INFOGRAPHIC - Cloud Computing Competitive Landscape 2014

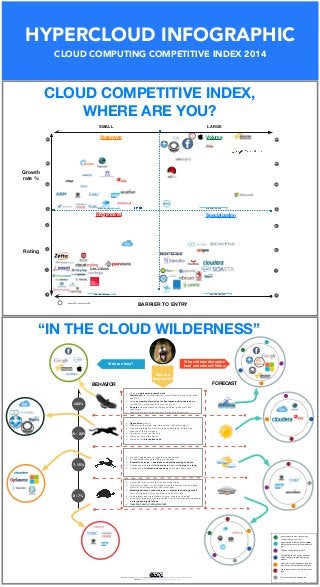

This infographic attempts to illustrate the cloud computing competitive landscape for 2014 - 2015 based on 4 distinct aspects - namely economies of scale/volume, cloud specialisation competencies, stalemate vendors with ageing technologies and services and finally fragmented cloud providers with limited reach and vertical focus. Methodology used: 1. For publicly traded firms, their revenue growth was used to determine their financial health and competitiveness. On the other hand their technical and delivery competencies are determined based on the marketshare they have in cloud or cloud-related work they have done for their clients. For a high resolution version please download it here: http://tarrysingh.com/2014/04/cloud-computing-competitive-landscape-2014-an-infographic/

Recommended

Recommended

More Related Content

Viewers also liked

Viewers also liked (7)

Recently uploaded

Recently uploaded (20)

INFOGRAPHIC - Cloud Computing Competitive Landscape 2014

- 1. BARRIER TO ENTRY Stalemate Volume SpecializationFragmented SMALL LARGE 10% 20% 30% market share Growth rate % 0% market share market share 5 10 15 0 Rating “IN THE CLOUD WILDERNESS” 10% 20% 30% 0% 5 10 15 0 0 - 7% ✓ On very aggressive growth path ✓ Predatory with lots of aerial view, lots of stealth-work, talent-grab and M&A ✓ Using extremely disruptive technologies and techniques to surprise the competition and woo the buyer ✓ Popular: Unpredictable yet darlings with early adopters and consumers ✓ Leadership in servicized products & productised services ✓ Aggressive growth ✓ Predatory with a clear two-dimensional LoS (line of sight) ✓ Creative strategies to maintain the double-digit growth at the expense of the turtle-pack ✓ Continues to out-run the hare ✓ Watch out for aerial attacks ✓ Watch out for disruptive tech ✓ Growth sluggishness yet slightly positive outlook ✓ Sr. leadership change in offing or underway ✓ Dramatic change in business models/operating models ✓ Challenges with interim turn-around initiatives; taking too long ✓ Challenges with talent-pool exodus to cheetah and eagle! ✓ Successful with current tech/current client base ✓ Internal cost-base, not yet aligned with the transformed operating model of its existing and/or new client base ✓ Misaligned talent-resource pool to digital technology stack such as big data, social, analytics, mobile and cloud ✓ Losing talent and marketshare to hare, cheetah and eagle. ✓ Looking at large/mid-size acquisition to gain marketshare/mindshare in disruptive digital stack ✓ Investing heavily in disruptive tech Who are they? How are they today? Who will take disruptive lead and who will follow Recent IPO/ upcoming IPOs Sources : Wikiinvest, FT.com, Fool.com, Yahoo Finance, Cloudtimes Top 100, Livemint FORECASTBEHAVIOR 7-15% 15 - 22% >22% Aggressively introduce and own new disruptive tech zone (IoT, searabletech etc.) Organic and inorganic growth Cannibalise its own ageing business model to adopt/consume emerging models Invest heavily in R&D; Technology championship prime goal Transform current/ageing services into disruptive or near-disruptive services White label current tech into disruptive tech Stick to current business model market share CLOUD COMPETITIVE INDEX, WHERE ARE YOU? HYPERCLOUD INFOGRAPHIC CLOUD COMPUTING COMPETITIVE INDEX 2014 HyperCloud Infographic by Tarry Singh is licensed under a Creative Commons Attribution-NonCommercial 4.0 International License.