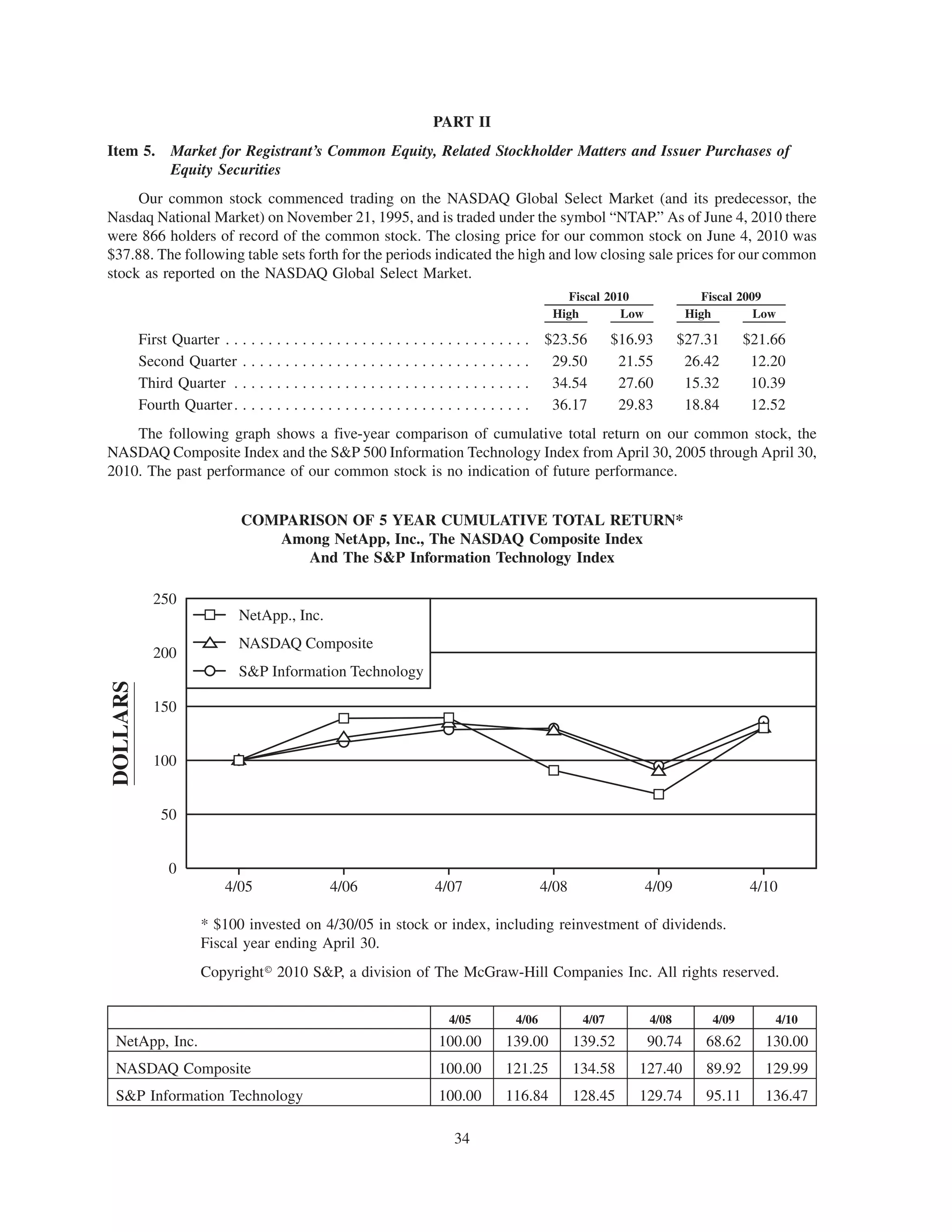

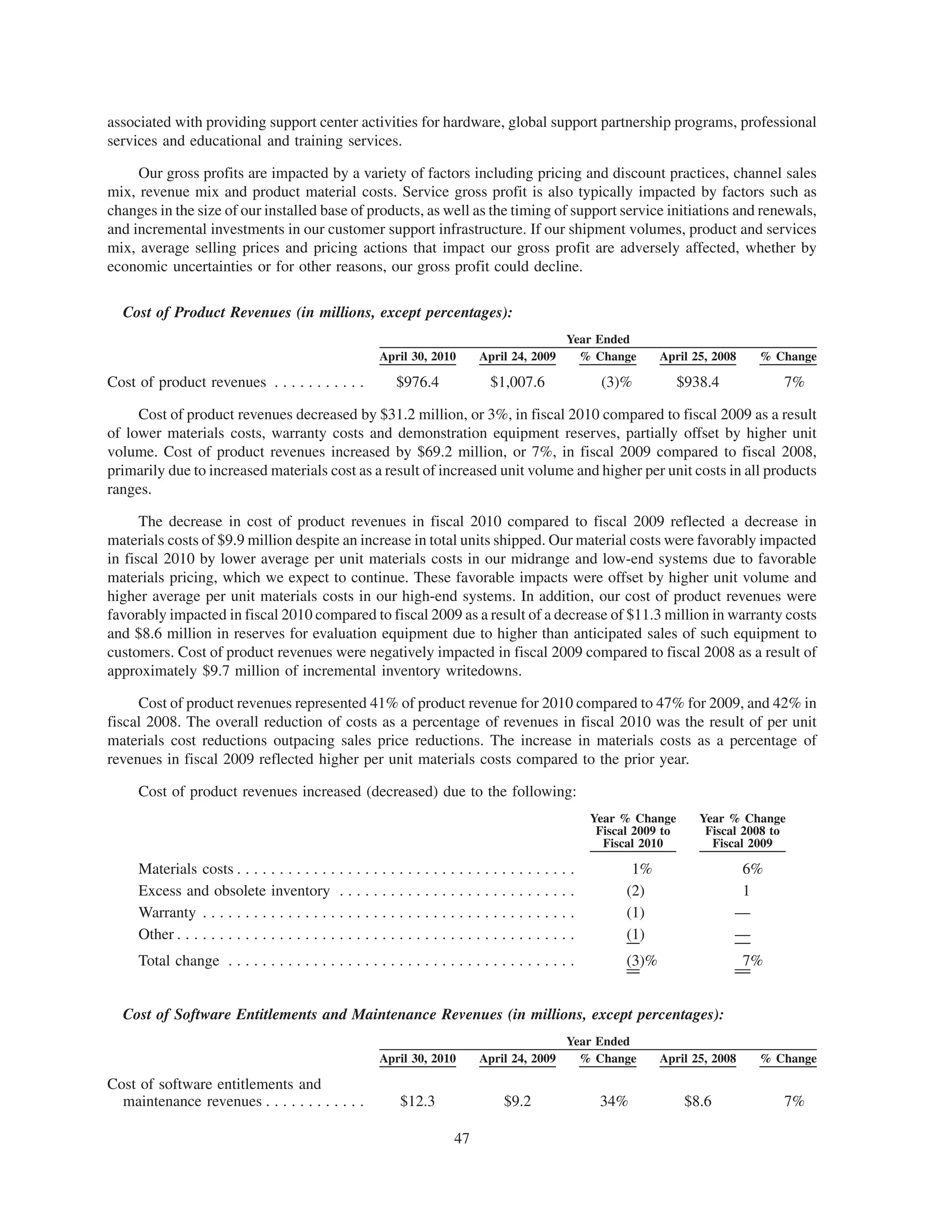

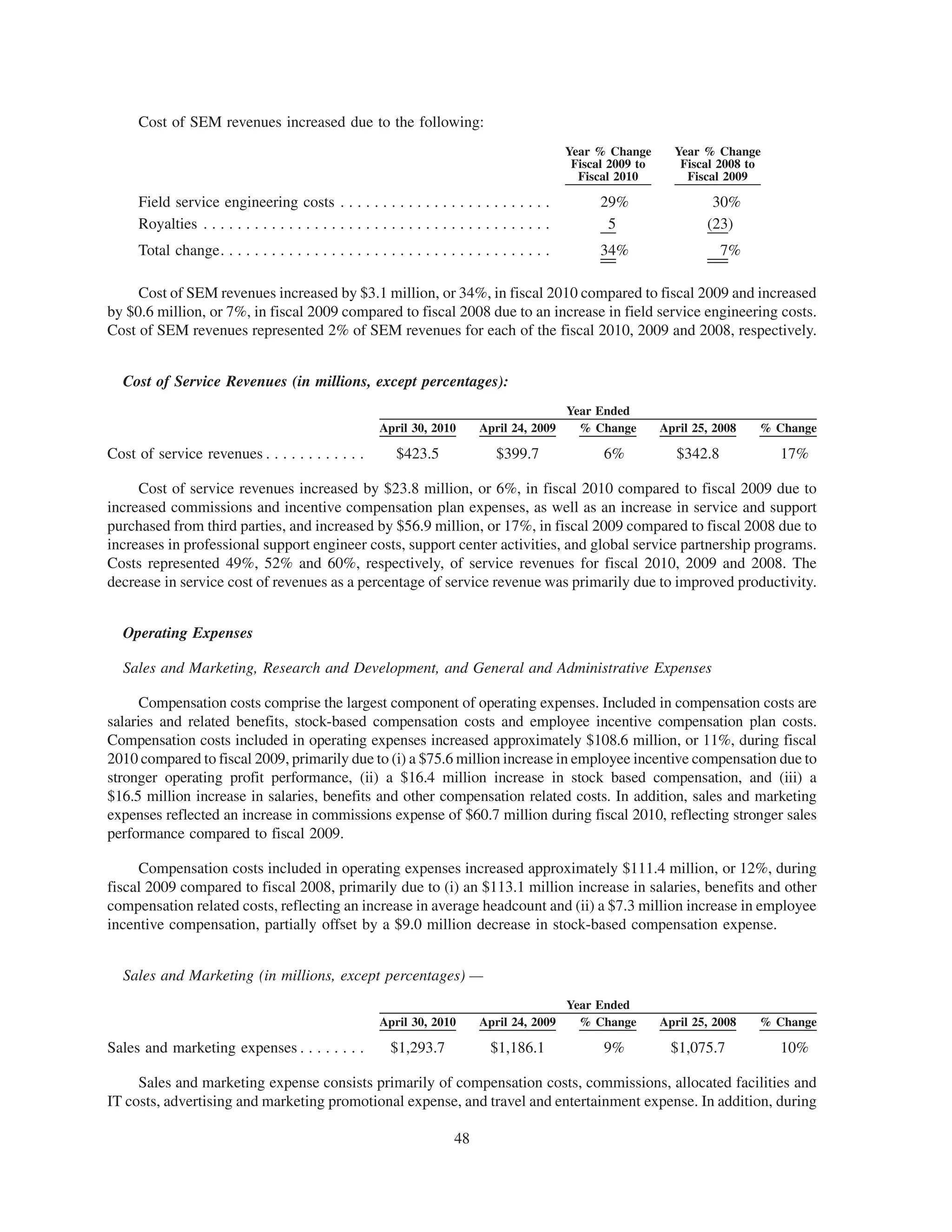

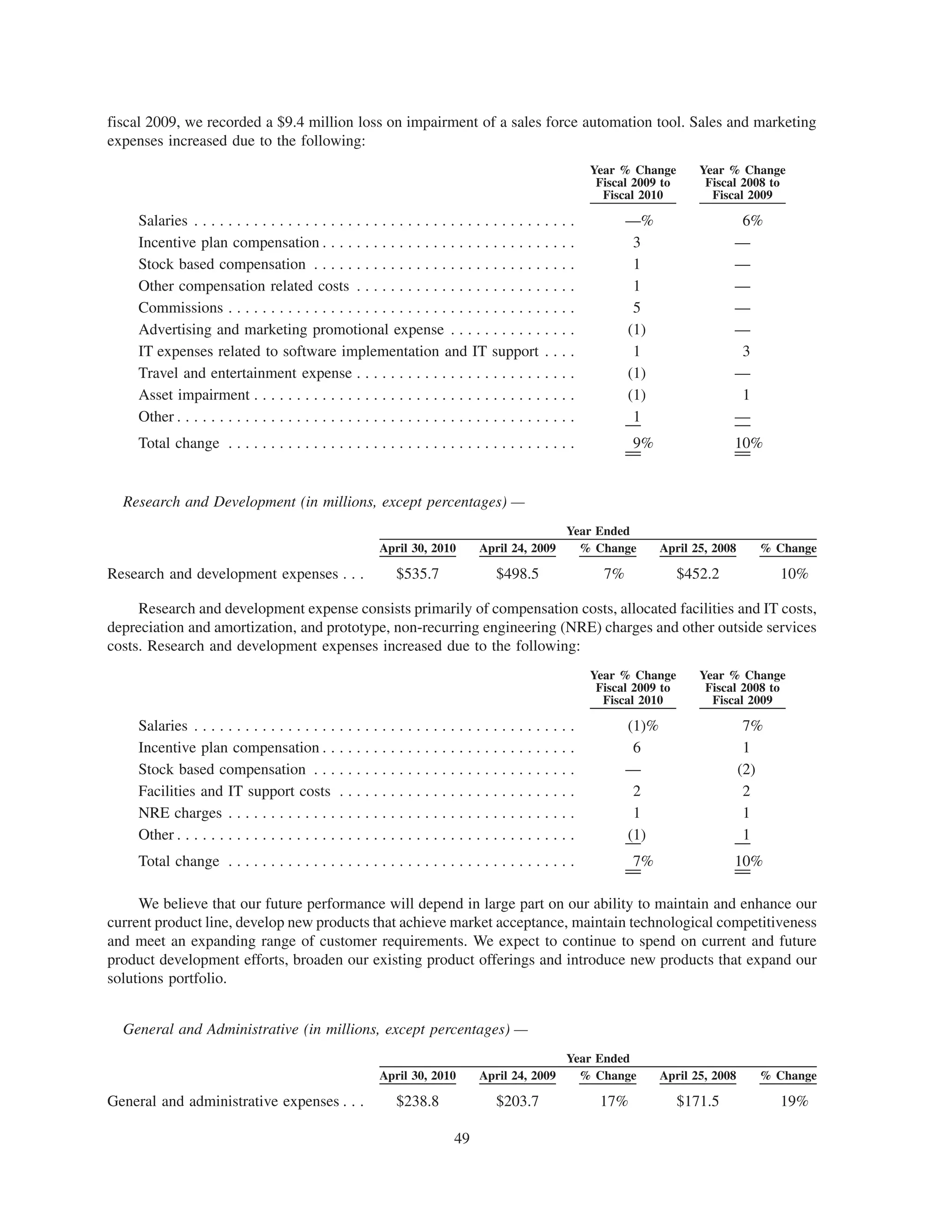

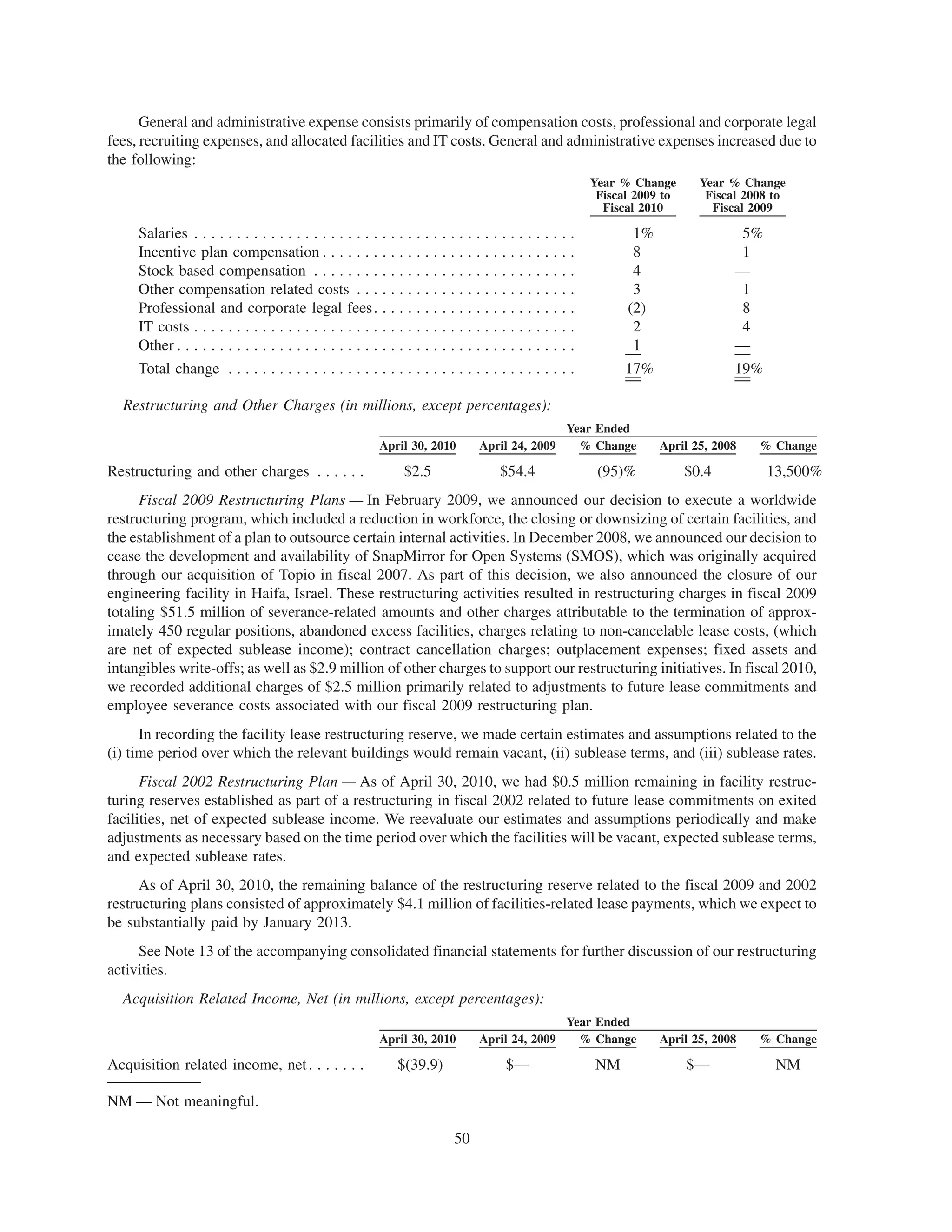

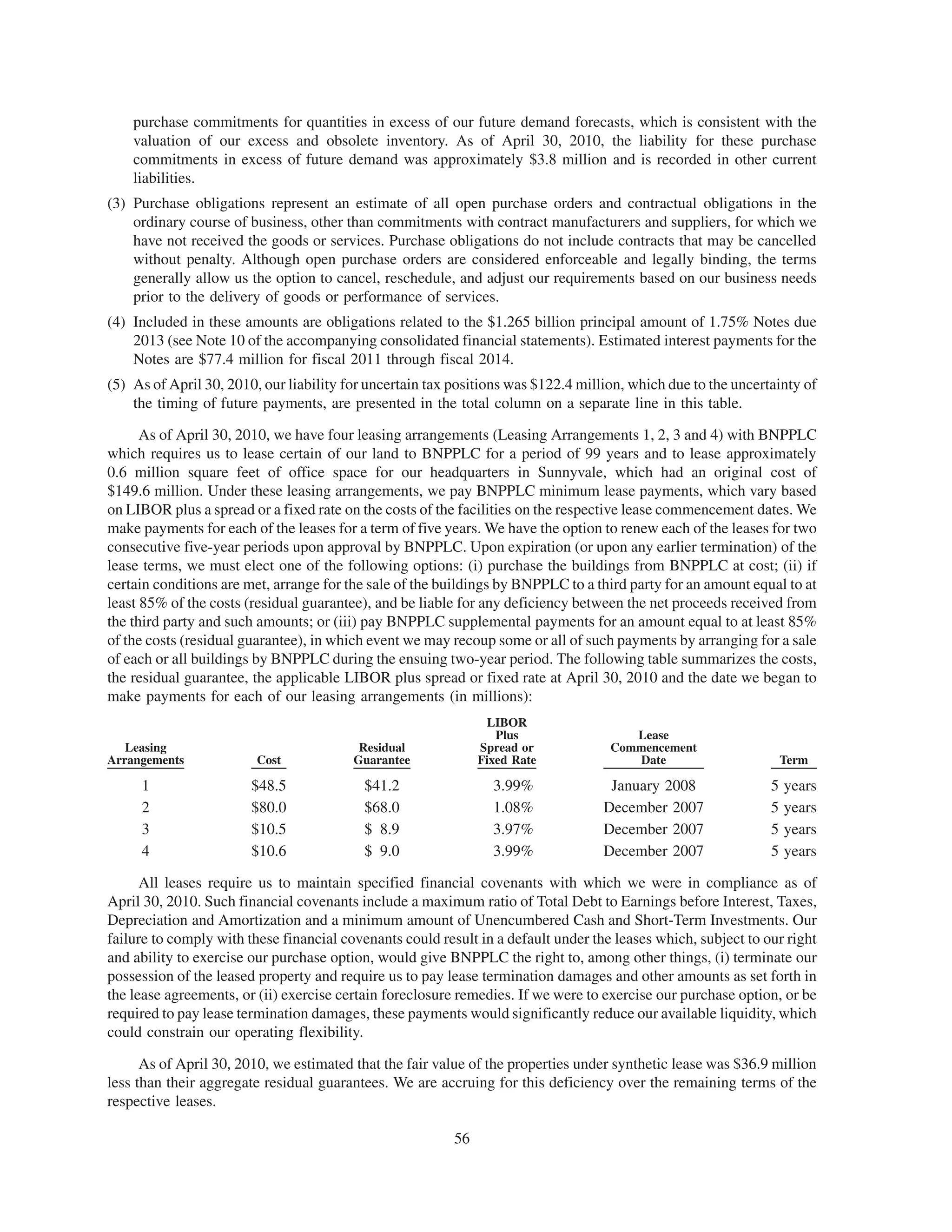

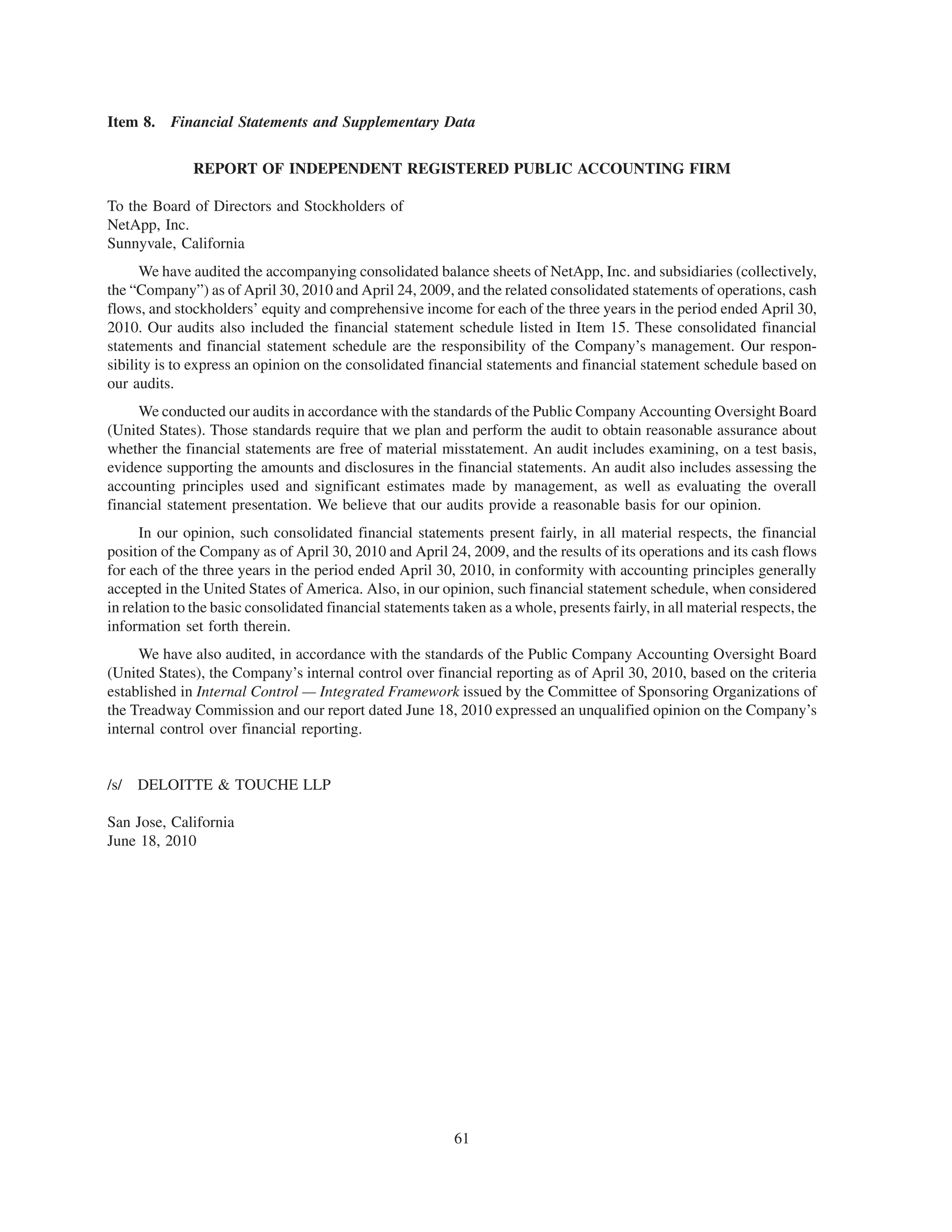

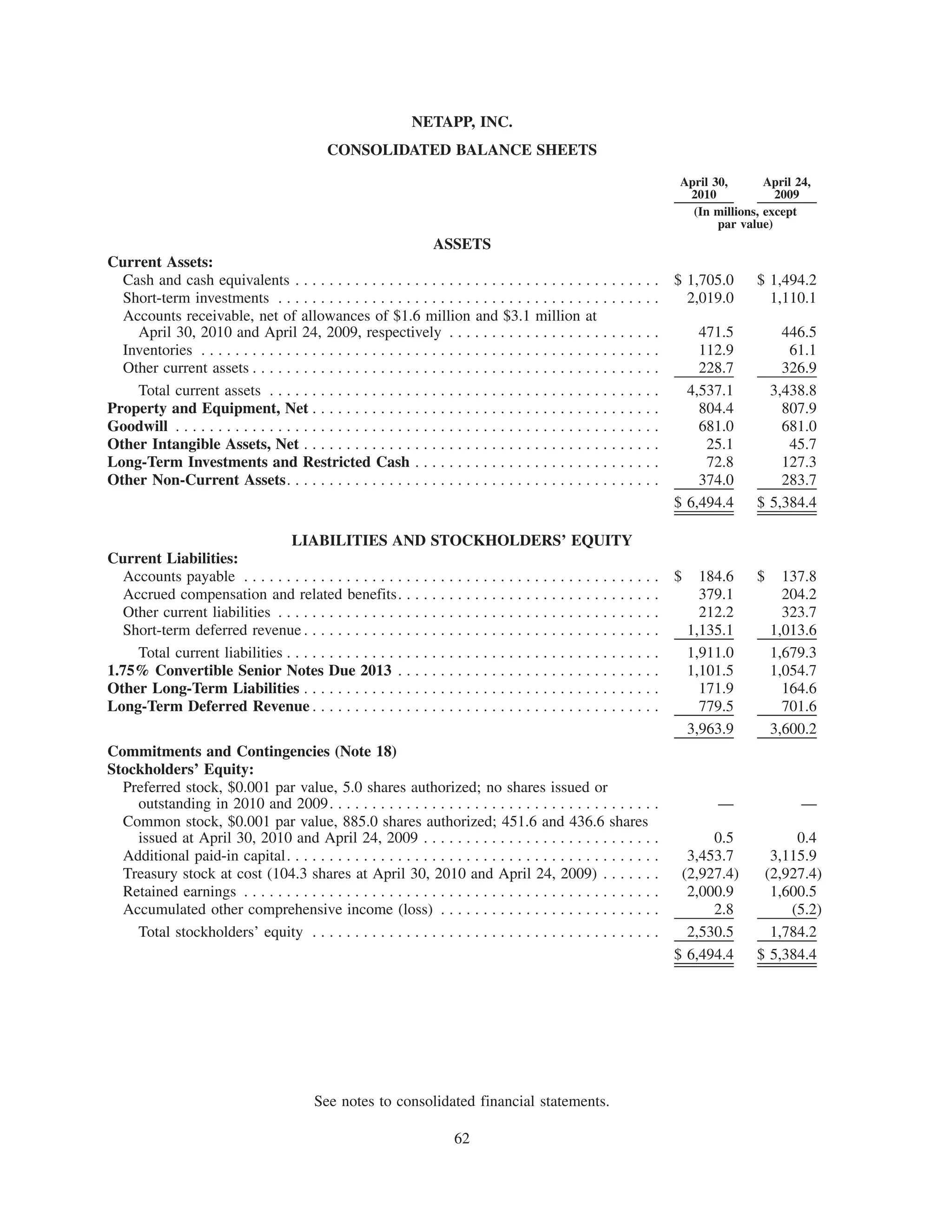

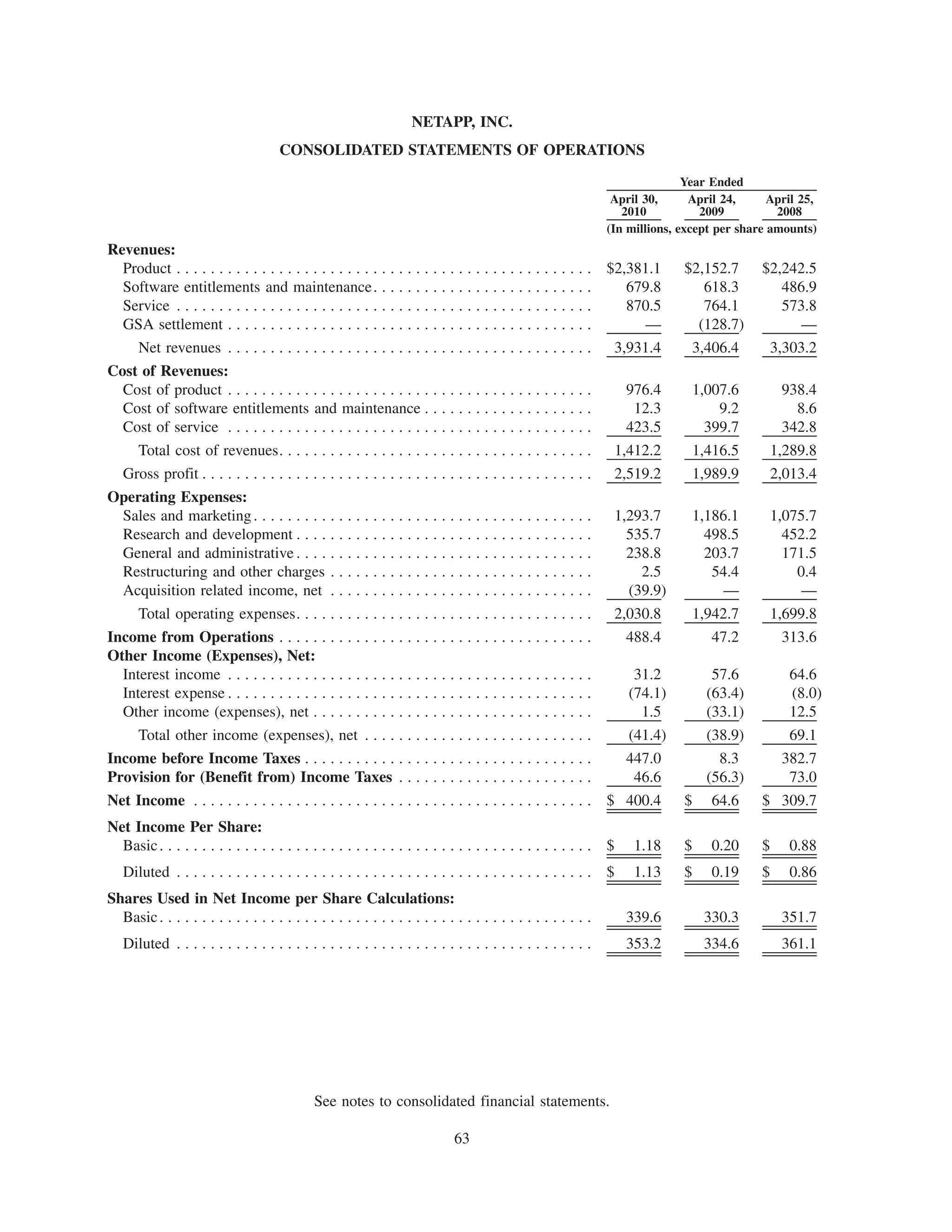

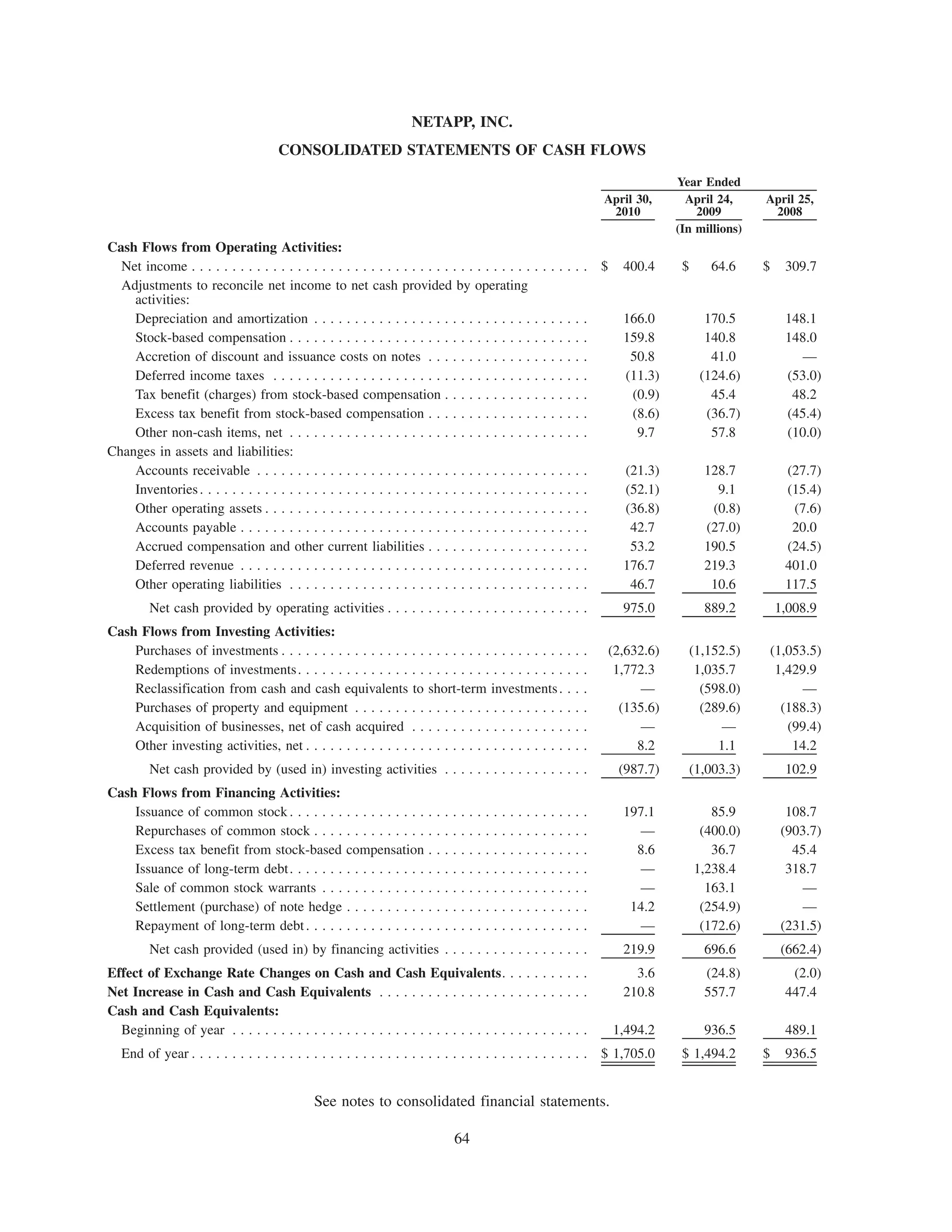

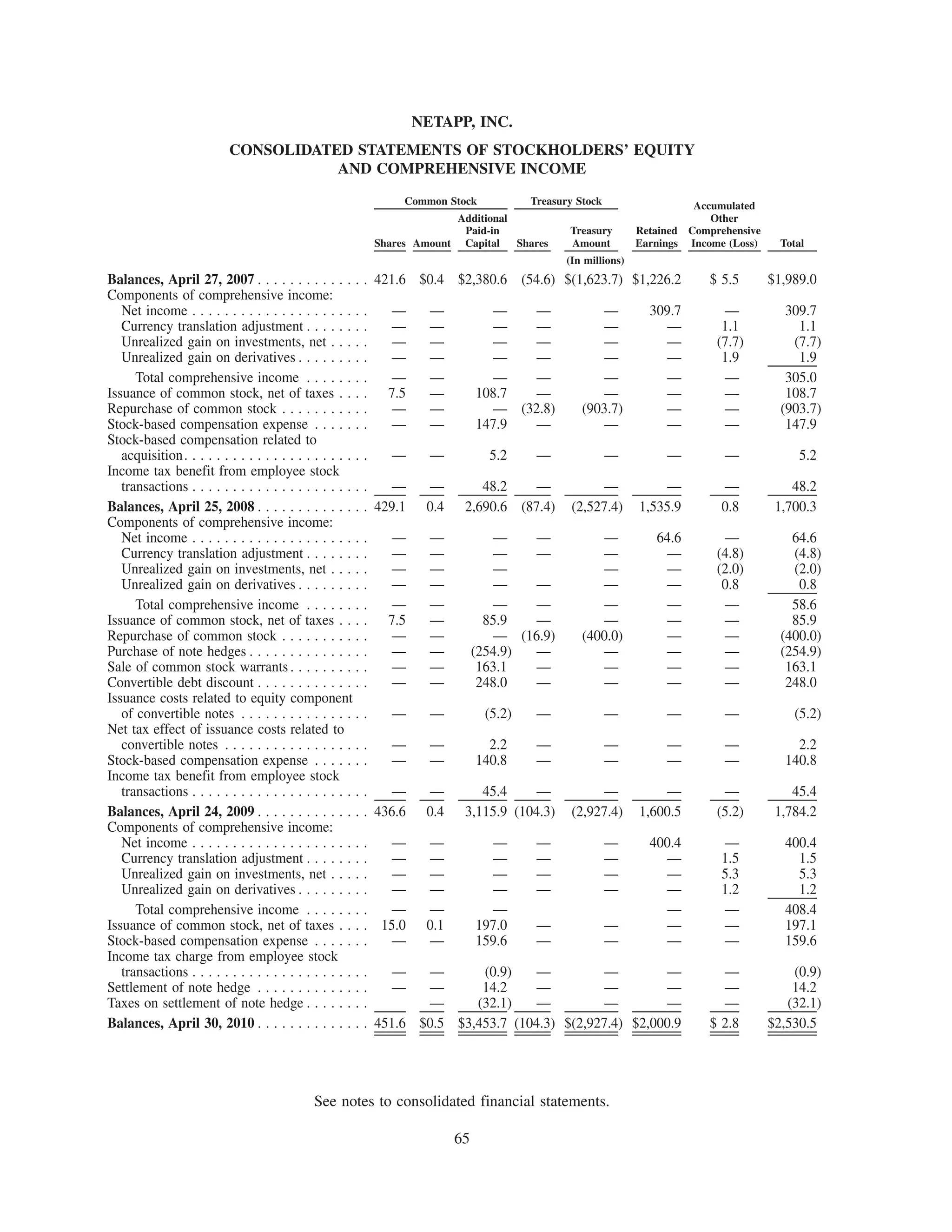

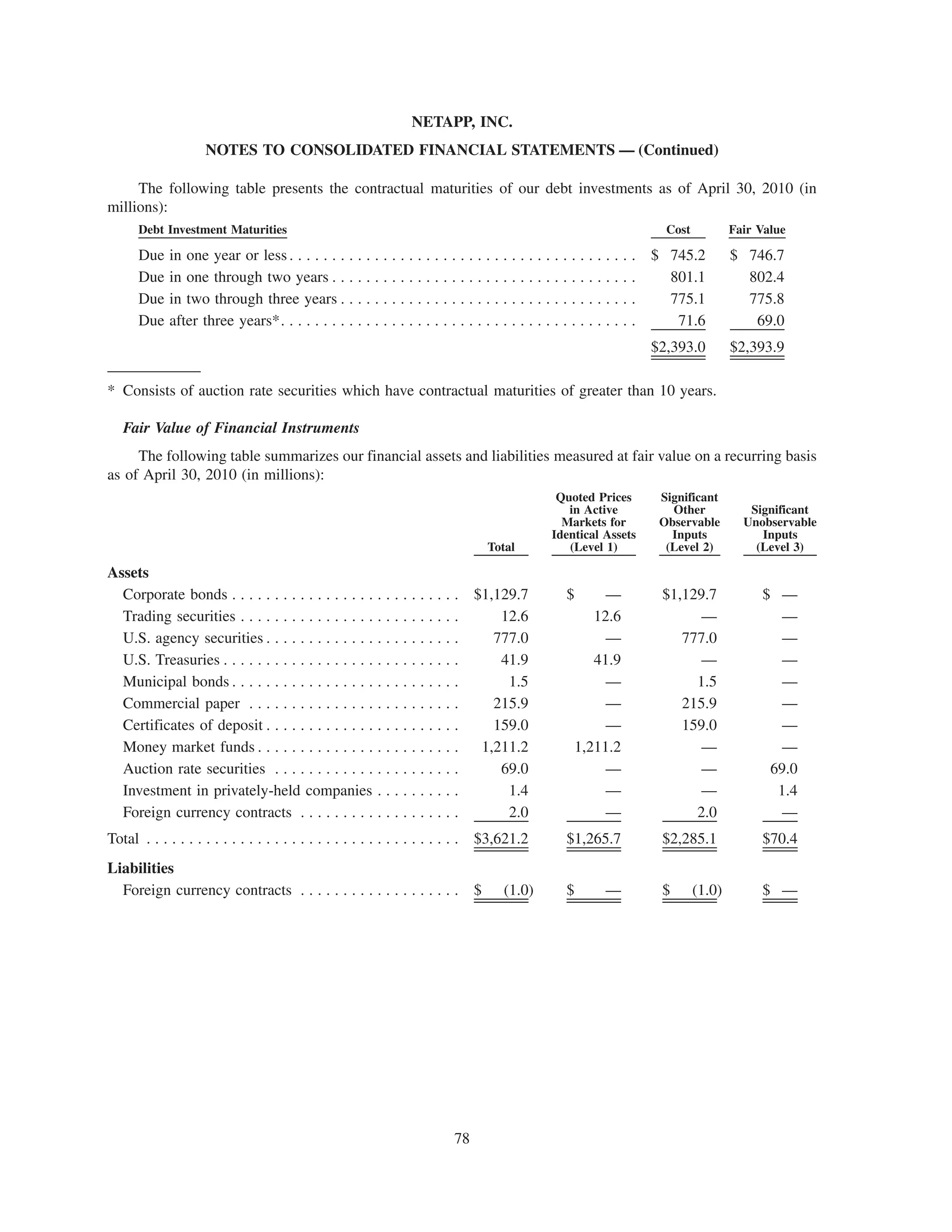

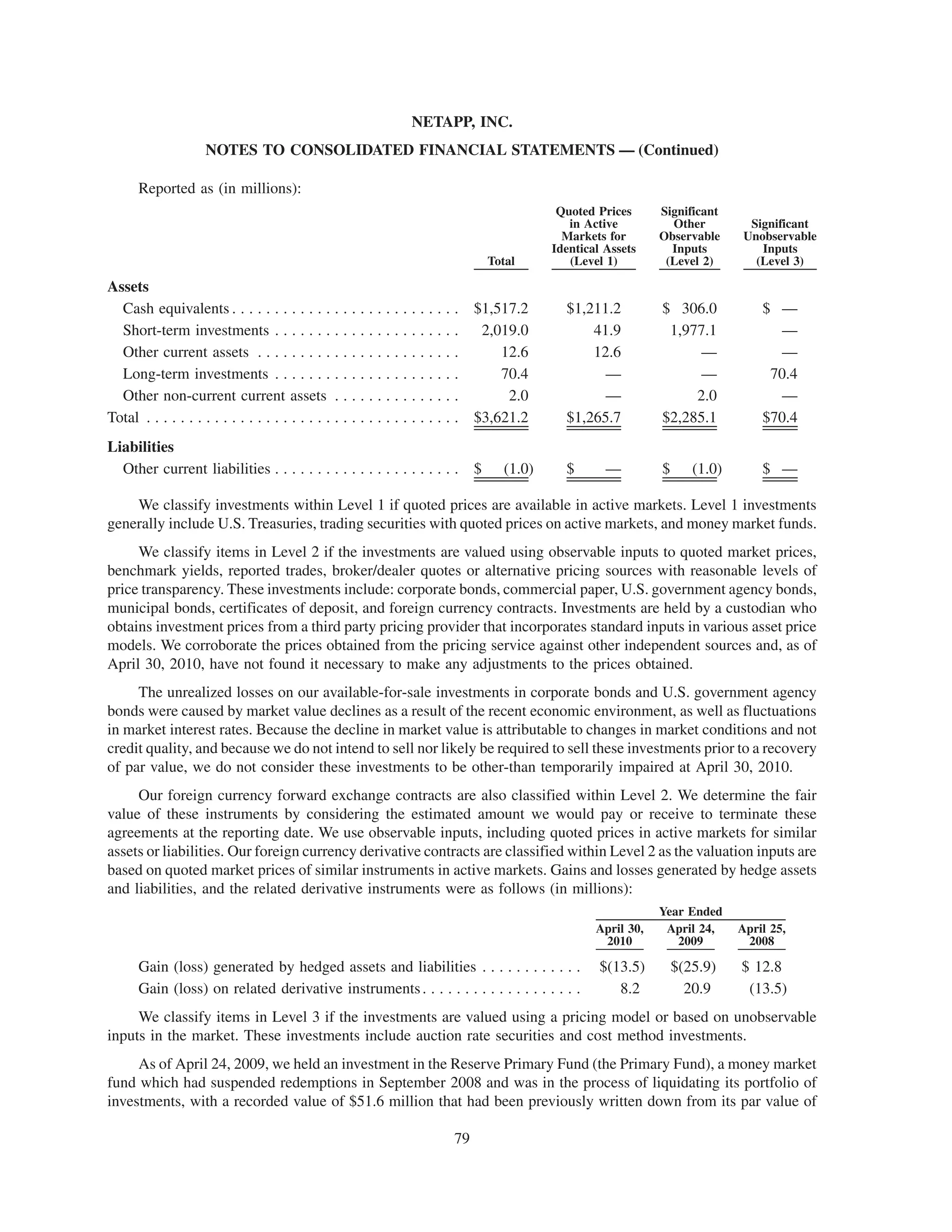

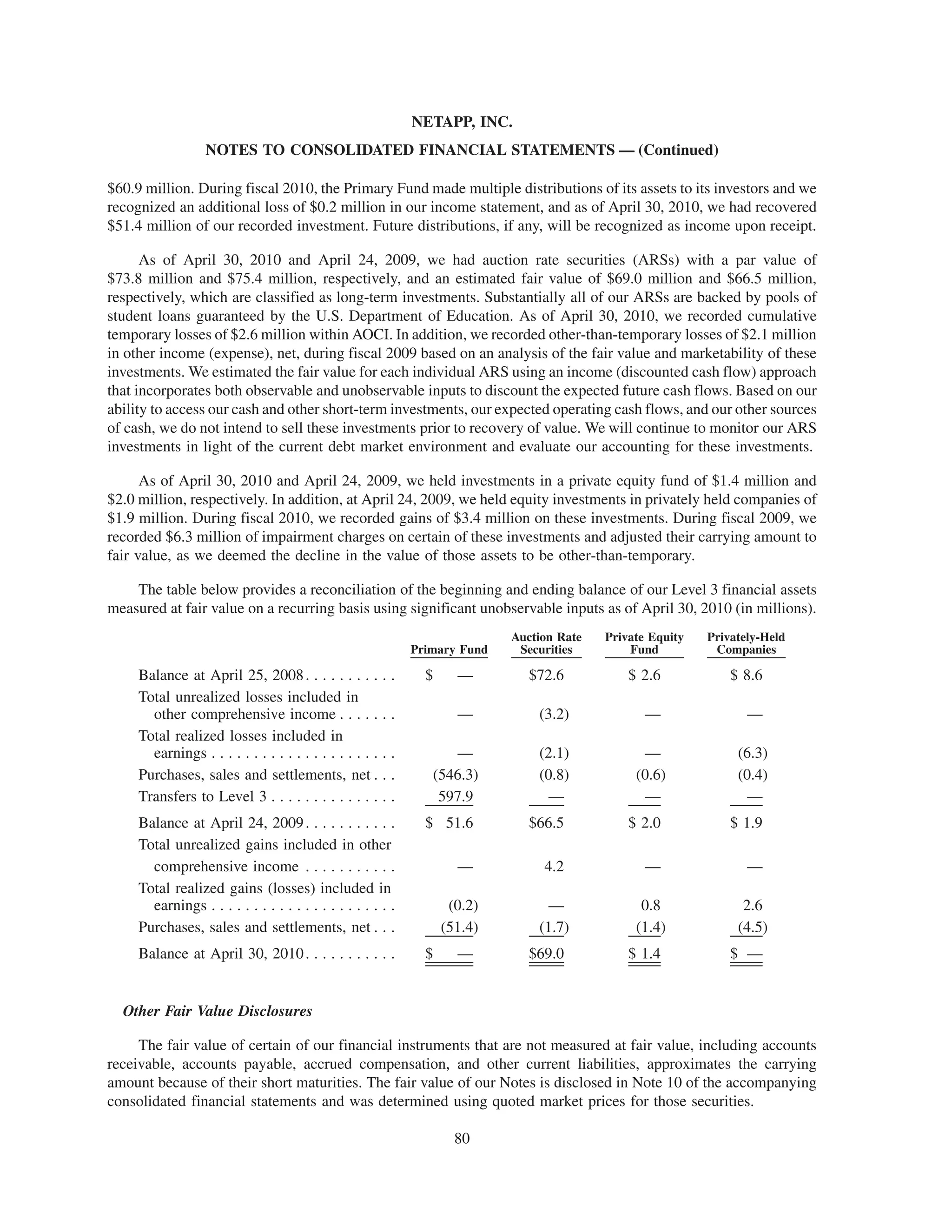

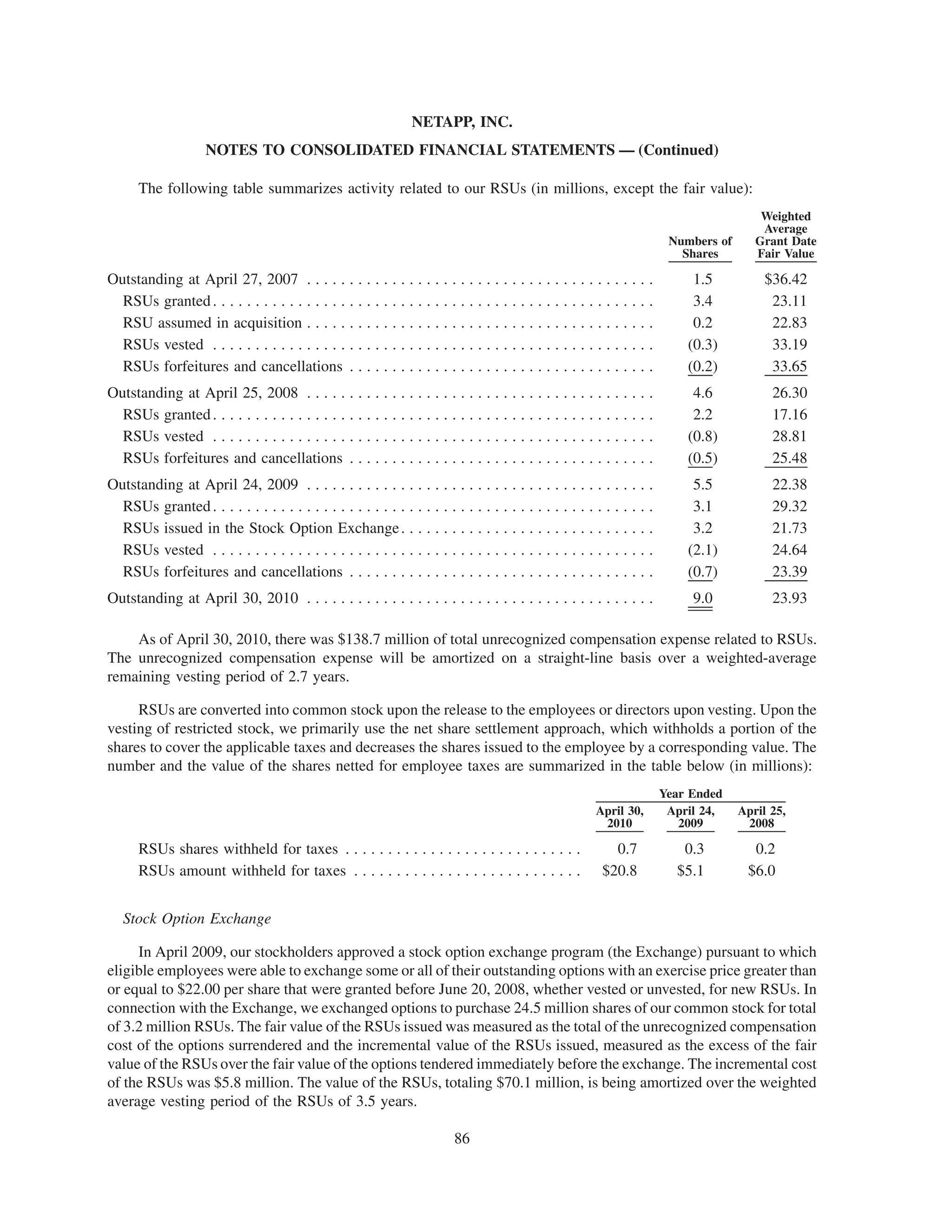

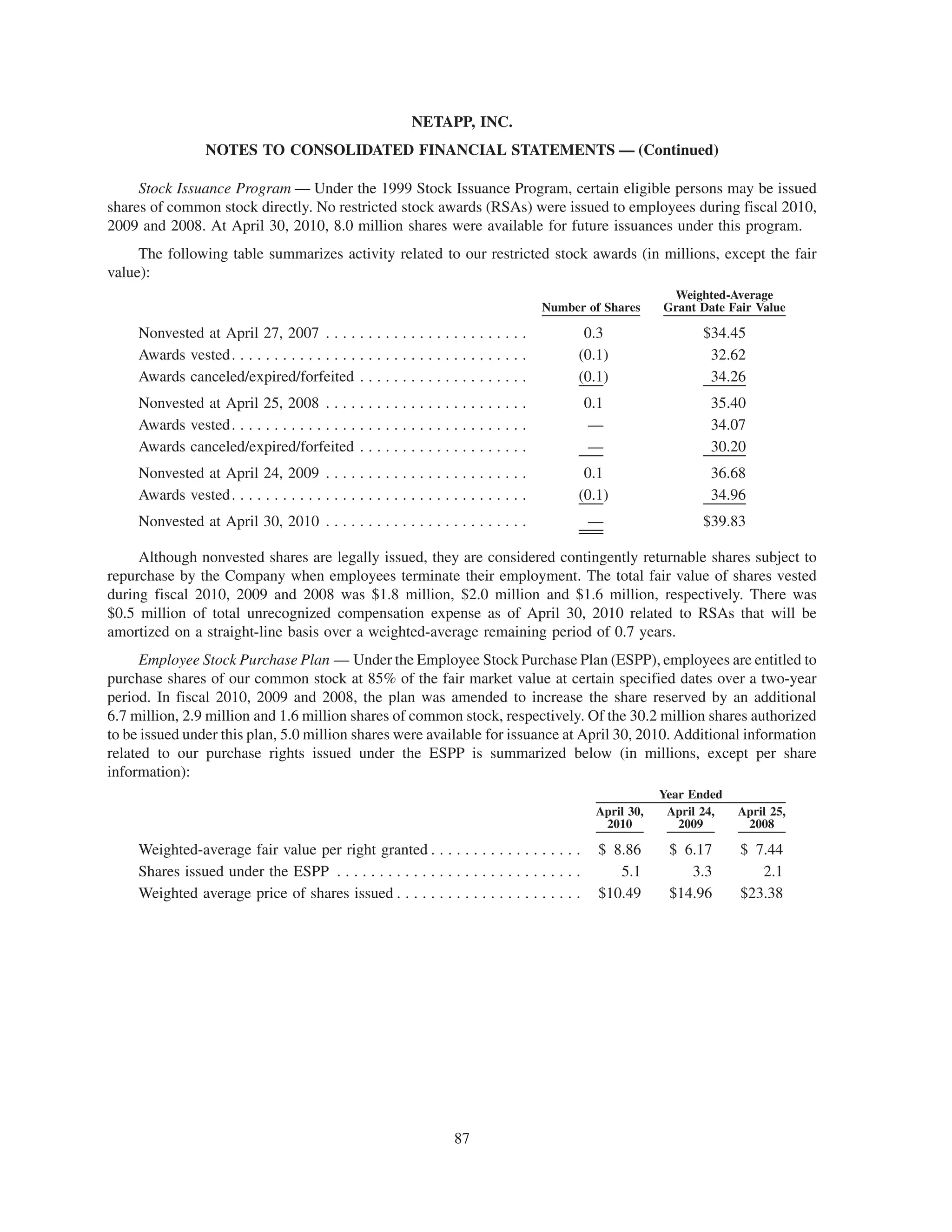

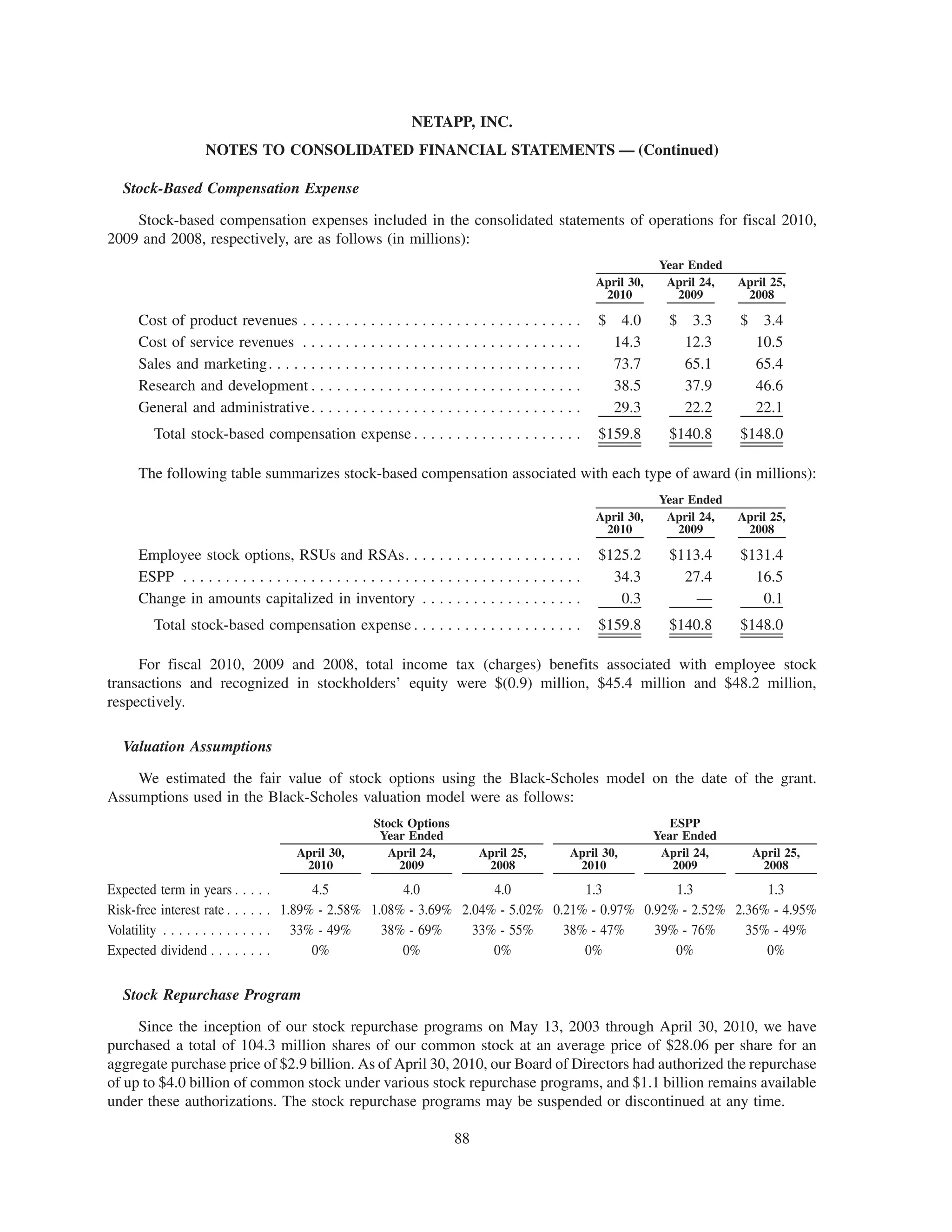

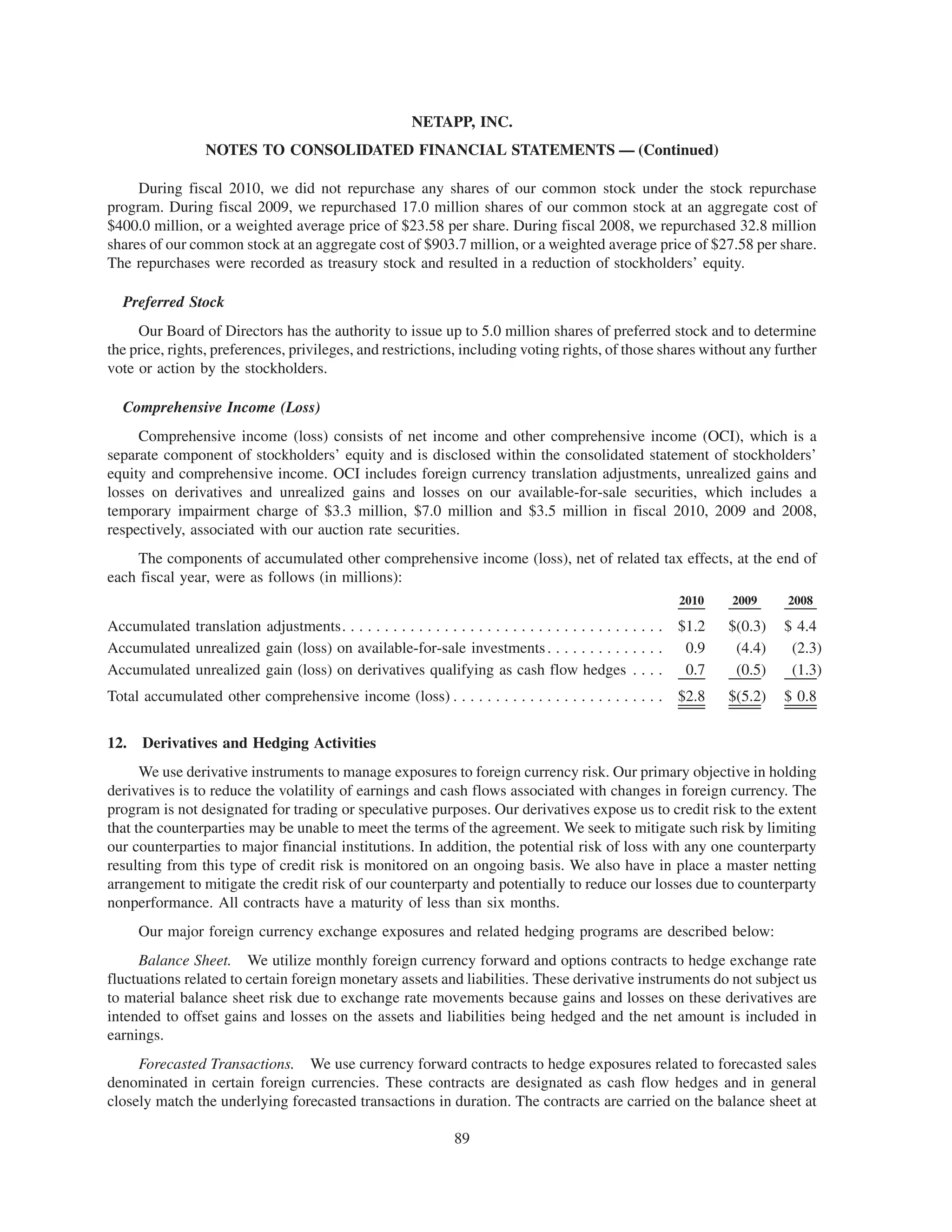

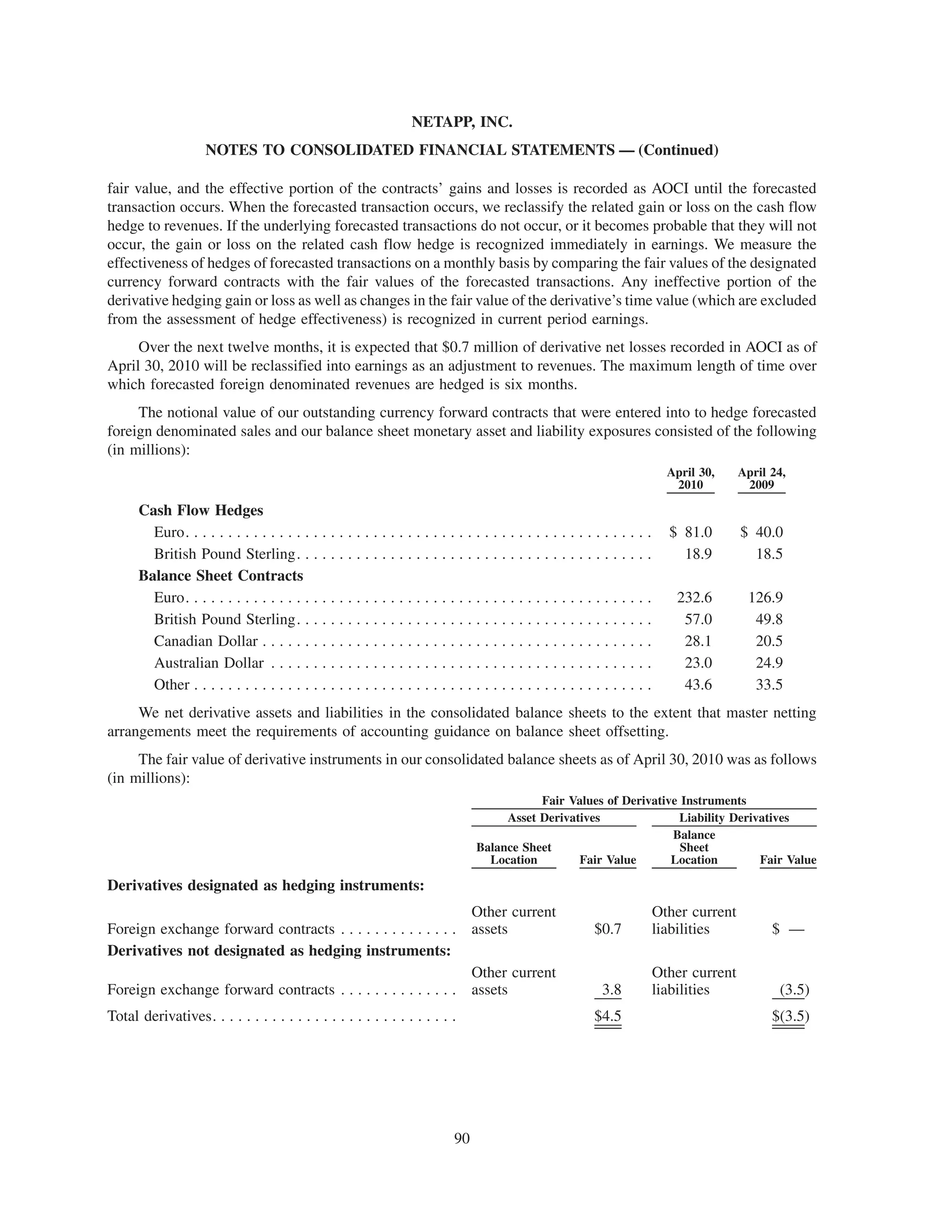

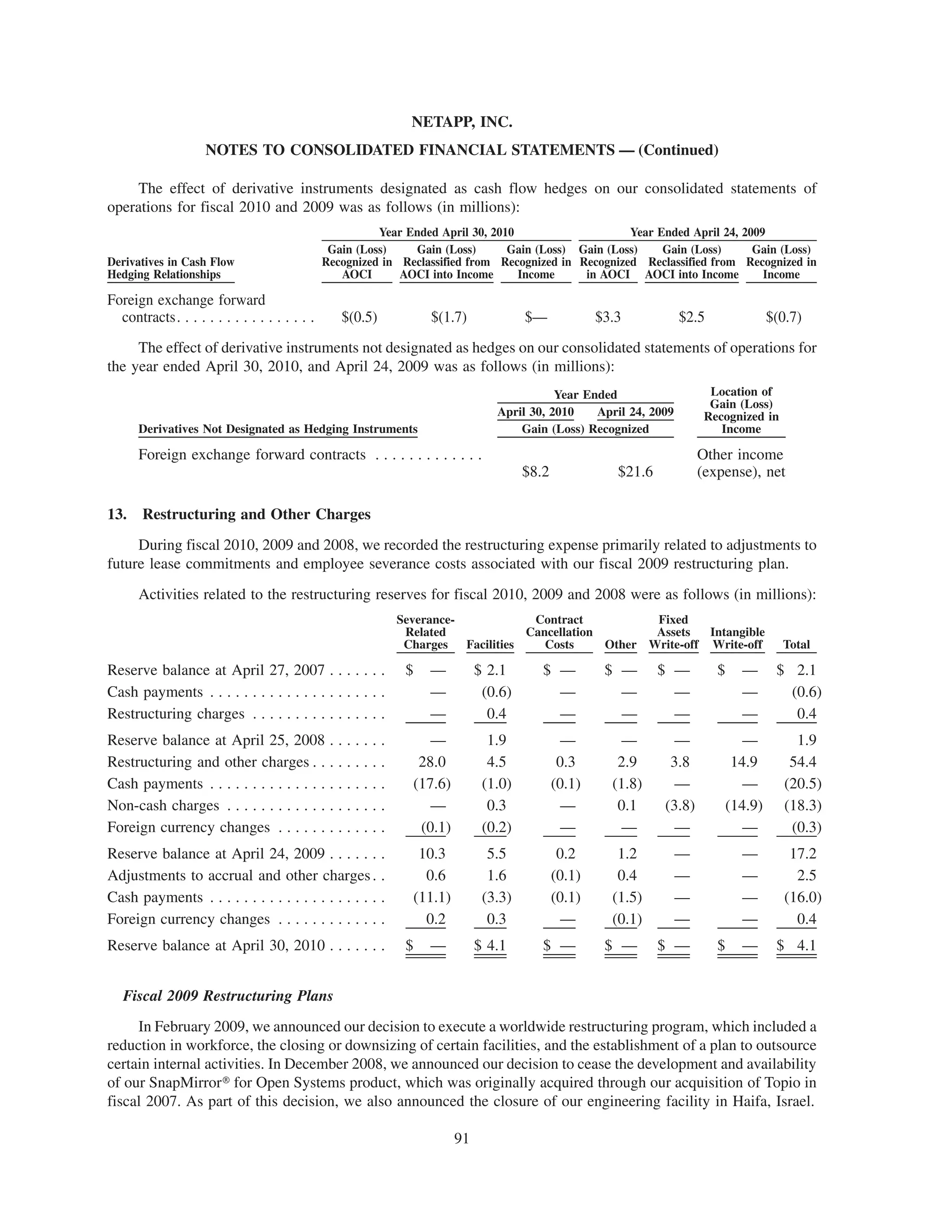

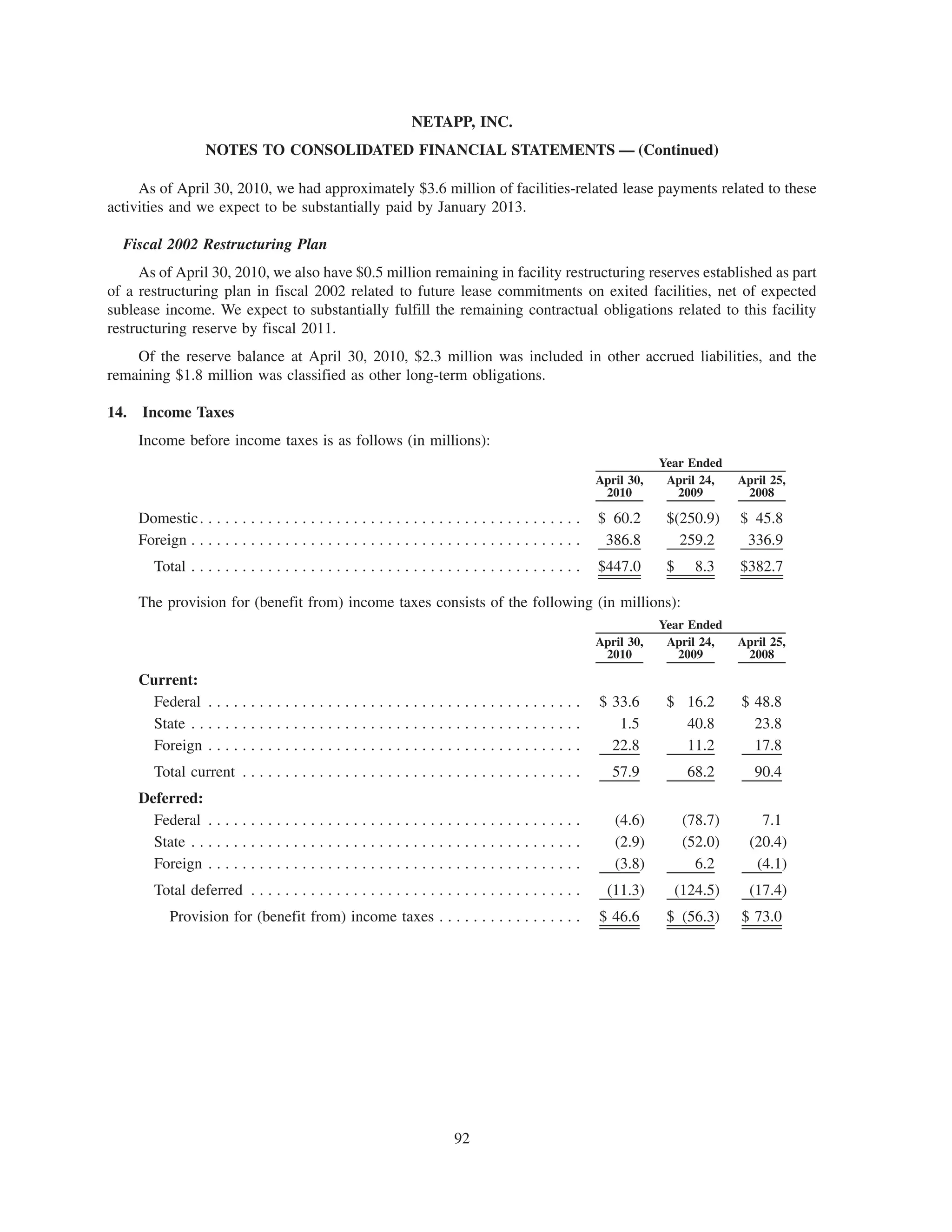

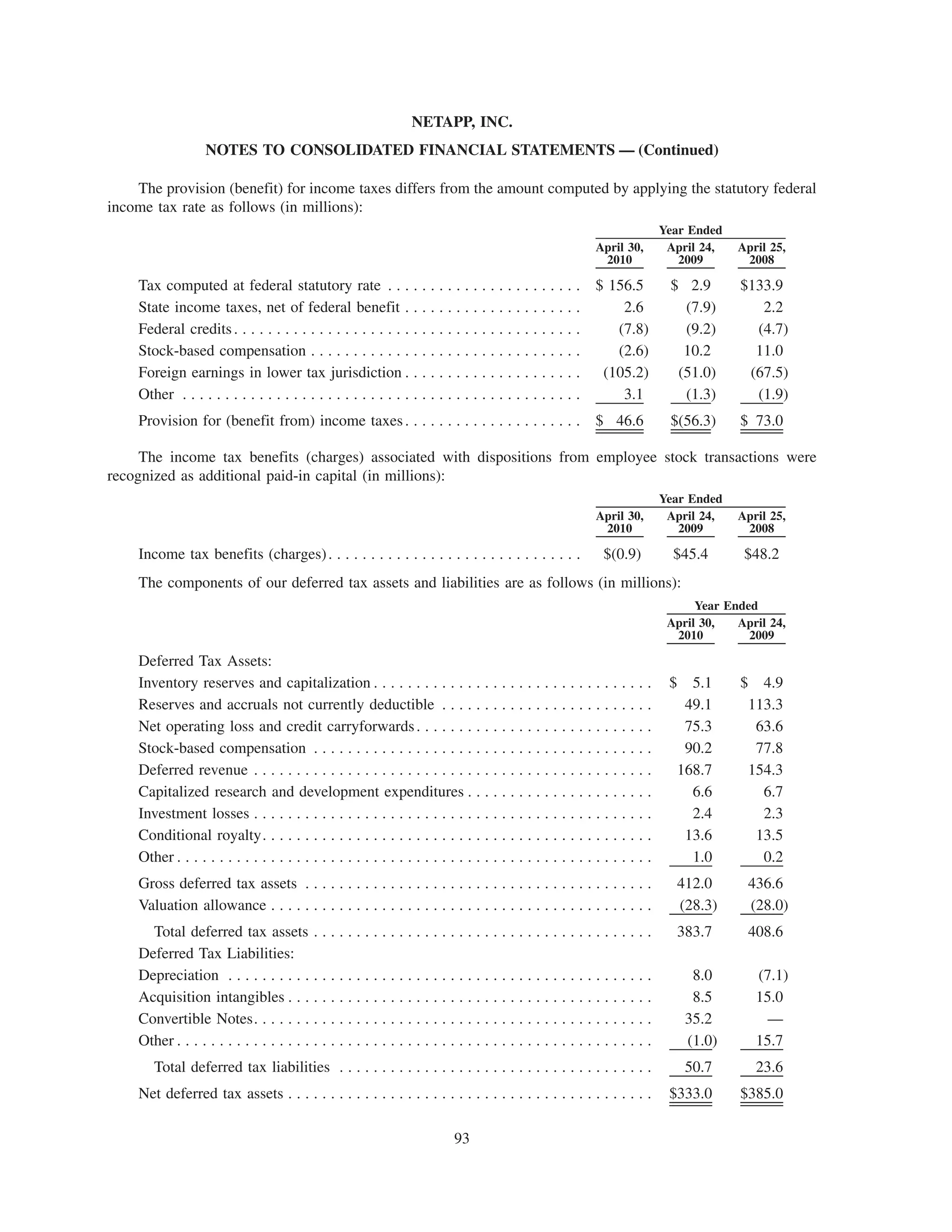

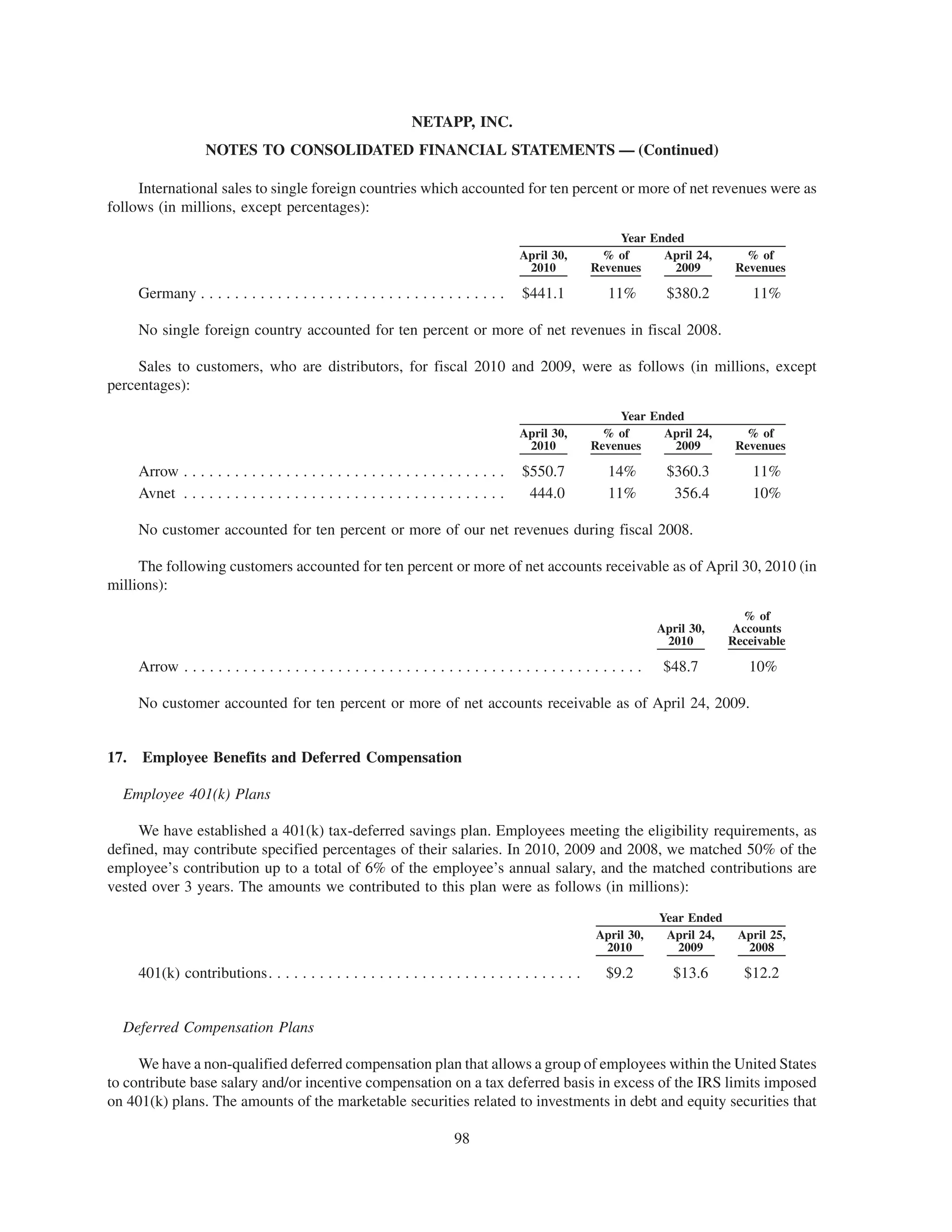

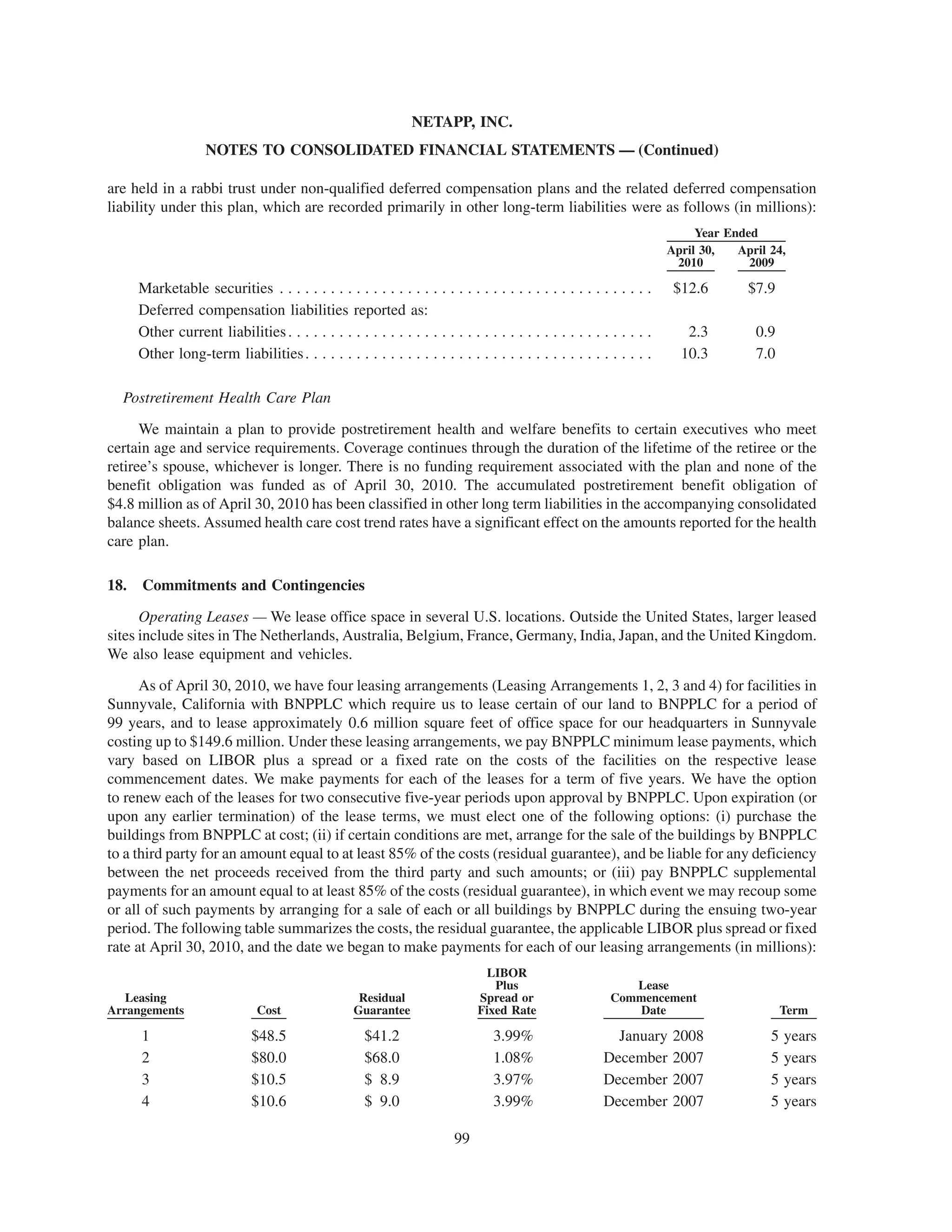

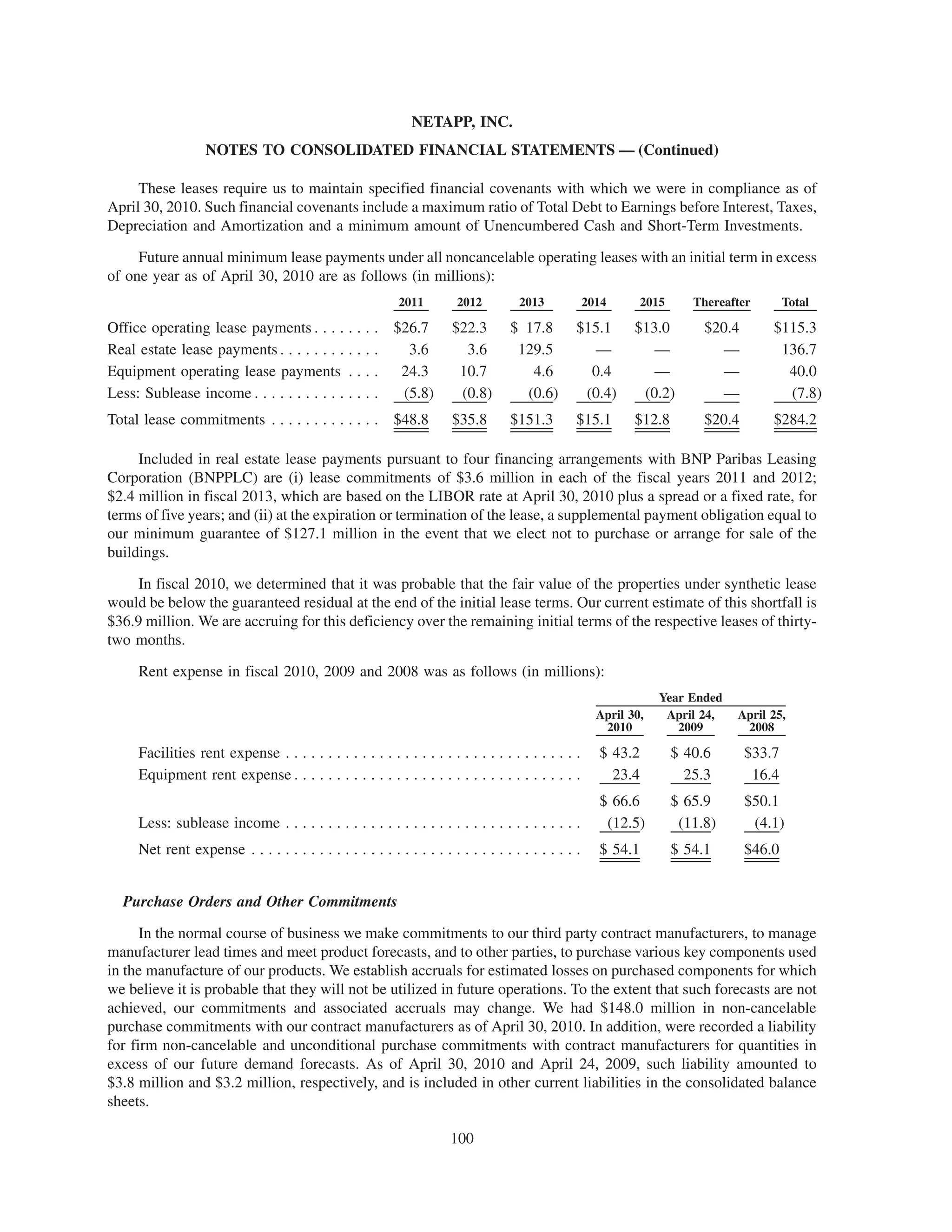

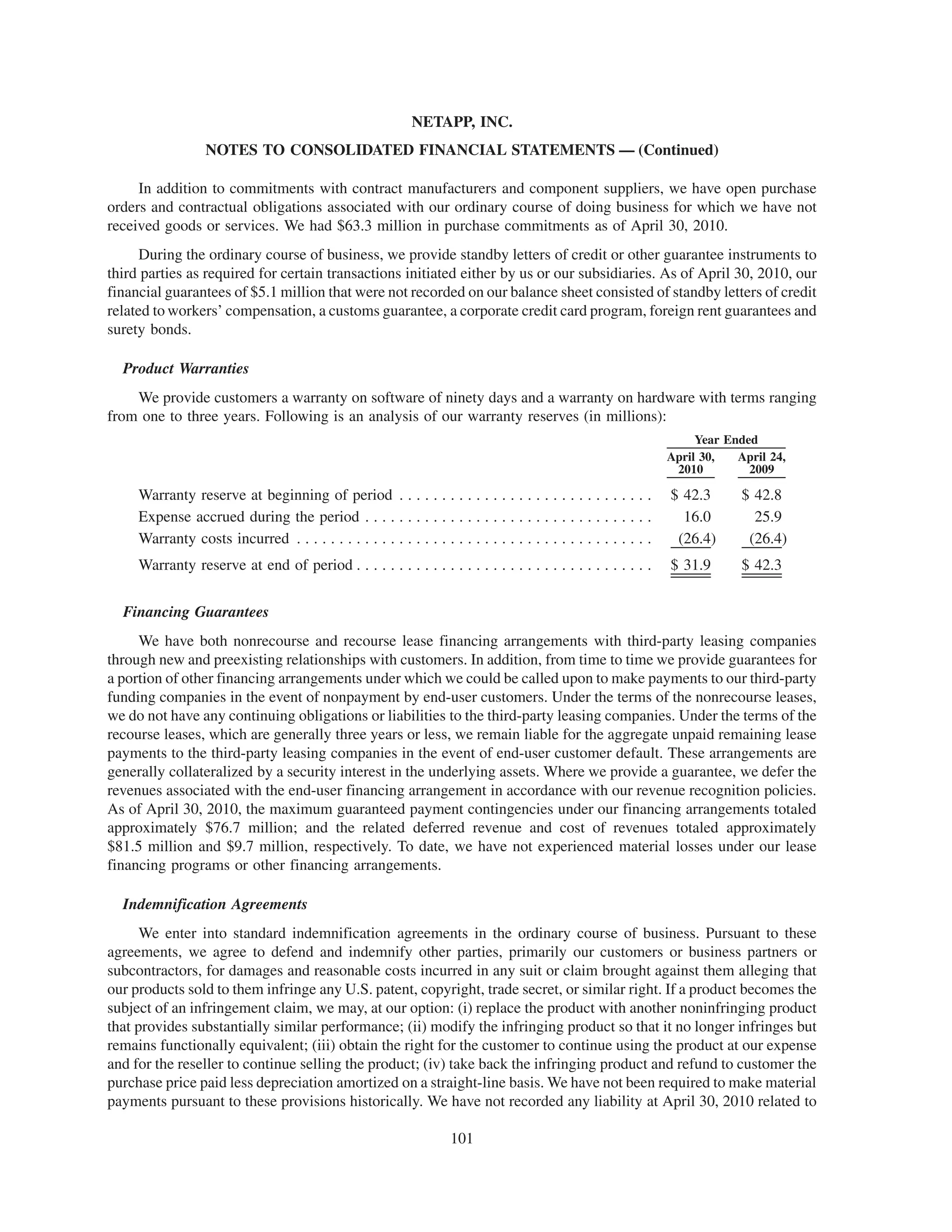

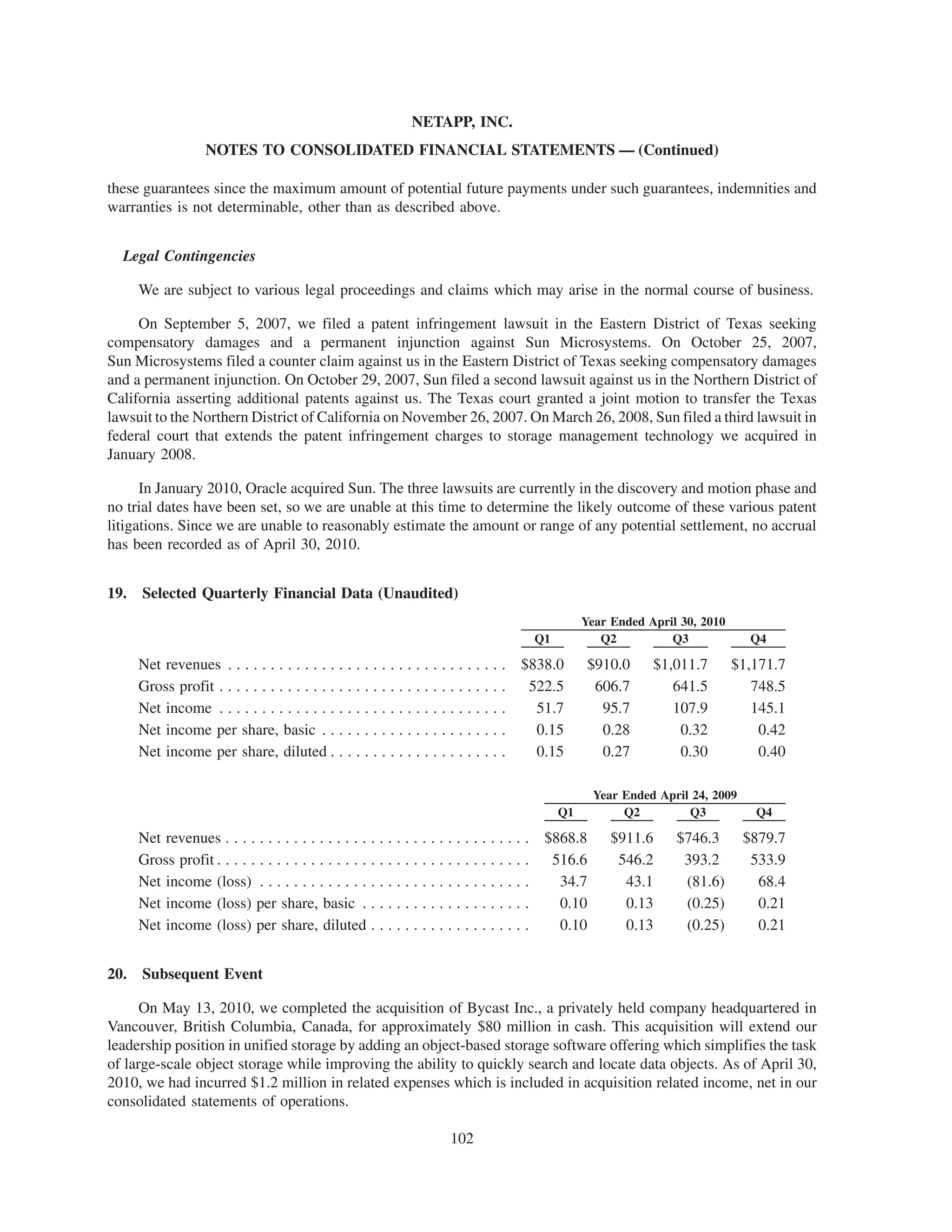

This document is NetApp's annual report on Form 10-K filed with the United States Securities and Exchange Commission for the fiscal year ending April 30, 2010. It provides an overview of NetApp's business and operations, financial statements, risks and uncertainties, and other legally required disclosures. Specifically, it discusses NetApp's data management and storage solutions business, financial results for fiscal year 2010, risk factors that could materially affect its business, and certifications regarding internal controls and disclosure controls.

![[제7회 인터넷리더십] 소통의 리더십 - 방대욱](https://cdn.slidesharecdn.com/ss_thumbnails/7-111021003434-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[인성] 멀리 가려면 함께 가라](https://cdn.slidesharecdn.com/ss_thumbnails/random-161111090732-thumbnail.jpg?width=640&height=640&fit=bounds)

![[공개용]정보보호, 우리 업무의 기본](https://cdn.slidesharecdn.com/ss_thumbnails/v1-130827234615-phpapp01-thumbnail.jpg?width=640&height=640&fit=bounds)

![[인성] 끊임없는 노력이 만들어낸 천재 스즈키 이치로](https://cdn.slidesharecdn.com/ss_thumbnails/161216-161217021341-thumbnail.jpg?width=640&height=640&fit=bounds)

![[2015체인지온] 디지털 세상 속 변화를 위한 뚜렷한 이정표 세우기 -Elizabeth Beachy](https://cdn.slidesharecdn.com/ss_thumbnails/2015-151114133649-lva1-app6892-thumbnail.jpg?width=640&height=640&fit=bounds)

![[2016 체인지온] ‘지금 여기’ 발 딛고 선 자리가 미디어의 중심_황풍년](https://cdn.slidesharecdn.com/ss_thumbnails/random-161110163619-thumbnail.jpg?width=640&height=640&fit=bounds)

![[2016 체인지온] 4차산업혁명의 도전과 기회_이원재](https://cdn.slidesharecdn.com/ss_thumbnails/4-161110162636-thumbnail.jpg?width=640&height=640&fit=bounds)