Berong Nickel Corporation - December 31, 2010

•

1 like•2,675 views

Berong Nickel Corporation The financial statements present all material respects and the financial position of Berong Nickel Corporation as at December 31, 2010 and 2009, and its financial performance and its cash flows for the years then ended in accordance with Philippine Financial Reporting Standards.

Recommended

More Related Content

What's hot

What's hot (17)

Similar to Berong Nickel Corporation - December 31, 2010

Similar to Berong Nickel Corporation - December 31, 2010 (20)

More from No to mining in Palawan

More from No to mining in Palawan (20)

Recently uploaded

Recently uploaded (20)

Berong Nickel Corporation - December 31, 2010

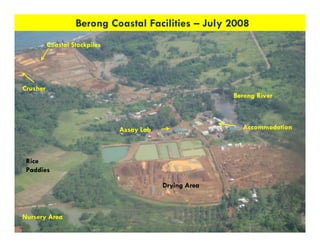

- 1. Berong Coastal Facilities – July 2008 Coastal Stockpiles Crusher Berong River Assay Lab Accommodation Rice Paddies Drying Area Nursery Area 11

- 2. Limonite benches being prepared on higher elevation for wet season mining – July 2008 Limonite Ore Saprolite Ore 12

- 3. Rehabilitation – Area 4 - Berong Water diverted around rehab area 108 Research Plots with various species of plants [with & without Top Soil] Water Management Systems 18

- 4. SyCip Gorres Velayo & Co. 6760 Ayala Avenue 1226 Makati City Philippines Phone: (632) 891 0307 Fax: (632) 819 0872 www.sgv.com.ph BOA/PRC Reg. No. 0001 SEC Accreditation No. 0012-FR-2 INDEPENDENT AUDITORS’ REPORT The Stockholders and the Board of Directors Berong Nickel Corporation Report on the Financial Statements We have audited the accompanying financial statements of Berong Nickel Corporation, which comprise the statements of financial position as at December 31, 2010 and 2009, and the statements of comprehensive income, statements of changes in equity and statements of cash flows for the years then ended, and a summary of significant accounting policies and other explanatory information. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with Philippine Financial Reporting Standards, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors’ Responsibility Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with Philippine Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. *SGVMC409311 A member firm of Ernst & Young Global Limited

- 5. -2- Opinion In our opinion, the financial statements present fairly, in all material respects, the financial position of Berong Nickel Corporation as at December 31, 2010 and 2009, and its financial performance and its cash flows for the years then ended in accordance with Philippine Financial Reporting Standards. Report on the Supplementary Information Required Under Revenue Regulations 15-2010 Our audits were conducted for the purpose of forming an opinion on the basic financial statements taken as a whole. The supplementary information on taxes, duties and license fees in Note 26 to the financial statements is presented for purposes of filing with the Bureau of Internal Revenue and is not a required part of the basic financial statements. Such information is the responsibility of the management of Berong Nickel Corporation. The information has been subjected to the auditing procedures applied in our audit of the basic financial statements. In our opinion, the information is fairly stated in all material respects in relation to the basic financial statements taken as a whole. SYCIP GORRES VELAYO & CO. Jaime F. del Rosario Partner CPA Certificate No. 56915 SEC Accreditation No. 0076-AR-2 Tax Identification No. 102-096-009 BIR Accreditation No. 08-001998-72-2009, June 1, 2009, Valid until May 31, 2012 PTR No. 2641518, January 3, 2011, Makati City March 18, 2011 *SGVMC409311

- 8. BERONG NICKEL CORPORATION STATEMENTS OF CHANGES IN EQUITY FOR THE YEARS ENDED DECEMBER 31, 2010 AND 2009 Retained Earnings Capital Stock (Deficit) Total Balances at December 31, 2008 = P303,750,000 = P249,933,080 = P553,683,080 Net loss – (142,440,297) (142,440,297) Other comprehensive income – – – Total comprehensive loss – (142,440,297) (142,440,297) Balances at December 31, 2009 303,750,000 107,492,783 411,242,783 Net loss – (134,748,908) (134,748,908) Other comprehensive income – – – Total comprehensive loss – (134,748,908) (134,748,908) Balances at December 31, 2010 = P303,750,000 (P27,256,125) = = P276,493,875 See accompanying Notes to Financial Statements. *SGVMC409311

- 9. BERONG NICKEL CORPORATION STATEMENTS OF CASH FLOWS Years Ended December 31 2010 2009 CASH FLOWS FROM OPERATING ACTIVITIES Loss before income tax (P135,100,062) = (P142,769,963) = Adjustments for: Depreciation, amortization and depletion (Notes 8 and 13) 56,323,955 54,325,231 Accretion expense for provision for mine rehabilitation and decommissioning (Notes 11 and 17) 1,170,513 1,098,887 Provision for impairment losses on trade and other receivables (Notes 5 and 13) 770,153 – Unrealized foreign exchange gains - net (520,797) (1,116,042) Loss (gain) on disposals of property and equipment (Note 18) 327,381 (347,731) Interest income (123,074) (177,337) Movement in accrued rent (Note 21) 61,786 – Interest expense (Note 17) – 151 Operating loss before changes in working capital (77,090,145) (88,986,804) Decrease (increase) in: Trade and other receivables 3,451,157 (940,949) Inventories (1,472,052) 75,787,720 Other current assets (658,294) (73,930) Decrease in trade and other payables (4,788,862) (45,496,708) Net cash used in operations (80,558,196) (59,710,671) Interest received 123,074 177,337 Interest paid – (151) Net cash flows used in operating activities (80,435,122) (59,533,485) CASH FLOWS FROM INVESTING ACTIVITIES Proceeds from disposal of property and equipment 600,000 1,181,920 Acquisitions of property and equipment (Note 8) (229,441) (7,604,767) Decrease (increase) in: Deferred mine exploration costs (28,581,470) (3,364,402) Other noncurrent assets 1,485,788 3,984,111 Net cash flows used in investing activities (26,725,123) (5,803,138) CASH FLOW FROM FINANCING ACTIVITY Additional advances from stockholders 70,513,338 46,834,677 NET DECREASE IN CASH AND CASH EQUIVALENTS (36,646,907) (18,501,946) EFFECT ON CASH AND CASH EQUIVALNTS OF CHANGES IN FOREIGN EXCHANGE RATE 14,060 (314,523) CASH AND CASH EQUIVALENTS AT BEGINNING OF YEAR 51,229,287 70,045,756 CASH AND CASH EQUIVALENTS AT END OF YEAR P14,596,440 = = P51,229,287 See accompanying Notes to Financial Statements. *SGVMC409311

- 10. BERONG NICKEL CORPORATION NOTES TO FINANCIAL STATEMENTS 1. Corporate Information and Status of Operations a. Corporate Information Berong Nickel Corporation (the Company) was registered with the Philippine Securities and Exchange Commission on September 27, 2004, for the purpose of exploring, developing and mining the Berong Mineral Properties located in Barangay Berong, Quezon, province of Palawan. The Company shall have the exclusive privilege and right to explore, develop, mine, operate, produce, utilize, process and dispose of all the minerals and the products or by-products that may be produced, extracted, gathered, recovered, unearthed or found within the Mineral Properties, inclusive of Direct Shipping Project, under a Mineral Production Sharing Agreement (MPSA) with the Government of the Philippines or under any appropriate rights granted by law or the Government of the Philippines. The Company is 60%-owned by Nickeline Resources Holdings, Inc. (NRHI), 21.3%-owned by Toledo Mining Corporation (TMC) and 18.7%-owned by European Nickel Plc (EN). Its ultimate parent is Atlas Consolidated Mining and Development Corporation (ACMDC). The registered office address of the Company is 7th Flr. Quad Alpha Centrum, 125 Pioneer Street, Mandaluyong City. b. Status of Operations Mining Project In 2005, following the grant of temporary exploration permit by the Philippine Government, the Company commenced a confirmatory exploration and resampling program in the initial production area of the “Berong Nickel Mining Project” (the Berong Project). In 2006, after establishing that economically recoverable reserves exist in the area, the Company proceeded to develop the area into commercial mining operation. On November 24, 2006, the Company was issued a Special Mines Permit (SMP) by the Department of Environment and Natural Resources (DENR), through the Mines and Geosciences Bureau (MGB) subject to the pertinent provisions of DENR Administrative Order No. 96-40. The issuance of the SMP allowed the Company to commence its mining operations while it completes a feasibility report as part requirement for the Company’s commercial MPSA application. On June 8, 2007, the government approved MPSA No. 235-2007-IVB in favor of the Company as the Contractor. The MPSA covers a contract area of approximately two hundred eighty-eight (288) hectares situated in Barangay Berong, Municipality of Quezon, Province of Palawan. In November 2008, the Company has decided not to continue its mining operations in the Berong Project due to low nickel prices and demand. The Company continues to assess the potential to re-open the Berong Project as a direct shipping operation, but no decision has been made yet to resume mining operations. *SGVMC409311

- 11. -2- On February 12, 2010, MGB granted Exploration Permit (EP) No. EP-002-2010IVB in favor of the Company. The EP covers an area of approximately one thousand sixty-nine (1,069) hectares situated in the Municipalities of Quezon and Aborlan, Province of Palawan. The EP shall be for a period of two (2) years from the date of issuance thereof. Registration with the Board of Investments (BOI) On May 28, 2007, the Company was registered with the BOI as a new producer of beneficiated nickel ore on a non-pioneer status. On November 5, 2010, BOI has approved the extension of Income Tax Holiday (ITH) period of the Company for another year until May 27, 2012 (see Note 25). The Company has been certified by BOI as a qualified enterprise for the purpose of Value Added Tax (VAT) zero-rating of its transactions pursuant to the terms and conditions set forth by the BOI. On January 22, 2010, the Company received the renewed certification of BOI for the Value Added Tax (VAT)-zero rated status, which is valid until December 31, 2010. In 2011, the registration was not renewed since the Company has no export sales in 2010, which is one of the requirements of the said certification. The financial statements of the Company as at and for the years ended December 31, 2010 and 2009 were authorized for issue by the Board of Directors (BOD) on March 18, 2011. 2. Basis of Preparation, Statement of Compliance and Summary of Significant Accounting Policies Basis of Preparation The Company’s financial statements have been prepared on a historical cost basis and are presented in Philippine peso, which is the Company’s functional and presentation currency. All values are rounded to the nearest Philippine peso, except as otherwise stated. Statement of Compliance The financial statements of the Company have been prepared in compliance with Philipppine Financial Reporting Standards (PFRS). Changes in Accounting Policies The accounting policies adopted are consistent with those of the previous financial year except for the following new and amended PFRSs, Philippine Accounting Standards (PAS), Philippine Interpretation International Financial Reporting Interpretations Committee (IFRIC) and improvements to PFRSs, which were adopted as at January 1, 2010: Amended and Revised Standards and New Interpretation · Revised PFRS 3, Business Combinations and Amended PAS 27, Consolidated and Separate Financial Statements · Philippine Interpretation IFRIC 17, Distributions of Non-Cash Assets to Owners Amendments and Improvements to Standards · Amendment to PAS 39, Financial Instruments: Recognition and Measurement, Eligible Hedged Items · Amendment to PFRS 2, Share-based Payment, Group Cash-settled Share-based Payment Transactions *SGVMC409311

- 12. -3- · Improvements to PFRSs 2008, with respect to PFRS 5, Noncurrent Assets Held for Sale and Discontinued Operations · Improvements to PFRSs 2009 The new, revised, amended and improved standards and/or interpretations that have been adopted are deemed to have no impact on the financial position or performance of the Company. Future Changes in Accounting Policies The Company did not early adopt the following standards and Philippine Interpretations that will become effective subsequent to December 31, 2010: Effective in 2011: · Amendment to PAS 24, Related Party Disclosures, effective for annual periods beginning on or after January 1, 2011, with earlier adoption permitted for either the partial exemption for government-related entities or for the entire standard. It clarified the definition of a related party to simplify the identification of such relationships and to eliminate inconsistencies in its application. The amended standard introduces a partial exemption of disclosure requirements for government-related entities. · Amendment to PAS 32, Financial Instruments: Presentation, Classification of Rights Issues, effective for annual periods beginning on or after February 1, 2010. It amended the definition of a financial liability in order to classify rights issues (and certain options or warrants) as equity instruments in cases where such rights are given pro rata to all of the existing owners of the same class of an entity’s non-derivative equity instruments, or to acquire a fixed number of the entity’s own equity instruments for a fixed amount in any currency. · Amendment to Philippine Interpretation IFRIC 14, Prepayments of a Minimum Funding Requirement, effective for annual periods beginning or after January 1, 2011, with retrospective application. The amendment provides guidance on assessing the recoverable amount of a net pension asset. The amendment permits an entity to treat the prepayment of a minimum funding requirement as an asset. · Philippine Interpretation IFRIC 19, Extinguishing Financial Liabilities with Equity Instruments, effective for annual periods beginning on or after July 1, 2010 with earlier application permitted. The interpretation clarifies that equity instruments issued to a creditor to extinguish a financial liability qualify as consideration paid. The equity instruments issued are measured at their fair value. In case that this cannot be reliably measured, the instruments are measured at the fair value of the liability extinguished. Any gain or loss is recognized immediately in the statement of comprehensive income. *SGVMC409311

- 13. -4- Improvements to PFRS 2010 The omnibus amendments to PFRS issued in 2010 were issued primarily with a view of removing inconsistencies and clarifying wordings. The amendments are effective for annual periods beginning on or after January 1, 2011, except when otherwise stated. · PFRS 3, Business Combinations, effective for annual reporting periods beginning on or after July 1, 2010, clarifies that the amendments to PFRS 7, Financial Instruments: Disclosures, PAS 32 and PAS 39 that eliminate the exemption for contingent consideration, do not apply to contingent consideration that arose from business combinations whose acquisition dates precede the application of PFRS 3 (as revised in 2008). The amendment will be applied retrospectively. The amendment also limits the scope of the measurement choices that only the components of non-controlling interest that are present ownership interests that entitle their holders to a proportionate share to the entity’s net assets, in the event of liquidation, shall be measured either at fair value or at present ownership instrument’s proportionate share of the acquiree’s identifiable net assets. Other components of non-controlling interest are measured at their acquisition date fair value, unless another measurement basis is required by another PFRS. The amendment will be applied prospectively from the date the entity applies revised PFRS 3. Further, the amendment requires an entity in a business combination to account for the replacement of the acquiree’s share-based payment transactions, whether obliged or voluntarily, such as split between considerations and post-combination expenses. However, if the entity replaces the acquiree’s awards that expire as a consequence of the business combination, these are recognized as post-combination expenses. The amendment also specifies the accounting for share-based payment transactions that the acquirer does not exchange for its own awards: if vested - they are part of non-controlling interest and measured at their market-based measure; if unvested - they are measured at market-based value as if granted at acquisition date, and allocated between non-controlling interest and post-combination expenses. The amendment will be applied prospectively. · PFRS 7, Financial Instruments: Disclosures, emphasizes the interaction between quantitative and qualitative disclosures and the nature and extent of risks associated with financial instruments. The amendment will be applied retrospectively. · PAS 1, Presentation of Financial Statements, clarifies that an entity will present an analysis of other comprehensive income for each component of equity, either in the statement of changes in equity or in the notes to the financial statements. The amendment will be applied retrospectively. · PAS 27, Consolidated and Separate Financial Statements, effective for annual reporting periods beginning on or after July 1, 2010, clarifies that the consequential amendments from PAS 27 made to PAS 21, The Effect of Changes in Foreign Exchange Rates, PAS 28, Investments in Associates and PAS 31, Interests in Joint Ventures, apply prospectively for annual periods beginning on or after July 1, 2009 or earlier when PAS 27 is applied earlier. The amendment will be applied retrospectively. *SGVMC409311

- 14. -5- · Philippine Interpretation IFRIC 13, Customer Loyalty Programmes, clarifies that when the fair value of award credits is measured based on the value of the awards for which they could be redeemed, the amount of discounts or incentives otherwise granted to customers not participating in the award credit scheme, is to be taken into account. The amendment will be applied retrospectively. Effective in 2012: · Amendment to PAS 12, Income Taxes - Deferred Tax: Recovery of Underlying Assets, effective for annual periods beginning or after January 1, 2012. The amendment provides a practical solution to the problem of assessing whether recovery of an asset will be through use or sale. It introduces a presumption that recovery of the carrying amount of an asset will, normally, be through sale. · Amendments to PFRS 7, Financial Instruments: Disclosures - Transfers of Financial Assets, effective for annual periods beginning on or after July 1, 2011. The amendments will allow users of financial statements to improve their understanding of transfer transactions of financial assets (for example, securitizations), including understanding the possible effects of any risks that may remain with the entity that transferred the assets. The amendments also require additional disclosures if a disproportionate amount of transfer transactions are undertaken around the end of a reporting period. · Philippine Interpretation IFRIC 15, Agreement for Construction of Real Estate, effective for annual periods beginning or after January 1, 2012, covers accounting for revenue and associated expenses by entities that undertake the construction of real estate directly or through subcontractors. This Interpretation requires that revenue on construction of real estate be recognized only upon completion, except when such contract qualifies as construction contract to be accounted for under PAS 11, Construction Contracts, or involves rendering of services in which case revenue is recognized based on stage of completion. Contracts involving provision of services with the construction materials and where the risks and reward of ownership are transferred to the buyer on a continuous basis will also be accounted for based on stage of completion. Effective in 2013: · PFRS 9, Financial Instruments: Classification and Measurement, effective for annual periods beginning on or after January 1, 2013, introduces new requirements on the classification and measurement of financial assets. It uses a single approach to determine whether a financial asset is measured at amortized cost or fair value, replacing the many different rules in PAS 39, Financial Instruments: Recognition and Measurement. The approach in the new standard is based on how an entity manages its financial instruments (its business model) and the contractual cash flow characteristics of the financial assets. The new standard also requires a single impairment method to be used, replacing the many different impairment methods in PAS 39. The Company does not expect any significant impact in the financial statements when it adopts the above standards and interpretations. The revised, amended and additional disclosures provided by the standards and interpretations will be included in the financial statements in the year of adoption, where applicable. *SGVMC409311

- 15. -6- Summary of Significant Accounting Policies Presentation of Financial Statements The Company has elected to present all items of recognized income and expense in one single statement of comprehensive income. Cash and Cash Equivalents Cash and cash equivalents include cash on hand and with banks and short-term cash investments that are highly liquid with original maturity of three (3) months or less. Financial Instruments Initial Recognition and Measurement of Financial Instruments The Company determines the classification of financial instruments at initial recognition and, where allowed and appropriate, re-evaluates this designation at every end of the reporting period. Financial instruments are recognized initially at fair value. Directly attributable transaction costs are included in the initial measurement of all financial instruments, except for financial instruments measured at fair value through profit or loss (FVPL). Financial Assets Financial assets within the scope of PAS 39 are classified as at FVPL, loans and receivables, available-for-sale (AFS) investments, held-to-maturity (HTM) investments, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. Purchases or sales of financial assets that require delivery of assets within a time frame established by regulation or convention in the marketplace (regular way trades) are recognized on the trade date (i.e., the date that the Company commits to purchase or sell the asset). The Company’s financial assets are in the nature of loans and receivables. The Company has no financial assets classified as at FVPL, AFS investments, HTM investments and derivatives designated as hedging instruments in an effective hedge as at December 31, 2010 and 2009. Financial Liabilities Financial liabilities within the scope of PAS 39 are classified as at FVPL, loans and borrowings, or as derivatives designated as hedging instruments in an effective hedge, as appropriate. Financial instruments are classified as liabilities or equity in accordance with the substance of the contractual arrangement. Interest, dividends, gains and losses relating to a financial instrument or a component that is a financial liability, are reported as expense or income. Distributions to holders of financial instruments classified as equity are charged directly to equity net of any related income tax. The Company’s financial liabilities are in the nature of loans and borrowings. The Company has no financial liabilities classified as at FVPL and derivatives designated as hedging instrument in an effective hedge as at December 31, 2010 and 2009. *SGVMC409311

- 16. -7- Subsequent Measurement The subsequent measurement of financial instruments depends on their classification as follows: Loans and Receivables Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. After initial measurement, loans and receivables are subsequently measured at amortized cost using the effective interest rate method, less allowance for impairment, in the statement of financial position. Amortized cost is calculated by taking into account any discount or premium on acquisition and fees and costs that are an integral part of the effective interest rate. Gains and losses are recognized in the statement of comprehensive income when the loans are derecognized or impaired as well as through the amortization process. Loans and receivables are included in current assets if maturity is within twelve (12) months from the end of the reporting period. Otherwise, these are classified as noncurrent assets. As at December 31, 2010 and 2009, the Company’s loans and receivables pertain to cash and cash equivalents, trade and other receivables, which are classified under current assets, and Mine Rehabilitation Fund (MRF), which is included under “Other noncurrent assets”. Loans and Borrowings This category pertains to financial liabilities that are not held for trading, not derivatives, or not designated as at FVPL upon the inception of the liability. These financial liabilities are subsequently carried at amortized cost, taking into account the impact of applying the effective interest method of amortization or accretion for any related premium, discount and any directly attributable transaction cost. Loans and borrowings are included under current liabilities if it will be settled within 12 months after the end of the reporting period or within the Company’s operating cycle, whichever is longer. Otherwise, these are classified as noncurrent liabilities. As at December 31, 2010 and 2009, the Company’s loans and borrowings pertain to trade and other payables, advances from stockholders and dividends payable, which are classified under current liabilities. Determination of Fair Values of Financial Instruments The fair value of financial instruments that are traded in active markets at each end of the reporting period is determined by reference to quoted market prices or dealer price quotations, bid price for long positions and ask price short positions, without any deduction for transaction costs. For financial instruments not traded in an active market, the fair value is determined using appropriate valuation techniques. Such techniques may include using recent arm’s length market transactions; reference to the current fair value of another instrument that is substantially the same; a discounted cash flow analysis or other valuation models. The Company uses hierarchy below in determining and disclosing the fair value of financial instruments by valuation technique: · Level 1 - Quoted prices in active markets for identical asset or liability; · Level 2 - Those involving inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (as prices) or indirectly (derived from prices); and *SGVMC409311

- 17. -8- · Level 3 - Those with inputs for asset or liability that are not based on observable market data (unobservable inputs). When fair values of listed equity and debt securities as well as publicly traded derivatives at the end of the reporting period are based on quoted market prices or binding dealer price quotations without any deduction for transaction costs, the instruments are included within Level 1 of the hierarchy. For all other financial instruments, fair value is determined using valuation technique. Valuation techniques include net present value techniques, comparison to similar instruments for which market observable prices exist, option pricing models and other relevant valuation model. For these financial instruments, inputs into models are market observable and are therefore included within Level 2. Instruments included in Level 3 include those for which there is currently no active market. An analysis of fair values of financial instruments and further details as to how they are measured are provided in Note 23. Offsetting of Financial Instruments Financial assets and financial liabilities are only offset and the net amount reported in the statement of financial position when there is a legally enforceable right to offset the recognized amounts and the Company intends to either settle on a net basis, or to realize the asset and the liability simultaneously. Impairment of Financial Assets Carried at Amortized Cost The Company assesses at each end of the reporting period whether there is objective evidence that a specific financial asset or group of financial assets may be impaired. The Company first assesses whether objective evidence of impairment exists individually for financial assets that are individually significant, and individually or collectively for financial assets that are not individually significant. The factors in determining whether objective evidence of impairment exist include, but are not limited to, the length of the Company’s relationship with debtors, their payment behavior and known market factors. Evidence of impairment may also include indications that the borrowers are experiencing significant difficulty, default and delinquency in payments, the probability that they will enter bankruptcy, or other financial reorganization and where observable data indicate that there is measurable decrease in the estimated future cash flows, such as changes in arrears or economic conditions that correlate with defaults. If it is determined that no objective evidence of impairment exists for an individually assessed financial asset, whether significant or not, the asset is included in a group of financial asset with similar credit risk characteristics and that group of financial assets is collectively assessed for impairment. Assets that are individually assessed for impairment and for which an impairment loss is or continues to be recognized are not included in a collective assessment of impairment. If there is objective evidence that an impairment loss on loans and receivables carried at amortized cost has been incurred, the amount of the loss is measured as the difference between the asset’s carrying amount and the present value of estimated future cash flows (excluding future credit losses that have not been incurred) discounted at the financial asset’s original effective interest rate (i.e., the effective interest rate computed at initial recognition). The carrying amount of the asset shall be reduced either directly or through use of an allowance account. The amount of the loss shall be recognized in the statement of comprehensive income. *SGVMC409311

- 18. -9- If, in a subsequent period, the amount of the impairment loss decreases and the decrease can be related objectively to an event occurring after the impairment was recognized, the previously recognized impairment loss is reversed. Any subsequent reversal of an impairment loss is recognized in the statement of comprehensive income, to the extent that the carrying value of the asset does not exceed its amortized cost at the reversal date. Impairment losses are estimated by taking into consideration the following information: current economic conditions, the approximate delay between the time a loss is likely to have been incurred and the time it will be identified as requiring an individually assessed impairment allowance, and expected receipts and recoveries once impaired. Management is responsible for deciding the length of this period which can extend for as long as one year. Derecognition of Financial Instruments Financial Assets A financial asset (or, where applicable a part of a financial asset or part of a group of similar financial assets) is derecognized when: · the rights to receive cash flows from the asset have expired; · the Company retains the right to receive cash flows from the asset, but has assumed an obligation to pay them in full without material delay to a third party under a “pass-through” arrangement; or · the Company has transferred its rights to receive cash flows from the asset and either: (a) has transferred substantially all the risks and rewards of the asset, or (b) has neither transferred nor retained substantially all the risks and rewards of the asset, but has transferred control of the asset. When the Company has transferred its rights to receive cash flows from an asset and has neither transferred nor retained substantially all the risks and rewards of the asset nor transferred control of the asset, the asset is recognized to the extent of the Company’s continuing involvement in the asset. Continuing involvement that takes the form of a guarantee over the transferred asset is measured at the lower of the original carrying amount of the asset and the maximum amount of consideration that the Company could be required to repay. Financial Liabilities A financial liability is derecognized when the obligation under the liability is discharged, cancelled or has expired. When an existing financial liability is replaced by another from the same lender on substantially different terms, or the terms of an existing liability are substantially modified, such an exchange or modification is treated as a derecognition of the original liability and the recognition of a new liability, and the difference in the respective carrying amounts is recognized in the statement of comprehensive income. *SGVMC409311

- 19. - 10 - Inventories Inventories are valued at the lower of cost or net realizable values (NRV). Cost is determined by the moving average production cost during the period for beneficiated nickel ore exceeding a determined cut-off grade and for fuel and supplies. NRV for beneficiated nickel ore is the estimated selling price in the ordinary course of business, less estimated costs of completion and the estimated costs necessary to make the sale. NRV for supplies and fuel is the current replacement cost. Property and Equipment Property and equipment, except land, is stated at cost, excluding the costs of day-to-day servicing, less accumulated depreciation, amortization and depletion and any accumulated impairment in value. Such cost includes the cost of replacing part of such property and equipment when that cost is incurred if the recognition criteria are met. Land is carried at cost less accumulated impairment in value, if any. Depreciation and amortization are computed on a straight-line basis over the following estimated useful lives of the assets or the term of the lease, whichever is shorter, in case of leasehold improvements. Category Number of Years Leasehold improvements 5-10 Laboratory and other equipment 5-10 Transportation equipment 5 Office equipment 5 Mine and mining properties consists of mine development costs, capitalized cost of mine rehabilitation and decommissioning (refer to accounting policy on “Provision for mine rehabilitation and decommissioning”) and mining rights. Mine development costs consist of capitalized costs previously carried under “Deferred mine exploration costs”, which were transferred to property and equipment upon start of commercial operations. Mining rights are expenditures for the acquisition of property rights that are capitalized. The net carrying amount of mine and mining properties is depleted using unit-of-production method based on the estimated economically recoverable reserves of the mine concerned or are written-off if the property is abandoned. Property and equipment, except for land, are depereciated, amortized and depleted in the following month from its availability for use and after the risks and rewards are transferred to the Company, or, in case of mine and mining properties, from start of commercial operations upon extraction of ore reserves. Depreciation, amortization and depletion ceases when the assets are fully depreciated, amortized or depleted, or at the earlier of the date that the item is classified as held for sale (or included in the disposal group that is classified as held for sale) in accordance with PFRS 5, Noncurrent Assets Held for Sale and Discontinued Operations, and the date the item is derecognized. The estimated useful lives and depreciation, amortization and depletion methods are reviewed at each end of the reporting period to ensure that the period and methods of depreciation, amortization and depletion are consistent with the expected pattern of economic benefits from items of property and equipment. *SGVMC409311

- 20. - 11 - An item of property and equipment is derecognized upon disposal or when no future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in the statement of comprehensive income in the year the asset is derecognized. Construction in-progress is stated at cost. This includes the cost of construction and other direct costs. Construction in-progress is not depreciated until completed and put into operational or available for use, whichever comes earlier. Deferred Mine Exploration Costs Expenditures for mine exploration work prior to drilling are charged to operations. When it has been established that a mineral deposit is commercially mineable and a decision has been made to formulate a mining plan (which occurs upon completion of a positive economic analysis of the mineral deposit), the costs subsequently incurred to develop a mine on the property prior to the start of mining operations are capitalized. Upon the start of commercial operations, such costs are transferred to mine and mining properties under “Property and equipment”. Capitalized amounts may be written down if future cash flows, including potential sales proceeds related to the property, are projected to be less than the carrying value of the property. If no mineable ore body is discovered, capitalized acquisition costs are expensed in the period in which it is determined that the mineral property has no future economic value. Costs incurred during the start-up phase of a mine are expensed as incurred. Ongoing mining expenditures on producing properties are charged against earnings as incurred. Major development expenditures incurred to expose the ore, increase production or extend the life of an existing mine are capitalized. Impairment of Non-financial Assets Inventories The Company determines the NRV of inventories at each end of the reporting period. If the cost of the inventories exceeds its NRV, the asset is written down to its NRV and impairment loss is recognized in the statement of comprehensive income in the year the impairment is incurred. In case the NRV of the inventories increased subsequently, the NRV will increase carrying amounts of inventories but only to the extent of their original acquisition costs. Property and Equipment Property and equipment, except land, are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. If any such indication exists and where the carrying amount of an asset exceeds its recoverable amount, the asset or cash-generating unit (CGU) is written down to its recoverable amount. The estimated recoverable amount is the higher of an asset’s or CGU’s fair value less cost to sell and value in use and is determined for an individual asset, unless the asset does not generate cash inflows that are largely independent of those from other assets or groups of assets, in which case the asset is tested as part of a large CGU. The fair value less cost to sell is the amount obtainable from the sale of an asset in an arm’s-length transaction less the costs of disposal while value in use is the present value, using a pre-tax discount rate, of estimated future cash flows expected to arise from the continuing use of an asset and from its disposal at the end of its useful life. Impairment losses are recognized in the statement of comprehensive income. *SGVMC409311

- 21. - 12 - Recovery of impairment losses recognized in prior periods is recorded when there is an indication that the impairment losses recognized for the asset no longer exist or have decreased. The recovery is recorded in the statement of comprehensive income. However, the increased carrying amount of an asset due to recovery of an impairment loss is recognized to the extent it does not exceed the carrying amount that would have been determined (net of depletion, depreciation and amortization) had no impairment loss been recognized for that asset in prior periods. Deferred Mine Exploration Costs An impairment review is performed, either individually or at the CGU level, when there are indicators that the carrying amount of the assets may exceed their recoverable amounts. To the extent that this occurs, the excess is fully provided against, in the financial period in which this is determined. Exploration assets are reassessed on a regular basis and these costs are carried forward provided that at least one of the following conditions is met: · such costs are expected to be recouped in full through successful development and exploration of the area of interest or alternatively, by its sale; or · exploration and evaluation activities in the area of interest have not yet reached a stage which permits a reasonable assessment of the existence or otherwise of economically recoverable reserves, and active and significant operations in relation to the area are continuing, or planned for the future. Provisions General Provisions are recognized when the Company has a present obligation (legal or constructive) as a result of a past event, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation. Provisions are reviewed at each end of the reporting period and adjusted to reflect the current and best estimate. When the Company expects some or all of the provisions to be reimbursed, the reimbursement is recognized as a separate asset but only when reimbursement is virtually certain. The expense relating to any provision is presented in the statement of comprehensive income, net of any reimbursement. If the effect of the time value of money is material, provisions are made by discounting the expected future cash flows at a pre-tax rate that reflects current market assessment of the time value of money and, where appropriate, the risks specific to the liability. Where discounting is used, the increase in the provision due to the passage of time is recognized as an accretion expense. Provision for Mine Rehabilitation and Decommissioning The Company records the present value of estimated costs of legal and constructive obligations required to restore operating locations in the period in which the obligation is incurred. The nature of these restoration activities includes dismantling and removing structures, rehabilitating mines and tailings dams, dismantling operating facilities, closure of waste sites, and restoration, reclamation and re-vegetation of affected areas. The obligation generally arises when the asset is installed or the ground/environment is disturbed at the production location. When the liability is initially recognized, the present value of the estimated cost is capitalized by increasing the carrying amount of the related mining assets. Over time, the discounted liability is increased for the change in present value based on the discount rates that reflect current market assessments and the risks specific to the liability. The periodic unwinding of the discount is recognized in the *SGVMC409311

- 22. - 13 - statement of comprehensive income under “Finance costs”. Additional disturbances or changes in rehabilitation costs will be recognize as additions or charges to the corresponding assets and provision for mine rehabilitation and decommissioning, respectively, when they occur. The liability is reviewed on an annual basis for changes to obligations or legislation or discount rates that affect change in cost estimates or life of operations. The cost of the related asset is adjusted for changes in the liability resulting from changes in the estimated cash flows or discount rate, and the adjusted cost of the asset is depleted prospectively. When rehabilitation is conducted progressively over the life of the operation, rather than at the time of closure, liability is made for the estimated outstanding continuous rehabilitation work at each end of the reporting period and the cost is charged to the statement of comprehensive income. The ultimate cost of mine rehabilitation is uncertain and cost estimates can vary in response to many factors including changes to the relevant legal requirements, the emergence of new restoration techniques or experience. The expected timing of expenditure can also change, for example in response to changes in ore reserves or production rates. As a result, there could be significant adjustments to the provision for mine rehabilitation and decommissioning, which would affect future financial results. MRF committed for use in satisfying environmental obligations are included within “Other noncurrent assets” in the statement of financial position. Related Party Relationships and Transactions Related party relationship exists when one party has the ability to control, directly, or indirectly through one or more intermediaries, the other party or exercise significant influence over the other party in making financial and operating decisions. Such relationship also exists between and/or among entities, which are under common control with the reporting enterprises and its key management personnel, directors, or its shareholders. In considering each related party relationship, attention is directed to the substance of the relationship, and not merely the legal form. Foreign Currency Transactions Transactions in foreign currencies are initially recorded in the functional currency rate ruling at the date of the transaction. Outstanding monetary assets and liabilities denominated in foreign currencies are restated using the closing rate of exchange ruling at the end of the reporting period. Nonmonetary items that are measured in terms of historical cost in foreign currency are translated using the exchange rates as at the dates of the initial transactions. Nonmonetary items measured at fair value in a foreign currency are restated using exchange rates at the date when the fair value was determined. All differences are taken to the statement of comprehensive income. Capital Stock Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options are shown in equity as a deduction from proceeds. The excess of proceeds from issuance of shares over the par value of the shares are credited to additional paid-in capital. *SGVMC409311

- 23. - 14 - Retained Earnings (Deficit) Retained earnings (deficit) are the cumulative portion of annual earnings or losses as stated in the statement of comprehensive income less dividends declared, if any. Dividends are recognized as a liability and deducted from retained earnings when they are approved by the stockholders of the Company. Dividends for the period that are approved after the end of the reporting period are dealt with as an event after the end of the reporting period. Revenue Recognition Revenue is recognized to the extent that it is probable that the economic benefits will flow to the Company and the revenue can be reliably measured, regardless of when payments are being made. Revenue is measured at the fair value of the consideration received or receivable, taking into account contractually defined terms of payment. The following specific recognition criteria must also be met before revenue is recognized: Sale of Beneficiated Nickel Ore Revenue is recognized when the significant risks and rewards of ownership of the goods have passed to the buyer, which coincides with the loading of the ores onto the buyer’s vessel. Under the terms of the arrangements with customers, the Company bills the remaining 10% of the ores shipped based on the assay tests agreed by both the Company and the customers. Where the assay tests are not yet available as at the end of the reporting period, the Company accrues for the remaining 10% of the revenue based on the amount of the initial billing made. HSEC Premium Revenue is recognized when the significant risks and rewards of ownership of the goods haved passed to Queensland Nickel Pty. Ltd. (QNPL). Despatch Despatch pertains to the income earned when shipment is loaded ahead of the allowable laytime. Revenue is recognized upon preparation of final invoice. Interest Income Income recognized as interest accrues using the effective interest rate, that is, the rate that exactly discounts estimated future cash receipts through the expected life of the financial instrument to the net carrying amount of the financial asset. Costs and Expenses Costs and expenses are decreases in economic benefits during the year in the form of outflows or decrease of assets or incurrence of liabilities that result in decrease in retained earnings or increase in deficit. Costs and expenses are recognized in statement of comprehensive income in the year these are incurred. Cost of Sales Cost of sales is incurred in the normal course of business and is recognized when incurred. They comprise mainly of personnel cost, cost of outside services, depreciation, amortization and depletion and production overhead, which are provided in the period when the goods are delivered. *SGVMC409311

- 24. - 15 - Expenses Expenses consist of costs associated with the development and execution of marketing and promotion activities, excise taxes and royalties due to the government and indigenous people and expense incurred in the direction and general administration of day-to-day operations of the Company. These are generally recognized when the expense arises. Leases Determination of Whether an Arrangement Contains a Lease The determination of whether an arrangement is, or contains a lease is based on the substance of the arrangement and requires an assessment of whether the fulfillment of the arrangement is dependent on the use of a specific asset or assets and the arrangement conveys a right to use the asset. A reassessment is made after inception of the lease only if one of the following applies: (a) There is a change in contractual term, other than a renewal or an extension of the arrangement; (b) A renewal option is exercised or extension granted, unless the term of the renewal or extension was initially included in the lease term; (c) There is a change in the determination of whether fulfillment is dependent on a specified asset; or (d) There is a substantial change to the asset. When a reassessment is made, lease accounting shall commence or cease from the date when the change in circumstances gave rise to the reassessment for scenarios (a), (c) or (d) above, and at the date of renewal or extension period for scenario (b). Company as a Lesee Operating leases represent those leases under which substantially all risks and rewards of ownership of the leased assets remains with the lessors. Noncancellable operating lease payments are recognized as expense in the statement of comprehensive income on a straight-line basis over the lease term. Input VAT Input VAT represents VAT imposed on the Company by its suppliers and contractors for the acquisition of goods and services in accordance with Philippine tax laws and regulations. Input VAT representing claims for refund from the taxation authorities, if any, is recognized under current asset. Input VAT is stated at its estimated net realizable value. Income Taxes Current Income Tax Current income tax assets and liabilities for the current and prior periods are measured at the amount expected to be recovered from or paid to the taxation authorities. The tax rates and tax laws used to compute the amount are those that are enacted or substantively enacted as at the end of the reporting period. *SGVMC409311

- 25. - 16 - Deferred Income Tax Deferred income tax is provided using the liability method on temporary differences at the end of the reporting period between the tax bases of assets and liabilities and their carrying amounts for financial reporting purposes. Deferred income tax liabilities are recognized for all taxable temporary differences, except: · where the deferred income tax liability arises from the initial recognition of goodwill or of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting income nor taxable income or loss; and · in respect of taxable temporary differences associated with investments in subsidiaries, associates and interests in joint ventures, where the timing of the reversal of the temporary differences can be controlled and it is probable that the temporary differences will not reverse in the foreseeable future. Deferred income tax assets are recognized for all deductible temporary differences, carryforward benefits of unused tax credits and unused tax losses, to the extent that it is probable that sufficient future taxable income will be available against which the deductible temporary differences, and the carryforward of unused tax credits and unused tax losses can be utilized except: · where the deferred income tax asset relating to the deductible temporary difference arises from the initial recognition of an asset or liability in a transaction that is not a business combination and, at the time of the transaction, affects neither the accounting income nor taxable income or loss; and · in respect of deductible temporary differences associated with investments in subsidiaries, associates and interests in joint ventures, deferred income tax assets are recognized only to the extent that it is probable that the temporary differences will reverse in the foreseeable future and sufficient future taxable income will be available against which the temporary differences can be utilized. The carrying amount of deferred income tax assets is reviewed at each end of the reporting period and reduced to the extent that it is no longer probable that sufficient future taxable income will be available to allow all or part of the deferred income tax asset to be utilized. Unrecognized deferred income tax assets are reassessed at each end of the reporting period and are recognized to the extent that it has become probable that sufficient future taxable income will allow the deferred income tax asset to be recovered. Deferred income tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled, based on tax rates (and tax laws) that have been enacted or substantively enacted at the end of reporting period. Deferred income tax assets and deferred income tax liabilities are offset, if a legally enforceable right exists to offset current income tax assets against current income tax liabilities and the deferred income taxes relate to the same taxable entity and the same taxation authority. *SGVMC409311

- 26. - 17 - Contingencies Contingent liabilities are not recognized in the financial statements. These are disclosed unless the possibility of an outflow of resources embodying economic benefits is remote. Contingent assets are not recognized in the financial statements but are disclosed when an inflow of economic benefits is probable. Events After the End of the Reporting Period Post year-end events that provide additional information about the Company’s position at the end of the reporting period (adjusting events) are reflected in the financial statements. Post year-end events that are not adjusting events are disclosed when material. 3. Significant Accounting Judgments, Estimates and Assumptions The preparation of the financial statements in compliance with PFRS requires the Company to make judgments, estimates and assumptions that affect the reported amounts of assets, liabilities, income and expenses and disclosure of contingent assets and contingent liabilities. Future events may occur which will cause the assumptions used in arriving at the estimates to change. The effects of any change in estimates are reflected in the financial statements as they become reasonably determinable. Judgments, estimates and assumptions are continually evaluated and are based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. However, actual outcome can differ from these estimates. Judgments In the process of applying the Company’s accounting policies, management has made the following judgments, apart from those involving estimations, which has the most significant effect on the amounts recognized in the financial statements: Determining Functional Currency Based on the economic substance of the underlying circumstances relevant to the Company, the functional currency of the Company has been determined to be the Philippine peso. The Philippine peso is the currency of the primary economic environment in which the Company operates. It is the currency that mainly influences labor, material and other costs of providing goods, and in which receipts from operating activities are generally retained. Classifying Financial Instruments The Company classifies a financial instrument, or its component parts, on initial recognition as a financial asset, a financial liability or an equity instrument in accordance with the substance of the contractual arrangement and the definitions of a financial asset, a financial liability or an equity instrument. The substance of a financial instrument, rather than its legal form, governs its classification in the statement of financial position. Operating Lease Commitments - Company as a Lessee The Company has entered into commercial property lease for its administrative office space and other property leases. The Company has determined that it does not retain all the significant risks and rewards of ownership of these properties which are leased on operating leases. *SGVMC409311

- 27. - 18 - Assessing Production Start Date The Company assesses the stage of each mine development project to determine when a mine moves into the production stage. The criteria used to assess the start date of a mine are determined based on the unique nature of each mine development project. The Company considers various relevant criteria to assess when the mine is substantially complete, ready for its intended use and moves into the production phase. Some of the criteria include, but are not limited to the following: · the level of capital expenditure compared to construction cost estimates; · completion of a reasonable period of testing of the property and equipment; · ability to produce ore in saleable form; and · ability to sustain ongoing production of ore. When a mine development project moves into the production stage, the capitalization of certain mine construction costs ceases and costs are either regarded as inventory or expensed, except for capitalizable costs related to mining asset additions or improvements, underground mine development or mineable reserve development. It is also at this point that depreciation or depletion commences. Estimates and Assumptions The key estimates and assumptions concerning the future and other key sources of estimation uncertainty at the end of the reporting period, that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below. Estimating Allowance for Impairment Losses on Trade and Other Receivables The Company maintains allowance for impairment losses at a level considered adequate to provide for potential uncollectible receivables. The level of this allowance is evaluated by management on the basis of the factors that affect the collectibility of the accounts. These factors include, but are not limited to, the Company’s relationship with its customer, customer’s current credit status and other known market factors. The Company reviews the age and status of trade and other receivables and identifies accounts that are to be provided with allowance either individually or collectively. The amount and timing of recorded expenses for any period would differ if the Company made different judgment or utilized different estimates. An increase in the Company’s allowance for impairment losses will increase the Company’s recorded expenses and decrease current assets. As at December 31, 2010 and 2009, the carrying value of trade and other receivables amounted to P7,531,094 and =11,752,404, net of allowance for impairment losses = P which amounted to P11,507,364 and P13,489,151, respectively (see Note 5). = = Estimating Beneficiated Nickel Ore Reserves Ore reserves are estimates of the amount of ore that can be economically and legally extracted from the Company’s mining properties. The Company estimates its ore reserves based on information compiled by appropriately qualified persons relating to the geological data on the size, depth and shape of the ore body, and require complex geological judgment to interpret the data. The estimation of recoverable reserves is based upon factors such as estimates of foreign exchange rates, commodity prices, future capital requirements, and production costs along with geological assumptions and judgment made in estimating the size and grade of the ore body. Changes in the *SGVMC409311

- 28. - 19 - reserve estimates may impact upon the carrying value of deferred mine exploration costs, property and equipment, provision for mine rehabilitation and decommissioning, recognition of deferred income tax assets, and depreciation and depletion charges. Estimating Allowance for Inventory Losses The Company maintains allowance for inventory losses at a level considered adequate to reflect the excess of cost of inventories over its NRV. NRV of inventories are assessed regularly based on prevailing estimated selling prices of inventory less the corresponding estimated costs necessary to make the sale. The carrying values of inventories amounted to P105,675,377 and = = P104,203,325, net of allowance for inventory losses amounting to P2,231,556, as at = December 31, 2010 and 2009, respectively (see Note 6). Estimating Useful Lives of Property and Equipment The Company estimates the useful lives of property and equipment, except land, based on the period over which the assets are expected to be available for use. The estimated useful lives of property and equipment are reviewed periodically and are updated if expectations differ from previous estimates due to physical wear and tear, technical or commercial obsolescence and legal or other limits on the use of the assets. In addition, estimation of the useful lives of property and equipment is based on collective assessment of industry practice, internal technical evaluation and experience with similar assets. It is possible, however, that future results of operations could be materially affected by changes in estimates brought about by changes in factors mentioned above. The amounts and timing of recorded expenses for any period would be affected by changes in these factors and circumstances. There were no changes in the useful lives of the property and equipment during the year. The aggregate net book values of property and equipment, excluding land, amounted to =627,701,090 and =684,722,985 as at December 31, 2010 and 2009, P P respectively (see Note 8). Depreciation, amortization and depletion recognized in 2010 and 2009 amounted to =56,323,955 and =54,325,231, respectively (see Notes 8 and 13). P P Estimating Allowance for Impairment on Property and Equipment The Company assesses impairment on property and equipment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. The factors that the Company considers important which could trigger an impairment review include the following: · significant underperformance relative to expected historical or projected future operating results; · significant changes in the manner of use of the acquired assets or the strategy for overall business; and · significant negative industry or economic trends. In determining the present value of estimated future cash flows expected to be generated from the continued use of the assets, the Company is required to make estimates and assumptions that can materially affect the financial statements. These assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss would be recognized whenever evidence exists that the carrying value is not recoverable. For purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash *SGVMC409311

- 29. - 20 - flows. As at December 31, 2010 and 2009, the Company has not recognized impairment losses on its property and equipment. The carrying values of property and equipment amounted to = P628,230,990 and =685,252,885 as at December 31, 2010 and 2009, respectively (see Note 8). P Estimating the Recoverability of Deferred Mine Exploration Costs The application of the Company’s accounting policy for deferred mine exploration costs requires judgment and estimates in determining whether it is likely that the future economic benefits are certain, which may be based on assumptions about future events or circumstances. Estimates and assumptions may change if new information becomes available. If, after mine explorations costs are capitalized, information becomes available suggesting that the recovery of expenditure is unlikely, the amount capitalized is written-off in the statement of comprehensive income in the period when the new information becomes available. The Company reviews the carrying values of its mineral property interests whenever events or changes in circumstances indicate that their carrying values may exceed their estimated net recoverable amounts. An impairment loss is recognized when the carrying values of these assets are not recoverable and exceeds their fair value. As at December 31, 2010 and 2009, there was no impairment noted on the Company’s deferred mine exploration costs. Deferred mine exploration costs amounted to P47,023,879 and P18,442,409 as at December 31, 2010 and 2009, = = respectively (see Note 9). Estimating Allowance for Impairment Losses on Non-financial Other Current Assets The Company provides allowance for impairment losses on non-financial other current assets when they can no longer be realized. The amounts and timing of recorded expenses for any period would differ if the Company made different judgments or utilized different estimates. An increase in allowance for impairment losses would increase recorded expenses and decrease other current assets. There is no allowance for impairment losses on the Company’s non-financial other current assets as at December 31, 2010 and 2009 as management has noted no indicators of impairment. The carrying values of non-financial other current assets amounted to P54,430,783 and P53,772,489 as = = at December 31, 2010 and 2009, respectively (see Note 7). Estimating Provision for Mine Rehabilitation and Decommissioning The Company assesses its provision for mine rehabilitation and decommissioning annually. Significant estimates and assumptions are made in determining the provision for mine rehabilitation as there are numerous factors that will affect the provision. These factors include estimates of the extent and costs of rehabilitation activities, technological changes, regulatory changes, cost increases, and changes in discount rates. Those uncertainties may result in future actual expenditure differing from the amounts currently provided. The provision at end of the reporting period represents management’s best estimate of the present value of the future rehabilitation costs required. Changes to estimated future costs are recognized in the statement of financial position by adjusting the mine and mining properties and provision for mine rehabilitation and decommissioning. Provision for mine rehabilitation and decommissioning amounted to =19,128,663 and =17,958,150 as at December 31, 2010 and 2009, respectively P P (see Note 11). *SGVMC409311

- 30. - 21 - Estimating the Realizability of Deferred Income Tax Assets The Company reviews the carrying amounts of deferred income tax assets at each end of the reporting period and reduces deferred income tax assets to the extent that it is probable that taxable income will be available against which these can be utilized. Significant management judgment is required to determine the amount of deferred income tax assets that can be recognized, based upon the likely timing and level of future taxable income together with future tax planning strategies. The Company recognized deferred income tax assets on the provision for mine rehabilitation and decommissioning costs amounting to P1,597,870 and P1,246,716 as at December 31, 2010 and = = 2009, respectively. The Company has other temporary differences such as allowance for impairment losses on trade and other receivables, allowance for inventory losses and accrued rent for which no deferred income tax assets have been recognized because management believes that the carryforward benefits would not be realized prior to its expiration (see Note 20). 4. Cash and Cash Equivalents 2010 2009 Cash with banks P14,257,447 = = P30,843,827 Cash on hand 338,993 287,006 Short-term cash investments – 20,098,454 P14,596,440 = = P51,229,287 Cash with banks earn interest at the respective bank deposit rates. Short-term cash investments are made for varying periods of up to three (3) months depending on the immediate cash requirements of the Company, and earn interest at the respective short-term cash investments rates. In 2010 and 2009, the Company earned interest from its cash with banks and short-term cash investments amounting to =115,313 and P134,136, respectively (see Note 22). P = 5. Trade and Other Receivables 2010 2009 Trade P11,503,164 = = P12,122,404 Advances to related parties (see Note 19) 6,602,632 10,417,753 Advances to officers and employees 486,880 1,585,153 Others 445,782 1,116,245 19,038,458 25,241,555 Less allowance for impairment losses (11,507,364) (13,489,151) P7,531,094 = = P11,752,404 The following are the terms and conditions of the above financial assets: · Trade receivables are noninterest-bearing and are normally settled on 15 to 30 days’ terms. · Advances to related parties and other receivables are noninterest-bearing and have an average term of 30 to 60 days. *SGVMC409311

- 31. - 22 - · Advances to officers and employees are noninterest-bearing and are subject to liquidation within 30 days, or if not liquidated within 30 days, this will be automatically deducted to officers’ and employees’ salary. Movement of allowance for impairment losses as at December 31, 2010 and 2009 follows: Advances to officers and 2010 Trade employees Total Balances at beginning of year P12,122,404 = P1,366,747 = P13,489,151 = Provision (see Note 13) – 770,153 770,153 Write-off – (2,132,700) (2,132,700) Exchange rate adjustment (619,240) – (619,240) Balances at end of year P11,503,164 = P4,200 = P11,507,364 = Advances to officers and 2009 Trade employees Total Balances at beginning of year = P12,459,575 = P1,366,747 = P13,826,322 Exchange rate adjustment (337,171) – (337,171) Balances at end of year = P12,122,404 = P1,366,747 = P13,489,151 As at December 31, 2010 and 2009, trade and other receivables amounting to =12,435,826 and P = P14,823,802, respectively, were subjected to specific impairment assessment. Based on the assessment done, the Company recognized allowance for impairment losses amounting to = P11,507,364 and =13,489,151, as at December 31, 2010 and 2009, respectively, covering those P receivables considered as individually impaired. With the foregoing level of allowance for impairment losses, management believes that the Company has sufficient allowance to cover any losses that the Company may incur from the noncollection or nonrealization of its trade and other receivables. 6. Inventories 2010 2009 Beneficiated nickel ore - at cost P103,502,330 = = P103,502,330 Fuel - at NRV 3,041,275 2,932,551 Supplies - at cost 1,363,328 – 107,906,933 106,434,881 Less allowance for inventory losses (2,231,556) (2,231,556) P105,675,377 = = P104,203,325 The allowance for inventory losses pertains to fuel inventory as at December 31, 2010 and 2009. *SGVMC409311

- 32. - 23 - 7. Other Current Assets 2010 2009 Input VAT P52,345,766 = = P52,043,011 Prepaid insurance 1,039,607 1,109,828 Prepaid rent 788,760 364,000 Prepaid income tax 195,650 195,650 Deposit with suppliers 60,000 60,000 Others 1,000 – P54,430,783 = = P53,772,489 Prepaid rent represents advance rental payments to the lessors of the properties leased by the Company (see Note 21). 8. Property and Equipment 2010 Mine and Mining Leasehold Laboratory and Transportation Office Construction Land Properties Improvements Other Equipment Equipment Equipment In-progress Total Cost: Balances at beginning of year = P529,900 P348,371,153 = = P249,493,362 = P190,633,692 = P24,329,970 = P25,402,307 = P4,441,502 P843,201,886 = Additions – – – – – 229,441 – 229,441 Disposals – – – – (1,464,286) – – (1,464,286) Reclassification – – 4,441,502 – – – (4,441,502) – Balances at end of year 529,900 348,371,153 253,934,864 190,633,692 22,865,684 25,631,748 – 841,967,041 Accumulated depreciation, amortization and depletion: Balances at beginning of year – 23,724,699 53,100,104 56,589,341 11,717,870 12,816,987 – 157,949,001 Depreciation, amortization and depletion (see Note 13) – – 23,901,967 22,913,300 4,646,351 4,862,337 – 56,323,955 Disposals – – – – (536,905) – – (536,905) Balances at end of year – 23,724,699 77,002,071 79,502,641 15,827,316 17,679,324 – 213,736,051 Net book values = P529,900 P324,646,454 = = P176,932,793 = P111,131,051 = P7,038,368 = P7,952,424 P = = – P628,230,990 2009 Mine and Mining Leasehold Laboratory and Transportation Office Construction Land Properties Improvements Other Equipment Equipment Equipment In-progress Total Cost: Balances at beginning of year = P529,900 P348,371,153 = = P236,132,570 = P183,518,312 = P25,507,649 = P25,085,361 = P17,629,853 = P836,774,798 Additions – – – 7,115,380 – 316,946 172,441 7,604,767 Disposals – – – – (1,177,679) – – (1,177,679) Reclassification – – 13,360,792 – – – (13,360,792) – Balances at end of year 529,900 348,371,153 249,493,362 190,633,692 24,329,970 25,402,307 4,441,502 843,201,886 Accumulated depreciation, amortization and depletion: Balances at beginning of year – 23,724,699 30,534,217 34,862,864 7,087,412 7,758,068 – 103,967,260 Depreciation, amortization and depletion (see Note 13) – – 22,565,887 21,726,477 4,973,948 5,058,919 – 54,325,231 Disposals – – – – (343,490) – – (343,490) Balances at end of year – 23,724,699 53,100,104 56,589,341 11,717,870 12,816,987 – 157,949,001 Net book values P529,900 P324,646,454 = = P196,393,258 = P134,044,351 = P12,612,100 = P12,585,320 = P4,441,502 = P685,252,885 = As at December 31, 2010 and 2009, mining rights, included in the mine and mining properties, amounting to P76,128,171, net of accumulated depletion of =5,828,129, pertain to the acquisition = P costs of property rights on the Berong Project (see Note 24). Fully depreciated property and equipment as at December 31, 2010 and 2009 amounting to = P1,428,511 and =56,300, respectively, are retained in the Company’s records until they are P disposed. No further depreciation and amortization are charged to current operations for these items. *SGVMC409311