More than Just Lines on a Map: Best Practices for U.S Bike Routes

Where Is Construction Headed Globally In 2011

1. Where Is Construction Headed Globally

In 2011?

This was my answer to a very similar

question in a LinkedIn group.

Leaving politics out of it and since the world financial collapse was brought on by the slow,

thirty year bipartisan deregulation of our financial institutions: we do not see where growth

will come from in 2011. The bottom line is our industry has been changed forever by the

correction which occurred in the fall of 2008 caused by the overheated residential and

commercial construction sectors. This correction started in early 2007 with the subprime loan

crisis which first affected the housing market and the rest we are still feeling. The upside in

2011 should be that the bleeding will start to subside and the first sign of this is that housing

seems to have bottomed out: “It is not showing any signs of growth, however housing starts

have been hovering around five hundred thousand units per month for most of 2010, however

at its height in 2006 we averaged 2.3 million starts per month. “ This said there is still a

considerable amount of toxic paper out there in the office, lodging and retail sector which is

keeping the banks from lending which will lead to more bank failures in the coming year. It

really doesn’t matter because there is a huge glut of vacant commercial and retail space.

Recently the Fed stated that unemployment will likely remain above nine percent through

2011, this combined with home foreclosures and the anemic sales of new and existing homes

has greatly diminished public revenues putting most states in a monetary crisis. These state

revenue short falls will make state financed construction projects impossible to fund; the

tragedy here is that elementary, middle and high school construction makeup virtually fifty

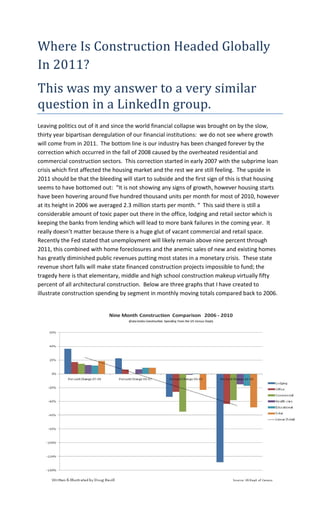

percent of all architectural construction. Below are three graphs that I have created to

illustrate construction spending by segment in monthly moving totals compared back to 2006.

2.

3. Foreign opportunities: Without getting specific, areas in the Pacific Rim especially China are

going to grow in varying markets: For the past ten years China has experienced an explosion in

high rise and other residential construction which has led to an increasing need to beef up

transportation and other miscellaneous infrastructure, we do expect this to continue; it is also

our feeling however that China is sitting on a financial bubble due to the drastic undervaluation

of it currency. Except for the foreign currency issue, the same can be said for India as it

continues to put a stake in the ground as the world’s new emerging economy. There is a

considerable amount of high rise residential construction, mixed with institutional and

infrastructure expansion, as its new middle class emerges. As it relates to the Middle East,

specifically Qatar, Saudi Arabia, Egypt and the Emirates; there will continue to be a growing

number of institutional, multi residential, commercial and infrastructural projects; the only

exception would be Dubai. We have all seen the news regarding the European economy; with

exception of Germany they are experiencing to some degree similar economic pressures as the

US. The growing austerity programs in the UE and Great Britain related to large domestic debt

will continue to stifle institutional construction and hamper overall economic growth. Please

free to contact me with any questions or comments.

(Written & Illustrated by Doug Bevill; Construction Economics & Strategies)

dbevill@con-econ.com

www.con-econ.com

Phone: 314-422-3177

Dated: 12/30/2010