as PPTX, PDF•

0 likes•216 views

The document discusses how specialty chemicals company Sadhan has outperformed the market. It summarizes Sadhan's business model, financial performance, and valuation. Sadhan started in 1979 and now generates around 70% of its revenue from pharmaceutical and agrochemical products. It has consistently grown sales by 17% annually and earnings. The market has highly valued Sadhan due to its growth trajectory, with its price-earnings ratio expanding in recent years. However, further rerating of the PE ratio is unlikely, so future outperformance will depend on continuing strong earnings growth.

Recommended

More Related Content

Similar to Alkyl Amine: The Making of a Multibagger

Similar to Alkyl Amine: The Making of a Multibagger (20)

Recently uploaded

Recently uploaded (20)

Alkyl Amine: The Making of a Multibagger

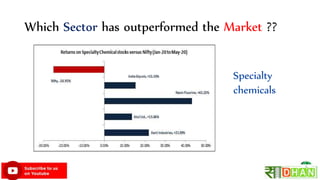

- 1. Which Sector has outperformed the Market ?? Specialty chemicals

- 2. • China Factor (Stringent environment norms, Clear Sky Policy, Covid 19) • Global opportunity (Export potential due to low cost labor) • Domestic Opportunity ( Import substitution, Atmnirbhar Bharat, Make In India, Anti Dumping Duty) • Shift from Unorganized to Organized helping Listed players How Specialty Chemicals have outperformed the Market ?? Sadhan

- 3. • China Factor (Stringent environment norms, Clear Sky Policy, Covid 19) How Specialty Chemicals have outperformed the Market ?? Sadhan

- 4. How Specialty Chemicals have outperformed the Market ?? Sadhan

- 5. Sadhan

- 7. • Started in 1979 with Aliphatic Amine in technical collaboration with a US firm. • Later on, they started making Derivatives • Then they started making Specialty Chemicals Aliphatic Amine 50% Derivative 25% Speciality Chemicals 25% History Sadhan

- 8. • Managing Director is Yogesh Kothari • Chemical Engineer from U.D.C.T., Mumbai, • Master of Management Science and Master of Science (Chemical Engineering) from University of Massachusetts, U.S.A. Management Sadhan

- 9. Management • Managing Director is Yogesh Kothari • Chemical Engineer from U.D.C.T., Mumbai, • Master of Management Science and Master of Science (Chemical Engineering) from University of Massachusetts, U.S.A. • Promoters own 74% of shareholding • No share pledge Sadhan

- 10. Business Model Raw material Methanol Ammonia Denatured Ethyl Alcohol Imported from Saudi Arabia, Oman, Qatar etc, especially post the US sanctions on Iran, which is one of the major manufacturers of methanol in the world. Methanol price are linked to crude prices Difficult to transport, it is largely sourced indigenously. Mainly sourced from sugar factories and distilleries besides being imported from the US and Latin American countries. Sadhan

- 11. Business Model Revenue Mix Pharma + Agro =~70% Sadhan

- 12. Product Aliphatic Amine Methyl Amine Ethyl Amine Indian market size:85,000 ton AACL have 30,000 ton capacity (40% market Share). Others are Balaji & RCF AACL is furtherenhancing capacity by 15,000 ton over next 2 years Methyl amine is dangerous & difficult to carry so Indian demand is captive Margin are low Sadhan

- 13. Product Aliphatic Amine Ethyl Amine Indian market size:21,000 ton AACL is market leader with 15,000 ton capacity. Others is Balaji Ethyl amine is dangerous & difficult to transport so Indian demand is mostly captive with limited 10-15% import Sadhan

- 14. Product Derivative DMA HCL AACL have 12,000 ton capacity. AACL+ Balaji controls 60-70% market. Competitive market Not dangerous & easy to carry Used in Ranitidine which is used in treatment of Peptic & Gastric ulcer Used in Metformin which is used in Type 2 Diabetes treatment Sadhan

- 15. Product Specialty Chemical Acetonitrile Indian market size:17,000 ton AACL is market leader with 10,000 ton capacity (40% Market share) 2 methods to make Acetonitrile : (1) From Acrylonitrile (Auto industry ) (2) From Ascetic Acid+ Ammonia (AACL) The increased pharma demand has widened margins for the product. Prices have increased by 3X due to shortage of supply Export market and increase in domestic demand would be met by the expanded capacity of 15,000 ton Sadhan

- 16. 236 288 366 446 476 484 501 616 846 993 972 Growth Rate:17% Sales Sadhan

- 17. 13% 15% 16% 19% 18% 19% 19% 19% 19% 26% 28% EBITDA Margin (%) Sadhan

- 19. 24 36 22 46 61 101 63 102 144 188 1 2 3 4 5 6 7 8 9 10 Cash flow from Operation (CFO) Sadhan

- 20. 0.78 0.84 0.39 0.54 0.70 1.11 0.67 0.87 0.88 0.73 1 2 3 4 5 6 7 8 9 10 CFO EBITDA 0.80 Is Profit generated is real i.e. Cash? Sadhan

- 21. 2012 2013 2014 2015 2016 2017 2018 2019 2020 1.Net Fixed Asset Turnover 2.6 2.9 3.2 3.1 2.9 2.5 2.1 2.3 2.5 2.Receivables days 68 68 68 72 71 68 65 60 58 3.Inventory Turnover 6 6 6 6 7 6 6 9 10 High is better Low is better High is better Cash Conversion Sadhan

- 22. 12.2% 16.9% 19.3% 26.4% 24.9% 25.9% 22.4% 21.7% 27.3% 43.3% 1 2 3 4 5 6 7 8 9 10 Return on Capital Employed 15% Sadhan

- 23. - 50 100 150 200 250 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Profit (in Rs cr) Valuation Stock price Sadhan

- 24. Growth Rate 10Yr 7Yr 5Yr 3Yr TTM Sales Growth 17% 15% 16% 26% -2% OPM 20% 20% 21% 21% 28% PAT Growth 40% 37% 37% 62% 8% Avg. PE 12.1 13.5 16.0 17.2 29.2 ROCE 24% 27% 26% 28% ROCE+ PAT Growth 64% 64% 63% 91% PE Rerating Increasing Consistently Growing Consistently Growing Consistently Growing Why Market have valued AACL so high? Sadhan

- 25. Why Market have valued AACL so high? • Growth Stock • PE Expansion (Rerating) due to moving to next orbit (Rs 100 cr + Club) Sadhan

- 26. Will it sustain? • Next PE Rerating seems unlikely • Earning growth will lead to price growth, so watching the earning growth quarterly is recommended • There is huge sectoral tailwind supporting the buoyant price of its key product (Acetonitrile price is key monitorable) • Institution holding (MF ) is still low at 2%, there is room for institution to increase holding (Aarti Industries , Atul Ltd had similar trajectory ) Sadhan

- 27. What you should do? • Stock is fairly valued • Stock have great potential so people with conviction in Specialty Chemical growth story should invest • Invest at Right time, Right price • Accumulate at drop Sadhan