ACC1000 Past Paper Summary | Monash University

•

3 likes•1,681 views

Download ACC1000 cheat sheet completely free + more videos and notes: http://goo.gl/pn8x4B

Recommended

More Related Content

Recently uploaded

Recently uploaded (20)

Featured

Featured (20)

ACC1000 Past Paper Summary | Monash University

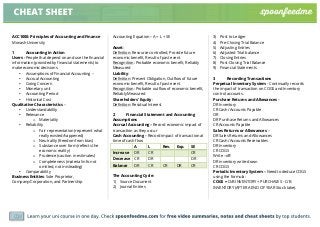

- 1. Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students. CHEAT SHEET ACC1000: Principles of Accounting and Finance Monash University 1 Accounting in Action Users - People that depend on and use the financial information (provided by financial statements) to make economic decisions. • Assumptions of Financial Accounting – • Accrual Accounting • Going Concern • Monetary unit • Accounting Period • Historical Cost Qualitative Characteristics – • Understandability • Relevance o Materiality • Reliability o Fair representation (represent what really existed/happened) o Neutrality (freedom from bias) o Substance over form (reflects the economic reality) o Prudence (caution in estimates) o Completeness (material info not omitted, not misleading) • Comparability Business Entities: Sole Proprietor, Company/Corporation, and Partnership Accounting Equation – A = L + SE Asset: Definition: Resource controlled, Provide future economic benefit, Result of past event Recognition: Probable economic benefit, Reliably Measured Liability: Definition: Present Obligation, Outflow of future economic benefit, Result of past event Recognition: Probable outflow of economic benefit, Reliably Measured Shareholders’ Equity: Definition: Residual Interest 2 Financial Statement and Accounting Assumptions Accrual Accounting – Record economic impact of transaction as they occur Cash Accounting – Record impact of transaction at time of cash flow A L Rev. Exp. SE Increase DR CR CR Decrease CR DR DR Balance DR CR CR DR CR The Accounting Cycle: 1) Source Document 2) Journal Entries 3) Post to Ledger 4) Pre-Closing Trial Balance 5) Adjusting Entries 6) Adjusted Trial balance 7) Closing Entries 8) Post-Closing Trial Balance 9) Financial Statements 3 Recording Transactions Perpetual Inventory System - Continually records the impact of transaction on COGS and Inventory control accounts. Purchase Returns and Allowances – DR Inventory CR Cash/ Accounts Payable OR DR Purchase Returns and Allowances CR Accounts Payable Sales Returns or Allowances – DR Sales Returns and Allowances CR Cash/ Accounts Receivables DR Inventory CR COGS Write –off: DR inventory write-down CR COGS Periodic Inventory System – Need to deduce COGS using the formula: COGS = O/B INVENTORY + PURCHASES - C/B INVENTORY (AFTER A END OF YEAR Stock take).

- 2. Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students. CHEAT SHEET Purchase Returns and Allowances - DR Cash/ Accounts payable CR Purchase Returns and Allowances Sales Returns and Allowances - Sales Returns or Allowance: DR Sales Returns and Allowances CR cash/ accounts receivable Sales Journal - Records only credit sales during a period. Purchase Journal - Records only credit purchases during a period Cash Receipts journal - Records entries, which debit cash at bank Cash Payment Journal - Records all entries that credit cash at bank Accounting For GST • GST Paid = Represents the amount owed to you by the ATO • GST Collected = Represents the amount you owe the ATO 4 Adjusting Accounts Expiration of Assets - DR Insurance Expense CR Prepaid Insurance Unearned Revenue - DR Unearned Revenue CR Service Revenue Accrual of Unrecorded Revenue - DR Accrued Revenue CR Service Revenue Accrual of Unrecorded Expenses - DR Wages expense CR Accrued Wages Contra Account - Are accounts that record any detraction from the historical cost of an asset or liability control account Allowance for Doubtful Debt Creating Allowance for Doubtful Debt DR Bad Debt Expense CR Allowance for Doubtful Debt Writing Off Bad Debt DR Allowance for Doubtful debt CR Accounts Receivable Depreciation DR Depreciation Expense CR Accumulated Depreciation 5 Preparing the Financial Statements Closing Entries - Temporary accounts are closed to leave them with zero balances in preparation for the next reporting period. Post Closing Trial Balance - Lists all permanent accounts and their balances. Prepare Financial Statements – • Prepare Balance Sheet • Income Statement • Statement of Cash Flows 6 Financial Statement Analysis Analytical Methods – Horizontal/ Trend Analysis: Evaluate series of financial statement data over period of time Vertical Analysis: Expressing each item in financial statement as % of base amount Ratio Analysis: Expresses Relationship among selected items of financial data Useful Ratios – Performance Ratios Return on Assets = !"#$%&'() !"#!"# !"#$%" !"# !"#$% !""#$" Activity Ratios Asset turnover rate = !"#$% !"#"$%" !"#$% !""#$" Liquidity Ratios Current ratio = !"##$%& !""#$ !"##$%& !"#$"%"&' Financial Structure Ratios Debt to Equity Ratio = !"#$% !"#$"%"&"'( !"#$% !!!"#!!"#$%& !"#$%& Du Pont Analysis ROE = 𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠 𝑇𝑜𝑡𝑎𝑙 𝑆ℎ𝑎𝑟𝑒ℎ𝑜𝑙𝑑𝑒𝑟𝑠 𝐸𝑞𝑢𝑖𝑡𝑦 𝑋 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝑝𝑟𝑜𝑓𝑖𝑡 𝑎𝑓𝑡𝑒𝑟 𝑡𝑎𝑥 𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠 𝑅𝑒𝑣𝑒𝑛𝑢𝑒 𝑋 𝑇𝑜𝑡𝑎𝑙 𝑆𝑎𝑙𝑒𝑠 𝑇𝑜𝑡𝑎𝑙 𝐴𝑠𝑠𝑒𝑡𝑠 Limitations • Estimates • Atypical Data • Diversification of Entities

- 3. Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students. CHEAT SHEET 7 Management and Control Non – Financial Performance Management – Balanced Scorecard: Formulated to translate an organisation’s mission/strategies into objectives/performance measures 4 Perspectives: • Financial • Customer • Internal Business Process • Learning and Growth Divisional Performance Management: 1) Evaluate a division’s performance 2) Evaluate performance of managers in those divisions 3) Evaluate level of investment in each division Responsibility Accounting: Hold managers accountable for the performance of their business units Only consider controllable costs (cost that the manager can exert control over). Ignore uncontrollable costs (manager can’t exert control over these costs). Financial Methods – R.O.I = !"#$%& !"#$%&'$"& (!"#$%&$' !"#$%"&) Residual Income = 𝑃𝑟𝑜𝑓𝑖𝑡 𝑏𝑒𝑓𝑜𝑟𝑒 𝑡𝑎𝑥 − (𝐶𝑜𝑠𝑡 𝑜𝑓 𝐶𝑎𝑝𝑖𝑡𝑎𝑙 𝑥 𝐼𝑛𝑣𝑒𝑠𝑡𝑚𝑒𝑛𝑡) 8 Cost and Costing Cost Behaviours – Variable Costs - Costs that vary directly, proportionately with changes in activity levels Fixed Costs - Costs that remain the same, regardless of changes in activity levels. High Low Method – Change in Total Costs (Highest Cost period − Lowest Cost Period) Highest Activity Level − Lowest Activity Level = 𝑉𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝐶𝑜𝑠𝑡 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 CVP Analysis – !#$% !#$ !#$ !##$% !#$%!!#$ !#$%' !#$ = Units needed !#$% !#$# !#$%%' !#$% + 𝑈𝑛𝑖𝑡 𝑉𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝐶𝑜s𝑡 = Unit Selling Price 𝑝𝑟𝑜𝑓𝑖𝑡 𝑎𝑓𝑡𝑒𝑟 𝑡𝑎𝑥 (1 − 𝑡𝑎𝑥 𝑟𝑎𝑡𝑒) + 𝐹𝑖𝑥𝑒𝑑 𝐶𝑜𝑠𝑡𝑠 𝑈𝑛𝑖𝑡 𝑆𝑒𝑙𝑙𝑖𝑛𝑔 𝑃𝑟𝑖𝑐𝑒 − 𝑈𝑛𝑖𝑡 𝑉𝑎𝑟𝑖𝑎𝑏l𝑒 𝐶𝑜𝑠𝑡 = 𝑄𝑢𝑎𝑛𝑡𝑖𝑡𝑦 𝑛𝑒𝑒𝑑𝑒𝑑 Overhead Allocation – Absorption Costing: 𝐸𝑠𝑡𝑖𝑚𝑎𝑡𝑒𝑑 𝐴𝑛𝑛𝑢𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡𝑠 𝐸𝑥𝑝𝑒𝑐𝑡𝑒𝑑 𝐴𝑛𝑛𝑢𝑎𝑙 𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑛𝑔 𝐴𝑐𝑡𝑖𝑣𝑖𝑡𝑦 = 𝑃𝑟𝑒𝑑𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑒𝑑 𝑜𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝑟𝑎𝑡𝑒 Activity Based Costing: Uses cost pools to accumulate the cost of significant business activities, allocating costs from these cost pools to products based on cost drivers, which measure each product’s/service’s demand for activities. 9 Strategic Management Accounting TQM - Reducing costs in the above phases, but at the same time, increasing quality/customer satisfaction JIT Processing - Management of inventory, in particular, reducing it. Lifecycle Costing - Estimating and accumulating the costs of a product over its entire life Target Costing 𝑇𝑎𝑟𝑔𝑒𝑡 𝑐𝑜𝑠𝑡 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡 = 𝑇𝑎𝑟𝑔𝑒𝑡 𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 − 𝑇𝑎𝑟𝑔𝑒𝑡 𝑝𝑟𝑜𝑓𝑖𝑡 𝑚𝑎𝑟𝑔𝑖𝑛 Kaizen Costing - Making incremental improvements during the production phase (e.g. improving processes, reducing costs in production/from suppliers, collaborative employee teamwork expertise) when large innovations may not be possible. Behavioural Aspects of Budgeting – Bias: Tension between upper and lower management Participation: encourage participation by lower management when setting budgets Slack: Temptation to inflate costs or depress sales forecast 10 11 Introduction to Finance and Financial Mathematics Steps of Capital Budgeting 1) Estimate all Cash Flows (both inflows and outflows). 2) Assess the riskiness of these Cash Flows.

- 4. Learn your uni course in one day. Check spoonfeedme.com for free video summaries, notes and cheat sheets by top students. CHEAT SHEET 3) Determine the borrowing costs of the project, by comparing such costs with the WACC – Weighted Average Capital Cost. 4) Find Net Present Value (NPV) and Internal Rate of Return (IRR). 5) Accept the project if: NPV 0, IRR WACC. NPV – • Calculates the expected net monetary gain or loss from a project by discounting all expected cash flows to the present • The amount of interest deducted is determined by the desired rate of return IRR – • IRR is the rate of return that a company can expect to earn by investing in a project