Tax benefits

•Download as PPTX, PDF•

0 likes•270 views

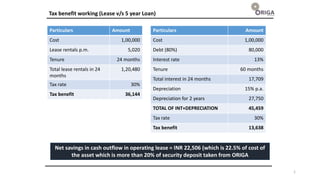

This document compares the tax benefits of leasing an asset versus taking out a loan to purchase the asset over 2 years and 5 years. Over 2 years, leasing the asset results in a tax benefit of INR 36,144 compared to INR 11,710 for a loan, a savings of INR 24,434. Over 5 years, leasing results in a tax benefit of INR 36,144 compared to INR 13,638 for a loan, a savings of INR 22,506. In both cases, leasing provides greater tax savings than taking out a loan to purchase the asset.

Report

Share

Report

Share

Recommended

Recommended

More Related Content

Similar to Tax benefits

Similar to Tax benefits (20)

1. Prepare and analize the common statement for An.pdf

1. Prepare and analize the common statement for An.pdf

Fiscal Year Ended March 2020 (FY2019) Financial Highlights

Fiscal Year Ended March 2020 (FY2019) Financial Highlights

First Quarter of Fiscal Year Ending March 2019(FY2018) Financial Highlights

First Quarter of Fiscal Year Ending March 2019(FY2018) Financial Highlights

MICROSOFT CORPORATIONFinancialStatementFY20Q1BALANCE SHEETS.docx

MICROSOFT CORPORATIONFinancialStatementFY20Q1BALANCE SHEETS.docx

MICROSOFT CORPORATIONFinancialStatementFY20Q1BALANCE SHEETS.docx

MICROSOFT CORPORATIONFinancialStatementFY20Q1BALANCE SHEETS.docx

Implications of the summer budget 2015 for PE houses

Implications of the summer budget 2015 for PE houses

Recently uploaded

VVVIP Call Girls In Greater Kailash ➡️ Delhi ➡️ 9999965857 🚀 No Advance 24HRS Live

Booking Contact Details :-

WhatsApp Chat :- [+91-9999965857 ]

The Best Call Girls Delhi At Your Service

Russian Call Girls Delhi Doing anything intimate with can be a wonderful way to unwind from life's stresses, while having some fun. These girls specialize in providing sexual pleasure that will satisfy your fetishes; from tease and seduce their clients to keeping it all confidential - these services are also available both install and outcall, making them great additions for parties or business events alike. Their expert sex skills include deep penetration, oral sex, cum eating and cum eating - always respecting your wishes as part of the experience

(07-May-2024(PSS)VVVIP Call Girls In Greater Kailash ➡️ Delhi ➡️ 9999965857 🚀 No Advance 24HRS...

VVVIP Call Girls In Greater Kailash ➡️ Delhi ➡️ 9999965857 🚀 No Advance 24HRS...Call Girls In Delhi Whatsup 9873940964 Enjoy Unlimited Pleasure

Recently uploaded (20)

Call Girls Jp Nagar Just Call 👗 7737669865 👗 Top Class Call Girl Service Bang...

Call Girls Jp Nagar Just Call 👗 7737669865 👗 Top Class Call Girl Service Bang...

FULL ENJOY Call Girls In Mahipalpur Delhi Contact Us 8377877756

FULL ENJOY Call Girls In Mahipalpur Delhi Contact Us 8377877756

👉Chandigarh Call Girls 👉9878799926👉Just Call👉Chandigarh Call Girl In Chandiga...

👉Chandigarh Call Girls 👉9878799926👉Just Call👉Chandigarh Call Girl In Chandiga...

Call Girls Service In Old Town Dubai ((0551707352)) Old Town Dubai Call Girl ...

Call Girls Service In Old Town Dubai ((0551707352)) Old Town Dubai Call Girl ...

Uneak White's Personal Brand Exploration Presentation

Uneak White's Personal Brand Exploration Presentation

Mysore Call Girls 8617370543 WhatsApp Number 24x7 Best Services

Mysore Call Girls 8617370543 WhatsApp Number 24x7 Best Services

Call Now ☎️🔝 9332606886🔝 Call Girls ❤ Service In Bhilwara Female Escorts Serv...

Call Now ☎️🔝 9332606886🔝 Call Girls ❤ Service In Bhilwara Female Escorts Serv...

Eluru Call Girls Service ☎ ️93326-06886 ❤️🔥 Enjoy 24/7 Escort Service

Eluru Call Girls Service ☎ ️93326-06886 ❤️🔥 Enjoy 24/7 Escort Service

Insurers' journeys to build a mastery in the IoT usage

Insurers' journeys to build a mastery in the IoT usage

Chandigarh Escorts Service 📞8868886958📞 Just📲 Call Nihal Chandigarh Call Girl...

Chandigarh Escorts Service 📞8868886958📞 Just📲 Call Nihal Chandigarh Call Girl...

Enhancing and Restoring Safety & Quality Cultures - Dave Litwiller - May 2024...

Enhancing and Restoring Safety & Quality Cultures - Dave Litwiller - May 2024...

Russian Call Girls In Gurgaon ❤️8448577510 ⊹Best Escorts Service In 24/7 Delh...

Russian Call Girls In Gurgaon ❤️8448577510 ⊹Best Escorts Service In 24/7 Delh...

Call Girls Kengeri Satellite Town Just Call 👗 7737669865 👗 Top Class Call Gir...

Call Girls Kengeri Satellite Town Just Call 👗 7737669865 👗 Top Class Call Gir...

MONA 98765-12871 CALL GIRLS IN LUDHIANA LUDHIANA CALL GIRL

MONA 98765-12871 CALL GIRLS IN LUDHIANA LUDHIANA CALL GIRL

VVVIP Call Girls In Greater Kailash ➡️ Delhi ➡️ 9999965857 🚀 No Advance 24HRS...

VVVIP Call Girls In Greater Kailash ➡️ Delhi ➡️ 9999965857 🚀 No Advance 24HRS...

Tax benefits

- 1. Tax benefit working (Lease v/s 5 year Loan) Particulars Amount Cost 1,00,000 Lease rentals p.m. 5,020 Tenure 24 months Total lease rentals in 24 months 1,20,480 Tax rate 30% Tax benefit 36,144 Particulars Amount Cost 1,00,000 Debt (80%) 80,000 Interest rate 13% Tenure 60 months Total interest in 24 months 17,709 Depreciation 15% p.a. Depreciation for 2 years 27,750 TOTAL OF INT+DEPRECIATION 45,459 Tax rate 30% Tax benefit 13,638 Net savings in cash outflow in operating lease = INR 22,506 (which is 22.5% of cost of the asset which is more than 20% of security deposit taken from ORIGA 1

- 2. Tax benefit working (Lease v/s 2 year Loan) Particulars Amount Cost 1,00,000 Lease rentals p.m. 5,020 Tenure 24 months Total lease rentals in 24 months 1,20,480 Tax rate 30% Tax benefit 36,144 Particulars Amount Cost 1,00,000 Debt (80%) 80,000 Interest rate 13% Tenure 24 months Total interest in 24 months 11,280 Depreciation 15% p.a. Depreciation for 2 years 27,750 TOTAL OF INT+DEPRECIATION 39,030 Tax rate 30% Tax benefit 11,710 Net savings in cash outflow in operating lease = INR 24,434 (which is 24.4% of cost of the asset which is more than 20% of security deposit taken from ORIGA 2