1. EQUITY RESEARCH

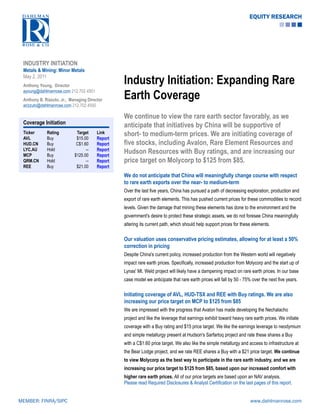

INDUSTRY INITIATION

Metals & Mining: Minor Metals

May 2, 2011

Anthony Young, Director

Industry Initiation: Expanding Rare

Earth Coverage

ayoung@dahlmanrose.com 212.702.4501

Anthony B. Rizzuto, Jr., Managing Director

arizzuto@dahlmanrose.com 212.702.4500

We continue to view the rare earth sector favorably, as we

Coverage Initiation

anticipate that initiatives by China will be supportive of

Ticker

AVL

Rating

Buy

Target

$15.00

Link

Report

short- to medium-term prices. We are initiating coverage of

HUD.CN Buy C$1.60 Report five stocks, including Avalon, Rare Element Resources and

LYC.AU

MCP

Hold

Buy

--

$125.00

Report

Report

Hudson Resources with Buy ratings, and are increasing our

QRM.CN Hold -- Report price target on Molycorp to $125 from $85.

REE Buy $21.00 Report

We do not anticipate that China will meaningfully change course with respect

to rare earth exports over the near- to medium-term

Over the last five years, China has pursued a path of decreasing exploration, production and

export of rare earth elements. This has pushed current prices for these commodities to record

levels. Given the damage that mining these elements has done to the environment and the

government's desire to protect these strategic assets, we do not foresee China meaningfully

altering its current path, which should help support prices for these elements.

Our valuation uses conservative pricing estimates, allowing for at least a 50%

correction in pricing

Despite China's current policy, increased production from the Western world will negatively

impact rare earth prices. Specifically, increased production from Molycorp and the start up of

Lynas' Mt. Weld project will likely have a dampening impact on rare earth prices. In our base

case model we anticipate that rare earth prices will fall by 50 - 75% over the next five years.

Initiating coverage of AVL, HUD-TSX and REE with Buy ratings. We are also

increasing our price target on MCP to $125 from $85

We are impressed with the progress that Avalon has made developing the Nechalacho

project and like the leverage that earnings exhibit toward heavy rare earth prices. We initiate

coverage with a Buy rating and $15 price target. We like the earnings leverage to neodymium

and simple metallurgy present at Hudson's Sarfartoq project and rate these shares a Buy

with a C$1.60 price target. We also like the simple metallurgy and access to infrastructure at

the Bear Lodge project, and we rate REE shares a Buy with a $21 price target. We continue

to view Molycorp as the best way to participate in the rare earth industry, and we are

increasing our price target to $125 from $85, based upon our increased comfort with

higher rare earth prices. All of our price targets are based upon an NAV analysis.

Please read Required Disclosures & Analyst Certification on the last pages of this report.

MEMBER: FINRA/SIPC www.dahlmanrose.com

2. DAHLMAN ROSE & CO. EQUITY RESEARCH

Executive Summary We continue to view the rare earth sector favorably. Over the near-term, we expect continued

upward pressure on the prices for the underlying metals as we do not expect that China,

which essentially controls supply, will meaningfully alter its course of decreasing exploration,

production and exports. Over the medium-term, we expect prices to decrease as Molycorp

and Lynas increase supply. From a supply/demand perspective, certain metals will see a

balanced market by the 2014 timeframe, with a slight surplus possible, but we believe that

metals used in magnets will remain in deficit for some time.

Despite soaring prices, demand for these metals remains relatively well supported, but we

believe it is possible that we are quickly reaching a "pain threshold" where further price

increases may lead to meaningful demand destruction. Demand from electronics, windmills

and electric automobiles should experience meaningful growth over the medium- to long-

term as manufacturers seek to miniaturize applications and maximize efficiency. In fact, it is

possible that increased supply and the possibility for lower prices over the long-term, may

spur development of new applications for these raw materials, which may cause demand to

exceed our expectations.

In our base case, we anticipate that prices will fall 50 - 75%, which may prove to be too

aggressive of a decrease. Despite the possibility of decreasing metal prices, we continue to

see meaningful upside in the equities.

We are initiating coverage of Avalon Rare Metals (AMEX: AVL) with a Buy rating and

a $15 price target. While the company has difficult metallurgy to work through, we like the

progress it has made attacking the project. Further, we like the leverage that the company

has to heavy rare earth metals, which have increased in price less than light rare earth metals

on a percentage basis, and therefore should see less of a contraction in price should the

broader rare earth sector see pricing decline.

We are initiating coverage of Rare Element Resources (AMEX: REE) with a Buy

rating and a $21 price target. We like the straightforward metallurgy that is present at the

company's Bear Lodge deposit and access to infrastructure that is present at this deposit. In

fact, we believe that these aspects make the company an attractive candidate to be acquired

by a producing rare earth company over the medium-term.

We are initiating coverage of Hudson Resources (TSX: HUD) with a Buy rating and

a C$1.60 price target. We like the leverage that the company has to neodymium, a rare

earth element that we anticipate will have the most robust demand profile of any metal in

the category. Further, we like the relatively straightforward metallurgy that is present at

the company's Sarfartoq deposit in Greenland and the expansion opportunities that are

available at this deposit. Given the relatively early stage of the project and the fact that it

is in Greenland, an area where not many large scale projects have been constructed, we

are applying an extremely high discount rate of 20%. We expect that this discount rate may

MEMBER: FINRA/SIPC 2 www.dahlmanrose.com

3. DAHLMAN ROSE & CO. EQUITY RESEARCH

move meaningfully lower as the company makes progress developing this asset, creating

substantial upside for the shares.

We are increasing our price target on Molycorp (NYSE: MCP) to $125 from $85 and

reiterating our Buy rating on the shares. We continue to view Molycorp as the best way

to participate in the near-term strength that we forecast in the rare earth market. The reason

for the increased price target is our comfort with rare earth prices and our belief that prices

will exceed our previous expectations. With construction well underway at the Mountain Pass

mine and the company having 50+ years of experience separating and processing rare earth

elements from this deposit, we believe that the company should be able to quickly ramp

production in 2012 when the construction is complete. Further, we like the company's low-

cost structure, and we believe that once production commences at this facility the company

will look to be a consolidator in the rare earth segment.

We are initiating coverage of Lynas (ASX: LYC) with a Hold rating. Management has

done an excellent job of shepherding the Mount Weld and Advanced Materials Plant projects

through the development stage toward production, but we remain concerned that the

company may face start-up issues as it looks to commence production in 3Q11. Over the

near-term, we are concerned that the shares will exhibit less leverage to rare earth prices and

more leverage to geopolitical negotiations.

We are initiating coverage of Quest Rare Minerals (TSX: QRM) with a Hold rating.

While we find the mix of rare earth elements that the company will be providing to the market

interesting, we believe that it will be some time before the project commences production.

Additionally, we are concerned with the difficult metallurgy present at the deposit. In order for

the company to enter production in the timeframe envisioned, it may be necessary for Quest

to license technology from another mining company, increasing the company's cost profile.

Exhibit 1: Coverage Universe Comp Sheet

As of 4/29/2011

Total Resource Market Cap /

Company Ticker Rating Target/NAV Price Currency Market Cap Base (mt REO)** Resource Base

Avalon Rare Metals Inc AVL Buy 15.00 9.09 USD 941,805,537 4,277,156 220

Hudson Resources Inc HUD-V Buy 1.60 1.11 CAD 93,906,000 212,838 441

Lynas Corporation Ltd LYC-AU Hold 2.85 2.09 AUD 3,462,818,590 1,415,668 2,446

Molycorp Inc MCP Buy 125.00 73.30 USD 6,032,639,111 1,015,938 5,938

Quest Rare Minerals Ltd QRM-V Hold 8.40 8.15 CAD 568,870,000 583,148 976

Rare Element Resources Ltd REE Buy 21.00 14.45 USD 673,370,000 549,301 1,226

**Total resource base includes measured, indicated, and inferred resources and is inclusive of any reserve estimates

Source: Company Reports, Dahlman Rose & Co. estimates

MEMBER: FINRA/SIPC 3 www.dahlmanrose.com

4. DAHLMAN ROSE & CO. EQUITY RESEARCH

China continues to dominate the rare Despite increased production from the West, we anticipate China will continue to dominate

earth sector the rare earth sector. China accounted for approximately 95% of rare earth element

production in 2010, and while its percentage of rare earth production is set to decline, the

country will continue to be the largest producer for the foreseeable future.

Exhibit 2: Global Rare Earth Production 2013 (151,000 metric tons)

India, 3% Recycling, 4%

Russia, 4%

Australia, 7%

US, 13%

China, 70%

Source: Dahlman Rose & Co. estimates

We believe that China continues to view rare earth metals as strategic assets and will

not waiver from its current path of decreasing exports, limiting exploration, and tightly

controlling production. In our opinion, China is pursuing this path in order to limit damage to

its environment and in an effort to lure high technology manufacturing to within its borders by

being able to supply lower-cost raw materials. Given that China will maintain its position as

the world's largest producer of rare earths, the internal Chinese price will be a key indicator

of the direction of global pricing, and we note that this price has been moving meaningfully

higher recently.

Exhibit 3: Chinese Rare Earth Export Quotas, Actual Exports and Western World Demand

70,000

60,000

50,000

metric tons

40,000

30,000

20,000

10,000

-

2004 2005 2006 2007 2008 2009 2010 2011e

Chinese Export Quota Chinese Exports Western World Demand

Source: Chinese Society of Rare Earths, Dahlman Rose & Co. estimates

MEMBER: FINRA/SIPC 4 www.dahlmanrose.com

5. DAHLMAN ROSE & CO. EQUITY RESEARCH

While we believe it is premature to forecast that China will eventually be an importer of

rare earth elements, certain Chinese agencies have been indicating that this is a distinct

possibility and that it might occur as soon as 2015. Additionally, steps by the Central

government to crack down on illegal mining appear to point toward concerns about the long-

term economic viability of Chinese deposits, unless rare earth prices are well above their

historical averages. Our belief stems from our observations of Chinese mining of other raw

materials such as iron ore and molybdenum, where illegal miners will attempt to "cherry-pick"

high grade areas, which damages the long-term viability of an entire deposit. Thus, a portion

of Chinese regulators enforcement initiatives appear to be focused on sustaining the long-

term economics of the country's assets.

Lower Prices on the Horizon? Rare earth prices have been surging higher since the 2Q09 timeframe, with prices increasing

by as much as 1000% for many classes of rare earths. We are uncertain that this price level

is sustainable over the medium- to long-term. In fact, in our base case valuation analyses we

anticipate that rare earth pricing will fall by 50 - 75%. While a decrease in rare earth prices will

have a short-term negative impact on the shares, we believe that many of the companies in

the sector can still produce tremendous earnings power in a lower price environment. Thus,

despite the likelihood of lower prices on the horizon, we continue to see meaningful upside in

the shares.

Exhibit 4: Rare Earth Relative Price Comparison

1800

1600

1400

1200

Relative Price (%)

1000

800

600

400

200

0

01 02 03 0 4 05 0 6 07 08 09 1 0

20 20 20 20 20 20 20 20 20 20

0 4/ 04/ 0 4/ 04/ 0 4/ 04/ 0 4/ 04/ 0 4/ 04/

Source: Metal-Pages, Dahlman Rose & Co. estimates

MEMBER: FINRA/SIPC 5 www.dahlmanrose.com

6. DAHLMAN ROSE & CO. EQUITY RESEARCH

Where do rare earth prices find While we believe that a correction is possible, we do not anticipate that prices will fall to levels

support? of three to five years ago, nor do we anticipate that prices will fall to the levels present at

the beginning of last year. We believe that the crackdown on rare earth production in China

will have a lasting impact on the global structure of rare earth prices. Therefore, we would

look to the Chinese price as a level where these metals will find substantial support. With

two exceptions, we set our long-term price deck near the current Chinese price. Demand for

lanthanum and yttrium will be will be well supported which should lead to pricing that exceeds

the current Chinese price.

Exhibit 5: Rare Earth Oxide Price Comparison ($/kg)

Element 1 Year Ago Chinese Domestic Prices DRCO Long Term Estimate Spot

Lanthanum 6 16 60 131

Cerium 5 23 30 131

Praseodymium 30 98 100 200

Neodymium 31 99 100 220

Dysprosium 193 498 500 690

Yttrium 11 32 75 158

Source: Metal-Pages, Dahlman Rose & Co. estimates

Supply / Demand From a supply/demand perspective, we anticipate that decreasing deficits will lead to lower

prices. While deficits are decreasing, we anticipate that it will be some time before the market

tips into a surplus, and therefore estimate a gradual decrease in price over many years.

Further, it is possible that market participants may exhibit more discipline, decreasing supply

in order to support pricing, than we currently forecast. If this were to come to pass, prices may

exceed our expectations.

Exhibit 6: Rare Earth Supply/Demand Estimates (metric tons)

Supply 2010 2011 2012 2013 2014 2015

Baotou Iron Ore 55,000 60,000 60,000 60,000 60,000 60,000

Sichuan 10,000 12,000 15,000 20,000 20,000 20,000

Ionic Clay 35,000 30,000 25,000 25,000 20,000 20,000

India 3,000 3,000 4,000 4,000 4,000 4,000

Russia 4,000 5,000 5,500 6,000 6,500 7,000

Mt. Weld - - 7,000 10,000 15,000 22,000

Mountain Pass 3,000 3,000 8,000 20,000 35,000 40,000

Recycling/Other 5,000 5,000 5,500 6,000 8,000 10,000

Total 115,000 118,000 130,000 151,000 168,500 183,000

Demand

Magnets 31,500 34,650 38,115 41,927 46,119 50,731

Battery Alloy 18,600 21,018 23,750 26,838 30,327 34,269

Mettallurgy ex batteries 11,700 11,817 11,935 12,055 12,175 12,297

Auto Catalytic Converters 9,000 9,540 10,112 10,719 11,362 12,044

Refinery Catalysts 21,300 22,152 23,038 23,960 24,918 25,915

Polishing Powder 14,000 14,700 15,435 16,207 17,017 17,868

Glass Additives 7,800 7,800 7,800 7,800 7,800 7,800

Phosphors 7,900 8,374 8,876 9,409 9,974 10,572

Other 5,700 5,700 5,800 5,800 5,900 5,900

Total 127,500 135,751 144,862 154,713 165,592 177,396

S/D Balance (12,500) (17,751) (14,862) (3,713) 2,908 5,604

Source: Dahlman Rose & Co. estimates

MEMBER: FINRA/SIPC 6 www.dahlmanrose.com

7. DAHLMAN ROSE & CO. EQUITY RESEARCH

Industry Overview The name “rare earths” is misleading. The term is used to represent 15 specific elements,

known as lanthanides, with some industry participants also including scandium and yttrium.

Some of these elements are actually quite plentiful in nature. Cerium, for example, is the 25th

most abundant element in the Earth's crust. Each of the elements share similar chemical

and physical properties. While some rare earths are relatively common, they are dispersed

in such a manner that makes it difficult to find deposits with high enough ore grades to

economically exploit. Very few large, high grade ore deposits have been discovered, and

it is this scarcity of economic projects that has driven rare earth prices substantially higher.

Greenfield exploration has increased in proportion to the move higher in rare earth prices, but

we continue to believe that it will take at least 12 - 15 years to commence production upon

the discovery of an economic rare earth ore body. (This development time line is not unique

to rare earth deposits; in fact, we are seeing this across the basic materials sector.) Once an

ore body has been discovered, there are several steps that must be taken to arrive at finished

rare earth oxides (REO) and rare earth alloys that can be consumed by end-users.

Rare Earth Extraction Mining

Open pit mining is well understood and utilized for numerous forms of base metals, bulk

materials and precious metals and is used more often when surface mineralization is high.

Mining can either be performed in an open pit or underground configuration, with open pit

mining being the more common in rare earth mining. In either configuration, ore is liberated

using explosives and then loaded onto large trucks or conveyor belts to be initially crushed,

typically by a primary crusher. The crushed ore is then transported to a mill where it is further

ground into fine grains.

Flotation

Material is often ground down to 50 micrometer particles (± 15 micrometers), de-slimed and

passed over magnets to remove impurities. This material is mixed with a reagent (this reagent

will vary with the chemical composition of the deposit) which will combine with the rare earth

mineral and cause the mineral to float when combined with water. The resulting slurry is then

pumped into rougher cells, where the minerals float to the top and form concentrate that is

skimmed off the solution.

Hydrometallurgy / Separation

A rare earth production company can be described as a chemical processing facility, with a

mine attached to it. As we described before, rare earth elements are relatively common in

the Earth's crust, but it is the hydrometallurgy/separation of these elements which is difficult

to achieve. In fact, with several rare earth projects planning on reaching tolling agreements

to process their concentrate, it is possible that hydrometallurgy/separation facilities may be

a bottleneck in achieving higher production in the 2015 - 2016 timeframe. The separation of

rare earths often involves the consumption of two different types of acids (hydrochloric and

sulfuric) along with placing the material under high temperature (up to 600 degrees C) and

pressure.

MEMBER: FINRA/SIPC 7 www.dahlmanrose.com

8. DAHLMAN ROSE & CO. EQUITY RESEARCH

Key Rare Earth Element Uses Rare Earth Magnets

Rare earth magnets, specifically neodymium-iron-boron magnets, are the strongest

permanent magnets known and are expected to be one of the primary drivers of rare earth

demand in the future. The strength of the magnetic field generated by these elements

allows much smaller rare earth magnets to be used, allowing for the miniaturization of many

applications. These magnets are used in everyday items like hard drives, audio speakers,

microphones and numerous consumer electronic applications, but it is the less common

uses that are gaining traction and will foster future demand. Turbines found in windmills are

shaping up to be a significant driver of demand for permanent magnets. It is estimated that

a three megawatt windmill would consume nearly 700 pounds of neodymium. Additionally,

hybrid and electric vehicles are shaping up to be significant drivers of demand for permanent

magnets. While the amount of magnets consumed per vehicle will vary upon the size, we

estimate that each vehicle may consume 3 - 5 kg of permanent magnets. The current push

toward energy efficiency and environmental protection will benefit both the hybrid car and

alternative energy industries, which bodes well for rare earth magnet demand, currently

estimated to represent 25% of rare earth demand.

Exhibit 7: Global Hybrid Vehicle Sales Growth (2007 - 2020)

Global Hybrid Vehicle Sales Growth

80

70

60

Sales (in millions)

50

40

30

20

10

-

2007

2008

2009

2010

2011e

2012e

2013e

2014e

2015e

2016e

2017e

2020e

Source: JD Power and Associates, Dahlman Rose & Co. estimates

Battery Alloys

Nickel-metal hydride batteries are found in hybrid-electric vehicles and utilize large amounts

of lanthanum (10 – 15 kg). These rechargeable batteries have two to three times the capacity

of similar sized nickel-cadmium batteries. While it is possible that lithium-based batteries may

MEMBER: FINRA/SIPC 8 www.dahlmanrose.com

9. DAHLMAN ROSE & CO. EQUITY RESEARCH

be a substitute over the long-term, we believe that lanthanum based NiMH batteries will be

the device of choice for the hybrid car industry over the near- to medium-term.

Phosphors

The phosphor market will continue to be an important area for rare earth elements. These

elements are used extensively in compact fluorescent lighting (CFL), and europium continues

to be an important element utilized in the television industry. Given energy conservation

initiatives that are occurring globally, we anticipate that CFL will continue to take market

share from incandescent bulbs, and therefore we expect above trend growth in the phosphor

market.

Catalysts

Rare earths play an important role in the manufacturing of automotive catalytic converters

and catalysts used in the cracking of crude petroleum at refineries. We anticipate strong

growth in the auto catalyst area, as we expect rare earth element based catalytic converters

to take market share from catalytic converters that consume larger amounts of platinum.

While we do not expect above trend growth in the fluid cracking catalysts consumed in the

refining industry, we do expect demand in this area to remain firm and to trend modestly

higher over the intermediate term.

Element Descriptions Light Rare Earths

Lanthanum

Lanthanum, one of the light rare earth elements, is also one of the most common,

representing roughly 20% of the rare earth content of global ore bodies. Lanthanum is used

primarily in the production of LaNiH (nickel-metal hydride) batteries, as a fluid cracking

catalyst, and as an additive to increase the refractive index of glass. The hybrid car market

presents a large demand opportunity, as a typical Toyota Prius hybrid requires between

10 and 15 kg of lanthanum. This amount may increase as Toyota seeks to increase fuel

efficiency. Currently, Toyota is selling over 16,000 hybrids a month, up over 60% from a

year ago. During this time, the price on lanthanum has increased from about $10/kg to over

$130/kg. While there is a threat of substitution from lithium batteries, we expect demand for

lanthanum to increase an average of 6% per year through 2015 and for the current supply

deficit to continue over the near-term.

Cerium

Cerium, representing about 40% of the rare earth content of source minerals and 0.046%

of the Earth’s crust by weight, is the most abundant of all the rare earth elements and is

considered a light element. Cerium is used mainly in catalytic converters in cars, polishing

powders for TVs, monitors, mirrors, silicon chips, and as an additive in glass to decrease

transmission of UV light. Since cerium is the most abundant of the REEs, it is also the first

one projected to be in a supply surplus, possibly by 2014. In response to this future supply

overhang, producers are developing new products to utilize cerium, most notably Molycorp’s

XSORBX product used for water treatment. Prices for cerium have steadily increased from

MEMBER: FINRA/SIPC 9 www.dahlmanrose.com

10. DAHLMAN ROSE & CO. EQUITY RESEARCH

the $7-$9/kg range from 2008 through mid-2010, to over $120/kg currently. We project annual

demand growth of 3% through 2015.

Neodymium

We expect neodymium demand growth to be among the strongest of the rare earths over the

medium-term. NdFeB magnets are among the strongest magnets known. These magnets are

used in many products such as microphones, loudspeakers, and computer hard disk drives.

We also expect increased demand from windmills and electric vehicles. Prices for neodymium

have risen more than tenfold from $17.50/kg in early 2009 to around $220/kg currently. We

anticipate annual demand growth of 12% through 2015, out pacing global GDP, due to the

increased usage and importance of rare earth magnets.

Praseodymium

Praseodymium is a light rare earth element that constitutes approximately 4-5% of the

rare earth content of ore bodies that have been identified globally. Its use in neodymium-

iron-boron magnets is expected to serve as a primary demand driver for the element going

forward, and its current supply deficit is not expected to abate. Current estimated demand

is roughly twice current supply, and we believe that inventories have reached critically low

levels. Praseodymium is also used to make high-strength alloys in the production of aircraft

engines and is used by the movie industry to make studio and projector lights. Prices for

praseodymium have increased drastically, from around $15/kg in 2009 to the $200/kg range

currently. Similar to neodymium, we anticipate annual growth of 12% through 2015 for

praseodymium.

Heavy Rare Earths

Dysprosium

Dysprosium is considered a heavy rare earth element and makes up approximately 1% of

the rare earth content of ore bodies globally. Dysprosium can be substituted for a portion

of neodymium in neodymium-iron-boron magnets in order to raise the magnet’s ability

to withstand high temperatures for use in hybrid electric motors, wind turbines, and hard

drives. Additionally, dysprosium oxide-nickel cement is used to make control rods for nuclear

reactors, due to the element's high thermal neutron absorption rate. The element is also used

to make lasers (when combined with vanadium) and high intensity lighting. Dysprosium is

currently in a supply deficit that should continue going forward due to the high demand of rare

earth magnets. Prices for dysprosium have steadily increased from roughly $100/kg in 2009

to $690/kg currently. We anticipate annual growth of 10% through 2015.

Europium

Europium is a heavy rare earth element that comprises about 0.5% of the rare earth content

of ore bodies globally. Europium is also used as a red phosphor in televisions and fluorescent

lights. When Molycorp's Mountain Pass mine initially opened, it was the supplier of europium

for the color red in virtually every TV in the world. Demand for europium is small compared

MEMBER: FINRA/SIPC 10 www.dahlmanrose.com

11. DAHLMAN ROSE & CO. EQUITY RESEARCH

to the other rare earth elements, but since it only makes up a small percentage of rare earth

content, it is in a slight supply deficit which is expected to persist. Prices for europium were in

the $400 - $500/kg range for most of 2008 and 2009 and have since risen to over $1,000/kg.

We anticipate a 2% annual growth rate for europium through 2015.

Yttrium

While not a rare earth element, it is sometimes found with these elements in ore bodies

and has chemical properties similar to rare earth elements. Yttrium is used as a phosphor

in compact fluorescent lights and sometimes combined with Europium to produce the color

red in television sets. Pricing for yttrium has ranged from a low of $10/kg in late 2009 to over

$150/kg currently. While we see improving demand for this element, the opportunity to recycle

is also robust; therefore, we see demand for this metal beyond recycled material increasing

by 3% annually.

Exhibit 8: Rare Element Breakdown

Source: Geology.com

MEMBER: FINRA/SIPC 11 www.dahlmanrose.com

12. DAHLMAN ROSE & CO. EQUITY RESEARCH

Exhibit 9: Composition of Ore Deposits

Element Symbol Hudson Lynas Molycorp REE Avalon Quest

Light Rare Earths

Cerium Ce 39% 45% 49% 47% 36% 27%

Lanthanum La 12% 25% 34% 31% 16% 13%

Neodymium Nd 33% 17% 12% 12% 18% 11%

Praseodymium Pr 7% 5% 4% 4% 5% 3%

Samarium Sm 5% 2% 1% 2% 4% 3%

Heavy Rare Earths

Dysprosium Dy 0% 1% 0% 0% 3% 4%

Erbium Er 0% 0% 0% 0% 1% 3%

Europium Eu 1% 1% 0% 1% 1% 0%

Gadolinium Gd 2% 2% 0% 1% 4% 3%

Holmium Ho 0% 0% 0% 0% 1% 1%

Lutetium Lu 0% 0% 0% 0% 0% 0%

Terbium Tb 0% 0% 0% 0% 1% 1%

Thulium Tm 0% 0% 0% 0% 0% 1%

Ytterbium Yb 0% 0% 0% 0% 1% 3%

Yttrium Y 0% 2% 0% 1% 12% 28%

Source: Dahlman Rose & Co. estimates

MEMBER: FINRA/SIPC 12 www.dahlmanrose.com

13. DAHLMAN ROSE & CO. EQUITY RESEARCH

Valuation Methodology & Investment Risks

Valuation Methodology

For companies with operating assets in the Metals & Mining space, we apply a multiple to our one-year forward EBITDA estimate to achieve our

year-end price targets. Our applied multiple is based on historical industry-wide and company specific multiples. For Metals & Mining companies

whose assets are primarily in pre-production, we apply an NAV analysis to future cash flows to achieve a one year forward price target.

Investment Risks

The global macro economy poses the biggest risk to the Metals & Mining industry as demand for metals and minerals is highly correlated to

economic growth. In particular, China is the world’s largest consumer of aluminum, coal, copper, iron ore, nickel and steel. A material slowing in

China’s economic growth trajectory could result in lower prices for commodities. Further, with China being a significant producer of aluminum and

steel, it is possible that the country may be less disciplined and export large quantities of these materials, further depressing global prices.

Primary Molybdenum Investment Risks include:

Molybdenum prices remain significantly above their marginal cost of production, and over the long term, prices may return to a reasonable margin

above cost.

Roasting molybdenum produces carbon dioxide and sulfuric acid. Increased government regulation, with respect to the storage or sequestration of

these materials, could negatively impact company economics.

The widespread acceptance of a molybdenum substitute for molybdenum could negatively impact demand for the metal.

Primary Uranium Investment Risks include:

The Japanese nuclear disaster intensifies in magnitude causing more countries to halt new reactor build rates or shut down reactors that are

already operating.

New technologies are developed to more efficiently recycle spent fuel, effectively increasing supply since fuel currently considered spent still

contains significant amounts of fissile material that cannot currently be used with existing technology.

Government entities liquidating stocks of highly enriched uranium from warhead stockpiles more quickly than forecast, thereby flooding the market

with supply.

Primary Rare Earth Investment Risks include:

In the past, China, which controls 97% of global supply, has flooded the market with rare earths, depressing the price. If China were to remove all

export restrictions, it is possible that rare earth prices may fall beyond our expectations.

If prices of rare earth elements continue to trend significantly higher, it is possible that substitution will begin to affect demand. For example, lithium

batteries can be used as a substitute for nickel-metal hydride batteries, which use lanthanum.

MEMBER: FINRA/SIPC 13 www.dahlmanrose.com

14. DAHLMAN ROSE & CO. EQUITY RESEARCH

If national governments begin to classify rare earths as strategic assets and begin building stockpiles, uneconomical mining of rare earths may be

subsidized in order to increase supply, and therefore pressuring prices.

MEMBER: FINRA/SIPC 14 www.dahlmanrose.com

15. DAHLMAN ROSE & CO. EQUITY RESEARCH

Disclosures

Disclaimer:

The information presented in this report is for informational purposes only. It was prepared based on information and sources that we believe to be

reliable, but we make no representations or guarantees as to the accuracy or completeness of the information contained herein. This report is not to

be construed as an offer to sell or a solicitation of an offer to buy any security. The opinions expressed in this report may change without notice.

Certification:

Each analyst identified in this report certifies in accordance with SEC Regulation AC, with respect to any company and securities discussed in this

report, that the recommendations and opinions expressed accurately reflect the analyst's personal views and no part of the analyst's compensation

was, is, or will be, directly or indirectly, related to the specific recommendations or views expressed herein.

Required Disclosures:

No analyst who participated in the creation of this report owns securities issued by the subject companies.

Dahlman Rose & Company, LLC, and/or its affiliates may have positions in the securities discussed in this report. However, none of those positions

equal or exceed 1% of the equity securities outstanding for the subject companies.

Dahlman Rose & Company, LLC, and/or any of its analysts, officers or employees, or any household members do not serve as an officer, director or

advisory board member of any of the companies discussed in this report.

Dahlman Rose & Company, LLC intends to seek to be a financial advisor or to engage in investment banking services with one or any of the subject

companies discussed in its research reports and may receive compensation for such services during the three months following publication of

this Report. As a result, investors should be aware that the firm might have a conflict of interest that could affect the objectivity of this report. For

disclosures regarding investment banking activity in the past 12 months, please contact Compliance, Dahlman Rose & Company, LLC, 1301 Avenue

of the Americas, 44th Floor, New York, NY 10019.

This report constitutes a compendium report (covers six or more subject companies). As such, Dahlman Rose & Company, LLC. chooses to provide

specific disclosures for the companies mentioned by reference. To access current disclosures for the all companies in this report, clients should refer

to our Disclosure Site or contact your Dahlman Rose & Company, LLC. representative for additional information.

Dahlman Rose & Company, LLC is not a tax or legal advisor and provides no legal or tax advice or opinions with respect to the securities

recommended in this report.

For disclosures regarding market making activity, please contact Compliance Department, Dahlman Rose & Company, LLC, 1301 Avenue of the

Americas, 44th Floor, New York, NY 10019.

Stock Ratings:

Dahlman Rose & Company, LLC assigns the following ratings to the securities of its subject companies:

Buy – The fundamentals/valuations of the subject company are improving and the investment return is expected to be 5 to 15 percentage points

higher than the general market return.

MEMBER: FINRA/SIPC 15 www.dahlmanrose.com

16. DAHLMAN ROSE & CO. EQUITY RESEARCH

Sell – The fundamentals/valuations of the subject company are deteriorating and the investment return is expected to be 5 to 15 percentage points

lower than the general market return.

Hold – The fundamentals/valuations of the subject company are neither improving nor deteriorating and the investment return is expected to be in

line with the general market return.

Ratings Distribution:

Ratings Distribution & Investment Banking Disclosure

Rating Count Ratings Distribution* Count Investment Banking**

Buy -rated 122 52.60 37 30.33

Hold -rated 105 45.30 35 33.33

Sell -rated 5 2.20 2 40.00

MEMBER: FINRA/SIPC 16 www.dahlmanrose.com