Foreign Ownership of Debt is an Important Indicator of Vulnerability to the Emerging Market Crisis

•

0 likes•887 views

Recommended

Recommended

More Related Content

More from QNB Group

More from QNB Group (20)

Recently uploaded

Recently uploaded (20)

Foreign Ownership of Debt is an Important Indicator of Vulnerability to the Emerging Market Crisis

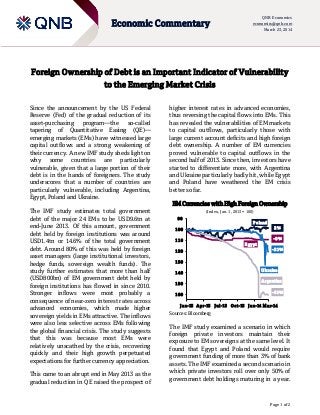

- 1. Page 1 of 2 Economic Commentary QNB Economics economics@qnb.com March 23, 2014 Foreign Ownership of Debt is an Important Indicator of Vulnerability to the Emerging Market Crisis Since the announcement by the US Federal Reserve (Fed) of the gradual reduction of its asset-purchasing program—the so-called tapering of Quantitative Easing (QE)— emerging markets (EMs) have witnessed large capital outflows and a strong weakening of their currency. A new IMF study sheds light on why some countries are particularly vulnerable, given that a large portion of their debt is in the hands of foreigners. The study underscores that a number of countries are particularly vulnerable, including Argentina, Egypt, Poland and Ukraine. The IMF study estimates total government debt of the major 24 EMs to be USD9.6tn at end-June 2013. Of this amount, government debt held by foreign institutions was around USD1.4tn or 14.6% of the total government debt. Around 80% of this was held by foreign asset managers (large institutional investors, hedge funds, sovereign wealth funds). The study further estimates that more than half (USD800bn) of EM government debt held by foreign institutions has flowed in since 2010. Stronger inflows were most probably a consequence of near-zero interest rates across advanced economies, which made higher sovereign yields in EMs attractive. The inflows were also less selective across EMs following the global financial crisis. The study suggests that this was because most EMs were relatively unscathed by the crisis, recovering quickly and their high growth perpetuated expectations for further currency appreciation. This came to an abrupt end in May 2013 as the gradual reduction in QE raised the prospect of higher interest rates in advanced economies, thus reversing the capital flows into EMs. This has revealed the vulnerabilities of EM markets to capital outflows, particularly those with large current account deficits and high foreign debt ownership. A number of EM currencies proved vulnerable to capital outflows in the second half of 2013. Since then, investors have started to differentiate more, with Argentina and Ukraine particularly badly hit, while Egypt and Poland have weathered the EM crisis better so far. EM Currencies with High Foreign Ownership (Index, Jan. 1, 2013 = 100) Sources: Bloomberg The IMF study examined a scenario in which foreign private investors maintain their exposure to EM sovereigns at the same level. It found that Egypt and Poland would require government funding of more than 3% of bank assets. The IMF examined a second scenario in which private investors roll over only 50% of government debt holdings maturing in a year. Mar-14 Egypt Poland Ukraine 90 100 110 120 130 140 150 160 Jan-13 Apr-13 Jul-13 Oct-13 Jan-14 -21% -9% -61% 2% Argentina

- 2. Page 2 of 2 Economic Commentary QNB Economics economics@qnb.com March 23, 2014 In this case, Argentina and Ukraine would also become sensitive to foreign outflows. The IMF analysis has proved itself relevant in recent months with the currencies of Argentina, Ukraine and, to a lesser extent, Egypt all succumbing to vulnerabilities. Argentina and Ukraine both have relatively high foreign ownership of government debt (30% and 46% respectively) and have faced severe currency weakness. Meanwhile, Egypt has a lower level of foreign ownership (13%) and has not experienced such a severe depreciation. The Argentinean economy has been blighted by burdensome debt, weak growth and high inflation, resulting in a steady weakening of the Argentine Peso for a number of years. This accelerated into a full-blown collapse in January 2014 as international reserves fell to unsustainable levels. Political instability in Ukraine eroded confidence in its currency in early 2014. Russia’s military intervention in Crimea heightened tensions more recently and led to further capital outflows and a sharp weakening of the currency. This is likely to continue unless a political solution to the Crimea crisis is found. In Egypt, low levels of foreign debt ownership mean that capital flight has been lower, making it easier for the authorities to support the currency. In addition, significant GCC grants in 2013 have helped the government to reduce its reliance on foreign investors buying its debt. This has helped maintain a relatively steady exchange rate of the Egyptian Pound during late 2013 and early 2014, notwithstanding major political developments. Despite high foreign ownership of government debt in Poland (50%), the currency has performed well as the economy is growing strongly and overall government debt is falling. However, should the economic situation turn sour, foreign ownership provides an important indicator that the country would be vulnerable to capital outflows. Overall, the IMF study provides an interesting new insight into the ongoing development of the EM crisis associated with QE tapering. It suggests that both large current account deficits and high foreign ownership of government debt can be key indicators of an EM vulnerability to continued capital flight. Contacts Joannes Mongardini Head of Economics Tel. (+974) 4453-4412 Rory Fyfe Senior Economist Tel. (+974) 4453-4643 Ehsan Khoman Economist Tel. (+974) 4453-4423 Hamda Al-Thani Economist Tel. (+974) 4453-4646 Ziad Daoud Economist Tel. (+974) 4453-4642 Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be reproduced in whole or in part without permission from QNB Group.