Apple Inc. designs consumer electronic devices including computers, phones, tablets and music players. The report issues a HOLD recommendation based on a valuation of $125.66 per share. While strong iPhone sales and a large cash position provide upside, uncertainty around new products like Apple Watch and a lack of sustainable growth models for maturing products like the iPad and Mac present risks.

Quan busquem l´ origen mes antic dels nostres avantpassats en la Vall de Segó, sempre apareix una referència a la Cova de la Collita en el terme de Quart de Les Valls, afirmant que en ella es va trobar ceràmica i un punxó d´ os de l´ Edat del Bronze valencià.

Autor: Sergi Arrando Máñez

Quan busquem l´ origen mes antic dels nostres avantpassats en la Vall de Segó, sempre apareix una referència a la Cova de la Collita en el terme de Quart de Les Valls, afirmant que en ella es va trobar ceràmica i un punxó d´ os de l´ Edat del Bronze valencià.

Autor: Sergi Arrando Máñez

A free version of Apple Inc. SWOT analysis 2016. To get the full presentation buy the SWOT here: https://www.strategicmanagementinsight.com/swot-analyses/apple-swot-analysis.html

Quadrant Strategic Objective Measure Target for YearFinanc.docxmakdul

Quadrant Strategic Objective Measure Target for Year

Financial

Be profitable at the end

of the year profit margin Breakeven

Customer

Grow business by

focusing on gaining

customer and

outstanding customer Market share

5%

Operation

Build on to the Apple

name and expand brand

Marketing campaign

with a developed

plan in place 4 months

Learning and Growth

Employees have proper

training and knowledge

to expand brand Training hours 20 hours

Running Head: APPLE CORPORATION

APPLE CORPORATION

7

Daniel Price

Professor Keen

BUS/475

Week 4

Apple Corporation

Apple Corporation

Introduction

Apple Corporation is an American universal technology company with its headquarters in Cupertino, California. It deals with developing computer software and designing and selling consumer electronics. It also offers online services. The hardware products of Apple include smart phones, iPads, iPods and personal computers. The consumer software includes the iTunes media player, iOS operating system, OS X and the Safari web browser. Its online services include the iOS App Store, iCloud, Mac App Store and the iTunes store.

Apple Corporation was founded by a group of associates on 1st April 1976 to design and sell personal computers. It was however incorporated as Apple Computer Inc. on 3rd January 1977 only to be renamed thirty years later to Apple Inc due to its focus on consumer electronics. It is the largest technology firm in terms of total assets and revenue and the second mobile manufacturer after Samsung. It has a net worth of over 700billion USD with over one hundred thousand employees and over four hundred retail stores around the world. Apple Inc. has over one billion products in the market as at May 2016.

However, the aim of this paper is to develop strategic objectives in the measurement of attaining company's vision and mission based on a balanced scorecard taking into account different perspectives of the whole company. The balanced scorecard contains the financial perspective, Customer value, Internal Operations and Employee perspective.

Financial Perspective

Apple Corporation is the world’s largest technology company based on total assets and revenue valued at over 700 USD as at May 2016 (Ingram, 2008). It is also the world’s second largest mobile phone manufacturer. Apple Corporation Inc entered the top ten Fortune 500 list of publicly traded companies on May 2013. It announced a dividend of $0.57 in May 2016 after earning revenue of $51.5 billion and a net profit of $11.1 billion which was a 22% increase in revenue from the previous year. Apple Inc has transferred 90% of its cash and marketable securities outside the United States, which is about 234billion USD due to tax purposes. In 2015, the company accumulated over 80% of the total earnings made by the eight largest universal smart phone manufacturers.

High tax rates in the United States pose big threat to the profitability of Apple Corporation Inc. In ord ...

Running Head Apple CompanyApple Company.docxSUBHI7

Running Head: Apple Company

Apple Company

Apple Company

Name

Course

Date

Apple Company

The products at apple include Ipads, IPhones, Tablets, macintosh, Apple TV. These items have done well in the market and their request is still high. The organization Apple Inc. begun in 1977 January, 3. The organization has composed items like advanced music players, PCs related programming, which are one of a kind in nature. The organization has done enormously well with regards to advancement and making of astounding and great products that have intensely beaten their opponent in the market. This paper is an outlook on the structure, products and nature of the apple company with regards to stakeholders and corporate social responsibility.

Apple's achievement is their craft of offering magnificent client benefit understanding and in-store better alternatives. The Company gives assortment of items and even the sales people use wonderful language. Apple evaluated that just about half of individuals purchasing Apple items are new clients. Apple has utilized talented and experienced group of offers representatives who have added to organization's prosperity. The organization in 2002 opened tech retail I Tokyo, Japan and there after the organization has kept on opening more shops all around. Their retail technique has truly worked to support them in this manner with higher returns compared to their counterparts (Francois nonnenmancher, 2004).

Apple's hierarchical structure is one of the variables adding to the organization's fruitful advancement. An association's authoritative structure can make open doors for business development. However, it can likewise force restrains on how the firm creates. For Apple's situation, the hierarchical structure is principally a conventional pecking order, with some key components from different sorts of authoritative structure. The achievement of the organization is connected to advancement and the authority of Steve Jobs, however its hierarchical structure is halfway in charge of guaranteeing support for such administration. Presently, under Tim Cook's administration, Apple has rolled out some little improvements in its hierarchical structure to suit market and industry requests.The advantages of Apple's various leveled hierarchical structure incorporate tight control controlled by senior administration over all parts of the business. Also, advancement openings rouse representatives to perform well and there are clear levels of expert and duty. On the negative side, Apple's progressive authoritative structure may trade off adaptably off the business to reflect changes in the worldwide commercial center. Moreover, in various leveled associations correspondence across various offices has a tendency to be less compelling than in level associations (Dudovskiy, 2018).

Unveiled over 10 years ago, the iPod is the one gadget that changed Apple from a PC organization into a mass-advertise hardware monster and would late ...

Running head EXTERNAL ENVIRONMENT SCAN—APPLE .docxjoellemurphey

Running head: EXTERNAL ENVIRONMENT SCAN—APPLE 1

EXTERNAL ENVIRONMENT SCAN—APPLE 5

External Environment Scan—Apple

An environmental scan is vital for every company as it helps to determine the threats and opportunities that are posed to the company. The following will be included in the environment scan of Apple incorporated: economic factors, political factors, legal factors, societal factors, technological factors, geographic factors and Porter’s five forces.

Key Factors and Trends

The economic environment of the company is determined by factors such as taxation policies, exchange rate, inflation, the economy, living standards, the average income and consumer buying power. Apple’s products main target market are people of medium to high income and standards. In an economic boom, the company’s products are more likely to be bought than during a recession. The rapid growth of developing countries provide an opportunity for Apple to venture into new markets.

Political stability can be a threat to Apple’s products. Poor political stability would mean a reduction in sales and distribution of the products would be hard as trade barriers would be imposed. Various trade policies that could be imposed on a country would have an adverse effect on the company’s sales. However, developing countries create an opportunity for Apple expand its customer base as more free trade policies are put into effect. As Lombardo (2015) states, “Additional free trade policies increase the opportunities for Apple to distribute more of its products to various markets around the world” (section 2).

Social-cultural factors, such as lifestyle, living standards, and demographics important to Apple. Social factors have an effect on consumer behavior and expectations. The increase in mobile phone use and social media is an opportunity for Apple to provide easy-to-use smart phones.

Current technology and technological changes can affect a customer’s priorities changing the demand for Apple products. For example, with the increasing popularity of Cloud computing, Apple can use that to bring in customers and retain their existing customers. Apple has taken advantage of this by making it so that information can be transferred between the different apple devices and between family members. “Everything’s better when shared, and sharing has never been easier” (Apple, 2016, section 3).

Legal factors can also create a threat to Apple. As governments become more aware of privacy issues in relation to digital technology, stricter regulations are imposed on companies like Apple. This poses a threat to Apple as they are now required to develop a product that not only meets consumer demand, but also the privacy regulations imposed by the government. Stricter regulations have been implemented on telecommunications therefore increasing threats to Apple. ...

This presentation discusses one of the business concept i.e. startups and one of the top rated multi national startup company, Apple Inc. Also it includes various points like risks associated, market scenario, steps to make a startup successful and other various topics. Take a look.

This document is originally written by AssignmentWOrkHelp. This report explains the successful running of the business of the Apple company. This shows the detail description of the factors influencing the future business, its internal analysis

and the reason of the success of the apple business.For more information, contact https://www.assignmentworkhelp.com/contact/

Day 7HEALTH COMMUNICATION EVALUATION RESEARCHEvOllieShoresna

Day 7

HEALTH COMMUNICATION

EVALUATION RESEARCH

Evaluation Research

Homework

AGENDA

PROGRAM

EVALUATION

ACTIVITIES....

USEFUL

FEASIBLE

ETHICAL

ACCURATE (CDC, 2010)

WHAT IT IS?

https://meera.snre.umich.edu/evaluation-what-it-and-why-do-it#should

How is it Done?

ID Program Elements to Monitor

Select Key Evaluation Questions

(CDC, 2010)

Determine How Info will be Gathered

Develop a Data Analysis & Reporting Plan

Develop a Timetable & Budget

ID Program Elements to Monitor

MONITORING /PROCESS

EVALUATION

REACH

FIDELITY

WHO , HOW , WHAT ,

WHETHER

(CDC , 2010)

WHAT DO SOME BASIC

EVALUATION QUESTIONS

INCLUDE?

WHAT SHOULD YOU FIND

OUT FROM

STAKEHOLDERS?

Select Key Evaluation Questions

(CDC, 2010)

Determine How Info will be Gathered

EXPERIMENTAL DESIGNS

CORRELATIONAL DESIGNS

QUASI-EXPERIMENTAL DESIGNS

CASE STUDY DESIGNS

QUANTITATIVE QUALITATIVE

(CDC, 2010)

DEVELOP A DATA ANALYSIS & REPORTING PLAN

INCLUDE HOW THE DATA FOR

EACH MONITORING &

EVALUATION QUESTION WILL BE

CODED , SUMMARIZED &

ANALYZED

DESCRIBE HOW MONITORING &

EVALUATION DATA WILL BE

REPORTED

(CDC, 2010)

DEVELOP A

TIMETABLE &

BUDGET

YOUR TIMELINE SHOULD

COVER . . . .

(CDC, 2010)

YOUR BUDGET SHOULD

INCLUDE . . . .

https://www.cdc.gov/eval/materials/index.htm

https://www.cdc.gov/eval/materials/index.htm

https://www.youtube.com/watch?v=XNR3KZzDoGQ

https://www.cdc.gov/healthcommunication/pdf/evaluationplanning.pdf

(Kreps , 2014)

EVALUATION RESEARCH CAN

ANSWER...

THE NEED FOR EVALUATION DATA

ID Problems

Guide design interventions

Examine costs & benefits

Advocate for needed support

(Kreps , 2014)

(Kreps , 2014)

THE NATURE FOR EVALUATION

DATA

Good evaluation data provides health COM program providers with critically

important information regarding the following...

VALIDITY OF EVALUATION RESEARCH

(KREPS , 2014 )

No research is better than research done poorly

Consider limitations of research

Internal validity

External validity

(Kreps , 2014)

FORMATIVE & SUMMATIVE

EVALUATION RESEARCH

"formative research looks at key parts of health communication interventions,

providing a microscopic analysis of individual components and influences of the

programs, summative research looks at the big picture of the overall influences of

health communication intervention programs."

METHODOLOGICAL ISSUES...

(KREPS , 2014 )

Cross-Sectional Data Self-Report Data

Tangential Variables Shallow Data

CH . 3 , PP . 85-98

CH . 7 , PP . 221-223

PERRAULT & CLARK

(2018 )

6

Comparison Between Microsoft Corporation and Apple Inc

Keenya Davis

South University

Comparison Between Microsoft Corporation and Apple Inc

Apple and Microsoft both provide top-of-the-line electronics, and both have operated in the market for many years now and are world-famous, so consumers continue to purchase goods. Many considerations are taken into account to de ...

General Environment, Forces of Competition, Future Improvement, Op.docxshericehewat

General Environment, Forces of Competition, Future Improvement, Opportunities, Strength and Weaknesses of Apple Inc.

Introduction

Apple Inc. is a multinational company that was found by Steve Jobs and Steve Wozniak in the year 1976. Since then, the company has able to produce mobile phones, iPads, personal computers and operating systems (Finkle, & Mallin, 2010). The company is successful under the current leadership of Timothy Donald. This paper will discuss the general environment, opportunities, threat, strength and capabilities of the company.

General Environment

The main segments of the general environment that affect Apple is the technology and social-cultural aspects. Technology has enabled the company to produce innovative and attractive products which attract customers. The socio-cultural segment of general environment involves values and attitude of people about products of the organization.

Technological Segment of the Environment

The technological segment of the environment influences how business operations are conducted—the segment use of advanced techs to design new and innovative products. Apple is ever-growing due to adoption of new and advanced technology. Advancement in technology has stiffened competition in the market. Apple uses better technologies such as wireless technology, cloud services and software to stay ahead in the competition.

Socio-Cultural Segment of the Environment

Social-Cultural segment refers to values and beliefs of people towards products and services of the organization. The positive interest and beliefs of people towards communication and entertainment results in the development of industries that deal with ICT. As a result, Apple incorporation continues to grow due to the interest of society towards its products and services. Similarly, the popularity of internet ad mobile phones leads to the success of the company. The company has prioritized to meet the demands of its customers by producing goods that are innovative and attractive.

Forces of Competition

The forces of competition are five. They include rivalry among competitors, threats of new entrants, threats of substitute commodities, bargaining power of suppliers and bargaining power of customers. In this assignment, rivalry among competitors and the bargaining power of suppliers is discussed.

Rivalry Among Competitors

Apple uses advanced technology and innovation to produce goods that are uniquely designed. The company make use of brand management to ensure its products are unique and innovative. The company has introduced produced products with a new feature, designs and performance to maintain market distinctness. All these changes have enabled Apple to stay ahead of the competition.

Apple should launch more products with unique design and features to stand out in the market. The company should also products other products and software to maintain market distinctness. The products should have new and updated features, version and ...

Full strategic case analysis for Apple incorporation including industry , competitor's and firm's self analysis. It covers all the strategic issues facing the industry and Apple inc. as well as the recommended solutions for these issues on business and corporate levels.

The study shows the development on the Apple Inc. mission& vision and the strategic objectives over time.

12 External and Internal Environments Mikia DixonBusiness BenitoSumpter862

1

2 External and Internal Environments

Mikia Dixon

Business Admin. Capstone BUS499

Professor Joseph Keller

November 11, 21

Apple corporation's general environment plays a significant role in influencing its working mechanisms both locally and internationally. External influences in the company distant or macro-environment have a direct impact on the company's performance. In the consumer electronics and information technology services industries, the company's performance is due to strategic management that exploits opportunities and defends the company from risks. Two of the most highly ranked general environment factors of the company include technology and economic environment factors.

Technology and technology breakthroughs are examined to identify company opportunities and dangers in the present and the future. Apple has a chance to grow by offering its technology services to a wider range of customers and institutions thanks to the growing importance of technology integration in business. For Apple to keep up with its competition, the company needs to release new goods more frequently. Apple's brand image and financial performance are negatively impacted by Apple's competitors' low-cost offerings of high-value technical products. Samsung, for example, has maintained its position in the PC market, whereas Apple has lost it. Competition from low-cost, high-tech rivals has contributed to this situation. Apple now has a big chance to take advantage of the growing demand for cloud computing services by establishing an extended cloud framework. The technological environment is likely to impact the future steps taken by the company because presently, this field is filled with numerous players who are all gearing towards competing with apple. With the new emerging trends in technology, the company is highly obligated to have working mechanisms that protect them from any threat from external sources such as competitors.

The economic environment impacts the working mechanisms of apple corporation in numerous significant ways. With the set-up of the modern global market dynamics, apple's success as a company relies on the sales made. For sales to be made, there must be markets that are dependent on good economies. According to MBA school Team (2021), Apple Corporation has numerous expansion opportunities. For instance, economic stability in industrialized countries, rapid economic growth in developing countries, and disposable income among target consumers. However, it is important to keep in mind all the competing factors in the worldwide marketplaces when investigating economic opportunities. In the context of major international corporations like Samsung and Huawei, these external strategic drivers represent growth opportunities for the company and its competitors.

Five forces of competition, also known as the Porter five forces analysis, are those elements that determine the success of a corporation through a comprehensive analysis of t ...

More Related Content

Similar to Writing Sample - Equity Research - AAPL

A free version of Apple Inc. SWOT analysis 2016. To get the full presentation buy the SWOT here: https://www.strategicmanagementinsight.com/swot-analyses/apple-swot-analysis.html

Quadrant Strategic Objective Measure Target for YearFinanc.docxmakdul

Quadrant Strategic Objective Measure Target for Year

Financial

Be profitable at the end

of the year profit margin Breakeven

Customer

Grow business by

focusing on gaining

customer and

outstanding customer Market share

5%

Operation

Build on to the Apple

name and expand brand

Marketing campaign

with a developed

plan in place 4 months

Learning and Growth

Employees have proper

training and knowledge

to expand brand Training hours 20 hours

Running Head: APPLE CORPORATION

APPLE CORPORATION

7

Daniel Price

Professor Keen

BUS/475

Week 4

Apple Corporation

Apple Corporation

Introduction

Apple Corporation is an American universal technology company with its headquarters in Cupertino, California. It deals with developing computer software and designing and selling consumer electronics. It also offers online services. The hardware products of Apple include smart phones, iPads, iPods and personal computers. The consumer software includes the iTunes media player, iOS operating system, OS X and the Safari web browser. Its online services include the iOS App Store, iCloud, Mac App Store and the iTunes store.

Apple Corporation was founded by a group of associates on 1st April 1976 to design and sell personal computers. It was however incorporated as Apple Computer Inc. on 3rd January 1977 only to be renamed thirty years later to Apple Inc due to its focus on consumer electronics. It is the largest technology firm in terms of total assets and revenue and the second mobile manufacturer after Samsung. It has a net worth of over 700billion USD with over one hundred thousand employees and over four hundred retail stores around the world. Apple Inc. has over one billion products in the market as at May 2016.

However, the aim of this paper is to develop strategic objectives in the measurement of attaining company's vision and mission based on a balanced scorecard taking into account different perspectives of the whole company. The balanced scorecard contains the financial perspective, Customer value, Internal Operations and Employee perspective.

Financial Perspective

Apple Corporation is the world’s largest technology company based on total assets and revenue valued at over 700 USD as at May 2016 (Ingram, 2008). It is also the world’s second largest mobile phone manufacturer. Apple Corporation Inc entered the top ten Fortune 500 list of publicly traded companies on May 2013. It announced a dividend of $0.57 in May 2016 after earning revenue of $51.5 billion and a net profit of $11.1 billion which was a 22% increase in revenue from the previous year. Apple Inc has transferred 90% of its cash and marketable securities outside the United States, which is about 234billion USD due to tax purposes. In 2015, the company accumulated over 80% of the total earnings made by the eight largest universal smart phone manufacturers.

High tax rates in the United States pose big threat to the profitability of Apple Corporation Inc. In ord ...

Running Head Apple CompanyApple Company.docxSUBHI7

Running Head: Apple Company

Apple Company

Apple Company

Name

Course

Date

Apple Company

The products at apple include Ipads, IPhones, Tablets, macintosh, Apple TV. These items have done well in the market and their request is still high. The organization Apple Inc. begun in 1977 January, 3. The organization has composed items like advanced music players, PCs related programming, which are one of a kind in nature. The organization has done enormously well with regards to advancement and making of astounding and great products that have intensely beaten their opponent in the market. This paper is an outlook on the structure, products and nature of the apple company with regards to stakeholders and corporate social responsibility.

Apple's achievement is their craft of offering magnificent client benefit understanding and in-store better alternatives. The Company gives assortment of items and even the sales people use wonderful language. Apple evaluated that just about half of individuals purchasing Apple items are new clients. Apple has utilized talented and experienced group of offers representatives who have added to organization's prosperity. The organization in 2002 opened tech retail I Tokyo, Japan and there after the organization has kept on opening more shops all around. Their retail technique has truly worked to support them in this manner with higher returns compared to their counterparts (Francois nonnenmancher, 2004).

Apple's hierarchical structure is one of the variables adding to the organization's fruitful advancement. An association's authoritative structure can make open doors for business development. However, it can likewise force restrains on how the firm creates. For Apple's situation, the hierarchical structure is principally a conventional pecking order, with some key components from different sorts of authoritative structure. The achievement of the organization is connected to advancement and the authority of Steve Jobs, however its hierarchical structure is halfway in charge of guaranteeing support for such administration. Presently, under Tim Cook's administration, Apple has rolled out some little improvements in its hierarchical structure to suit market and industry requests.The advantages of Apple's various leveled hierarchical structure incorporate tight control controlled by senior administration over all parts of the business. Also, advancement openings rouse representatives to perform well and there are clear levels of expert and duty. On the negative side, Apple's progressive authoritative structure may trade off adaptably off the business to reflect changes in the worldwide commercial center. Moreover, in various leveled associations correspondence across various offices has a tendency to be less compelling than in level associations (Dudovskiy, 2018).

Unveiled over 10 years ago, the iPod is the one gadget that changed Apple from a PC organization into a mass-advertise hardware monster and would late ...

Running head EXTERNAL ENVIRONMENT SCAN—APPLE .docxjoellemurphey

Running head: EXTERNAL ENVIRONMENT SCAN—APPLE 1

EXTERNAL ENVIRONMENT SCAN—APPLE 5

External Environment Scan—Apple

An environmental scan is vital for every company as it helps to determine the threats and opportunities that are posed to the company. The following will be included in the environment scan of Apple incorporated: economic factors, political factors, legal factors, societal factors, technological factors, geographic factors and Porter’s five forces.

Key Factors and Trends

The economic environment of the company is determined by factors such as taxation policies, exchange rate, inflation, the economy, living standards, the average income and consumer buying power. Apple’s products main target market are people of medium to high income and standards. In an economic boom, the company’s products are more likely to be bought than during a recession. The rapid growth of developing countries provide an opportunity for Apple to venture into new markets.

Political stability can be a threat to Apple’s products. Poor political stability would mean a reduction in sales and distribution of the products would be hard as trade barriers would be imposed. Various trade policies that could be imposed on a country would have an adverse effect on the company’s sales. However, developing countries create an opportunity for Apple expand its customer base as more free trade policies are put into effect. As Lombardo (2015) states, “Additional free trade policies increase the opportunities for Apple to distribute more of its products to various markets around the world” (section 2).

Social-cultural factors, such as lifestyle, living standards, and demographics important to Apple. Social factors have an effect on consumer behavior and expectations. The increase in mobile phone use and social media is an opportunity for Apple to provide easy-to-use smart phones.

Current technology and technological changes can affect a customer’s priorities changing the demand for Apple products. For example, with the increasing popularity of Cloud computing, Apple can use that to bring in customers and retain their existing customers. Apple has taken advantage of this by making it so that information can be transferred between the different apple devices and between family members. “Everything’s better when shared, and sharing has never been easier” (Apple, 2016, section 3).

Legal factors can also create a threat to Apple. As governments become more aware of privacy issues in relation to digital technology, stricter regulations are imposed on companies like Apple. This poses a threat to Apple as they are now required to develop a product that not only meets consumer demand, but also the privacy regulations imposed by the government. Stricter regulations have been implemented on telecommunications therefore increasing threats to Apple. ...

This presentation discusses one of the business concept i.e. startups and one of the top rated multi national startup company, Apple Inc. Also it includes various points like risks associated, market scenario, steps to make a startup successful and other various topics. Take a look.

This document is originally written by AssignmentWOrkHelp. This report explains the successful running of the business of the Apple company. This shows the detail description of the factors influencing the future business, its internal analysis

and the reason of the success of the apple business.For more information, contact https://www.assignmentworkhelp.com/contact/

Day 7HEALTH COMMUNICATION EVALUATION RESEARCHEvOllieShoresna

Day 7

HEALTH COMMUNICATION

EVALUATION RESEARCH

Evaluation Research

Homework

AGENDA

PROGRAM

EVALUATION

ACTIVITIES....

USEFUL

FEASIBLE

ETHICAL

ACCURATE (CDC, 2010)

WHAT IT IS?

https://meera.snre.umich.edu/evaluation-what-it-and-why-do-it#should

How is it Done?

ID Program Elements to Monitor

Select Key Evaluation Questions

(CDC, 2010)

Determine How Info will be Gathered

Develop a Data Analysis & Reporting Plan

Develop a Timetable & Budget

ID Program Elements to Monitor

MONITORING /PROCESS

EVALUATION

REACH

FIDELITY

WHO , HOW , WHAT ,

WHETHER

(CDC , 2010)

WHAT DO SOME BASIC

EVALUATION QUESTIONS

INCLUDE?

WHAT SHOULD YOU FIND

OUT FROM

STAKEHOLDERS?

Select Key Evaluation Questions

(CDC, 2010)

Determine How Info will be Gathered

EXPERIMENTAL DESIGNS

CORRELATIONAL DESIGNS

QUASI-EXPERIMENTAL DESIGNS

CASE STUDY DESIGNS

QUANTITATIVE QUALITATIVE

(CDC, 2010)

DEVELOP A DATA ANALYSIS & REPORTING PLAN

INCLUDE HOW THE DATA FOR

EACH MONITORING &

EVALUATION QUESTION WILL BE

CODED , SUMMARIZED &

ANALYZED

DESCRIBE HOW MONITORING &

EVALUATION DATA WILL BE

REPORTED

(CDC, 2010)

DEVELOP A

TIMETABLE &

BUDGET

YOUR TIMELINE SHOULD

COVER . . . .

(CDC, 2010)

YOUR BUDGET SHOULD

INCLUDE . . . .

https://www.cdc.gov/eval/materials/index.htm

https://www.cdc.gov/eval/materials/index.htm

https://www.youtube.com/watch?v=XNR3KZzDoGQ

https://www.cdc.gov/healthcommunication/pdf/evaluationplanning.pdf

(Kreps , 2014)

EVALUATION RESEARCH CAN

ANSWER...

THE NEED FOR EVALUATION DATA

ID Problems

Guide design interventions

Examine costs & benefits

Advocate for needed support

(Kreps , 2014)

(Kreps , 2014)

THE NATURE FOR EVALUATION

DATA

Good evaluation data provides health COM program providers with critically

important information regarding the following...

VALIDITY OF EVALUATION RESEARCH

(KREPS , 2014 )

No research is better than research done poorly

Consider limitations of research

Internal validity

External validity

(Kreps , 2014)

FORMATIVE & SUMMATIVE

EVALUATION RESEARCH

"formative research looks at key parts of health communication interventions,

providing a microscopic analysis of individual components and influences of the

programs, summative research looks at the big picture of the overall influences of

health communication intervention programs."

METHODOLOGICAL ISSUES...

(KREPS , 2014 )

Cross-Sectional Data Self-Report Data

Tangential Variables Shallow Data

CH . 3 , PP . 85-98

CH . 7 , PP . 221-223

PERRAULT & CLARK

(2018 )

6

Comparison Between Microsoft Corporation and Apple Inc

Keenya Davis

South University

Comparison Between Microsoft Corporation and Apple Inc

Apple and Microsoft both provide top-of-the-line electronics, and both have operated in the market for many years now and are world-famous, so consumers continue to purchase goods. Many considerations are taken into account to de ...

General Environment, Forces of Competition, Future Improvement, Op.docxshericehewat

General Environment, Forces of Competition, Future Improvement, Opportunities, Strength and Weaknesses of Apple Inc.

Introduction

Apple Inc. is a multinational company that was found by Steve Jobs and Steve Wozniak in the year 1976. Since then, the company has able to produce mobile phones, iPads, personal computers and operating systems (Finkle, & Mallin, 2010). The company is successful under the current leadership of Timothy Donald. This paper will discuss the general environment, opportunities, threat, strength and capabilities of the company.

General Environment

The main segments of the general environment that affect Apple is the technology and social-cultural aspects. Technology has enabled the company to produce innovative and attractive products which attract customers. The socio-cultural segment of general environment involves values and attitude of people about products of the organization.

Technological Segment of the Environment

The technological segment of the environment influences how business operations are conducted—the segment use of advanced techs to design new and innovative products. Apple is ever-growing due to adoption of new and advanced technology. Advancement in technology has stiffened competition in the market. Apple uses better technologies such as wireless technology, cloud services and software to stay ahead in the competition.

Socio-Cultural Segment of the Environment

Social-Cultural segment refers to values and beliefs of people towards products and services of the organization. The positive interest and beliefs of people towards communication and entertainment results in the development of industries that deal with ICT. As a result, Apple incorporation continues to grow due to the interest of society towards its products and services. Similarly, the popularity of internet ad mobile phones leads to the success of the company. The company has prioritized to meet the demands of its customers by producing goods that are innovative and attractive.

Forces of Competition

The forces of competition are five. They include rivalry among competitors, threats of new entrants, threats of substitute commodities, bargaining power of suppliers and bargaining power of customers. In this assignment, rivalry among competitors and the bargaining power of suppliers is discussed.

Rivalry Among Competitors

Apple uses advanced technology and innovation to produce goods that are uniquely designed. The company make use of brand management to ensure its products are unique and innovative. The company has introduced produced products with a new feature, designs and performance to maintain market distinctness. All these changes have enabled Apple to stay ahead of the competition.

Apple should launch more products with unique design and features to stand out in the market. The company should also products other products and software to maintain market distinctness. The products should have new and updated features, version and ...

Full strategic case analysis for Apple incorporation including industry , competitor's and firm's self analysis. It covers all the strategic issues facing the industry and Apple inc. as well as the recommended solutions for these issues on business and corporate levels.

The study shows the development on the Apple Inc. mission& vision and the strategic objectives over time.

12 External and Internal Environments Mikia DixonBusiness BenitoSumpter862

1

2 External and Internal Environments

Mikia Dixon

Business Admin. Capstone BUS499

Professor Joseph Keller

November 11, 21

Apple corporation's general environment plays a significant role in influencing its working mechanisms both locally and internationally. External influences in the company distant or macro-environment have a direct impact on the company's performance. In the consumer electronics and information technology services industries, the company's performance is due to strategic management that exploits opportunities and defends the company from risks. Two of the most highly ranked general environment factors of the company include technology and economic environment factors.

Technology and technology breakthroughs are examined to identify company opportunities and dangers in the present and the future. Apple has a chance to grow by offering its technology services to a wider range of customers and institutions thanks to the growing importance of technology integration in business. For Apple to keep up with its competition, the company needs to release new goods more frequently. Apple's brand image and financial performance are negatively impacted by Apple's competitors' low-cost offerings of high-value technical products. Samsung, for example, has maintained its position in the PC market, whereas Apple has lost it. Competition from low-cost, high-tech rivals has contributed to this situation. Apple now has a big chance to take advantage of the growing demand for cloud computing services by establishing an extended cloud framework. The technological environment is likely to impact the future steps taken by the company because presently, this field is filled with numerous players who are all gearing towards competing with apple. With the new emerging trends in technology, the company is highly obligated to have working mechanisms that protect them from any threat from external sources such as competitors.

The economic environment impacts the working mechanisms of apple corporation in numerous significant ways. With the set-up of the modern global market dynamics, apple's success as a company relies on the sales made. For sales to be made, there must be markets that are dependent on good economies. According to MBA school Team (2021), Apple Corporation has numerous expansion opportunities. For instance, economic stability in industrialized countries, rapid economic growth in developing countries, and disposable income among target consumers. However, it is important to keep in mind all the competing factors in the worldwide marketplaces when investigating economic opportunities. In the context of major international corporations like Samsung and Huawei, these external strategic drivers represent growth opportunities for the company and its competitors.

Five forces of competition, also known as the Porter five forces analysis, are those elements that determine the success of a corporation through a comprehensive analysis of t ...

Similar to Writing Sample - Equity Research - AAPL (20)

12 External and Internal Environments Mikia DixonBusiness

Writing Sample - Equity Research - AAPL

1. Student Investment Management Report

Company Description

Apple Inc. (Apple) designs and markets consumer electronic devices,

including personal computers, mobile phones, tablets, portable

digital music players. The company also provides its own operating

systems on each products and allows customers to purchase and

storage a variety of accessories, services and digital contents through

its iCloud and iTunes stores. Apple is the pioneer in information

technology sector which re-defined several industries through its

Mac, iPod, iPhone, and iPad.

Investment Thesis

I issue a HOLD recommendation for Apple. My valuation yield a

fair value of $125.66 as of 07/24. I believe the company’s advantage

of current strong product portfolio is offset by the uncertainty of

future product initiative.

- Apple launched its latest version of iPhone – iPhone 6/6+ last

September which generated the highest additional customers in

one quarter. Given only 10-15% of iPhone users have upgraded

to iPhone 6 as of Q2 FY15, I believe there is still more room

for iPhone 6 to grow.

- The company is sitting on $32B cash & equivalent and

possesses $110B net financial asset as of Q2 FY15. It is

planning to pay back $65B of cash through share buyback and

dividend in CY15. This set a buffet for downside potential.

- Currently, I could not see a clear strategy for the long-expected

Apple Watch. There is no certain function or business need that

distinguishes the product from good-to-have to must-have. The

long term growth concern will remain an issue if the company

could not figure out a more sustainable business model.

Risk to Recommendation

- Failure to successfully launch new product will impact top and

bottom line of the company.

- Similar function of different products could lead to self-

cannibalization.

- Strong dollar and weaker economy outlook in major oversea

market can affect the company’s performance.

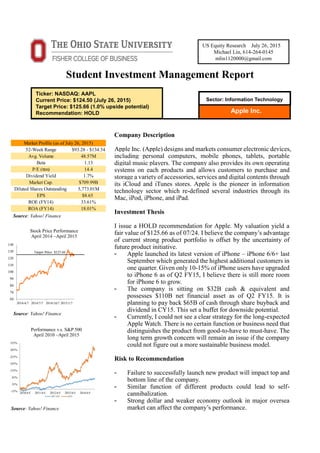

Apple Inc.

US Equity Research July 26, 2015

Michael Lin, 614-264-0145

mlin1120000@gmail.com

Sector: Information Technology

Ticker: NASDAQ: AAPL

Current Price: $124.50 (July 26, 2015)

Target Price: $125.66 (1.0% upside potential)

Recommendation: HOLD

Stock Price Performance

April 2014 –April 2015

Performance v.s. S&P 500

April 2010 –April 2015

Source: Yahoo! Finance

Source: Yahoo! Finance

Source: Yahoo! Finance

52-Week Range $93.28 - $134.54

Avg. Volume 48.57M

Beta 1.13

P/E (ttm) 14.4

Dividend Yield 1.7%

Market Cap. $709.99B

Diluted Shares Outstanding 5,773.01M

EPS $8.65

ROE (FY14) 33.61%

ROA (FY14) 18.01%

Market Profile (as of July 26, 2015)

2. OSU Student Investment Management July 26, 2015

2

Table of Contents

Company Overview…………………………………………………………3

Business Segments………………………………………………………3

Business Model………………………………………………………….4

Industry Overview and Competition Positioning……………………......5

Current Issues…………………………………………………………....7

Business Trend…………………………………………………………..9

Investment Thesis………………………………………………….……....10

Economic Analysis…………………………………………………..…10

Financial Analysis…………………………………………………...…11

Risk…………………………………………………………........................12

Supply Chain Risk………………………………………………….......12

Competition Risk……………………………………………………….12

Currency Risk…………………………………………………………..12

Valuation…………………………………………………………...............12

DCF Valuation………………………………………………………….12

Relative Valuation…………………………………………...…………14

Risk to Target Price…………………………………………………….15

Conclusion…………………………………………………………............15

Appendices…………………………………………………………............16

Works Cited………………..………………………………………............20

3. OSU Student Investment Management July 26, 2015

3

Company Overview

Founded at 1977, the Cupertino, California based consumer electronic

provider is now the largest public company in the world with $710B market

cap at the end of Q3 FY15. The company’s revenue can be broken down

into six regions: Americas: 46.3%, Europe: 28.1%, Greater China: 21.0%,

Japan: 13.7%, Rest of the Asia Pacific: 6.9% and Retail: 8.9% (Figure 1).

Apple designs and markets its product and outsources the manufacturing

process. While most of its peers use Windows and Google’s operation

system and follow the open source strategy, Apple provides its own

operating system and leaves less room for programmers to adjust to its

system. Similarly the company put more control on the hardware; for

instance, instead of using Intel or Qualcomm’s processor, the company

design its own CPU. This strategy leads to better integration between

software and hardware which leads to the company’s 30% installed base

market share in premium smartphone market. Another obvious advantage of

the closed platform strategy is that there are less viruses on Apple’s platform.

Unlike its competitors, Apple operates its own retail stores that accounts for

28% of the company’s revenue. The company’s revenue and net income are

$182.8B and $39.5B in FY14; the growth rates are 7.1% and 6.8%

respectively (Figure 2).

Business Segments

Apple currently reports six product segments – iPhone, iPad, Mac, iPod,

Accessories, and iTunes, Software and Services (Figure 3). The new

products such as Apple Watch and Apple Pay will be discussed in Current

Issues.

iPhone

iPhone is the most important product for Apple which represents 55.8% of

revenue. This segment enjoyed 41.9% CAGR in sales for the past five years.

Thanks to constant upgrade of its product, the ASP remains constant. iPhone

is estimated to have 20% unit sales market share by Q4 CY14. The company

sold 169M units of iPhone in FY14 at an average price of $602 (Figure 5).

Macintosh (Mac)

This segment accounts for 13.2% of revenue. As a more mature product,

Mac segment saw more cyclical revenue growth with 8.3% CAGR for the

past five years. This segment is facing a decreasing ASP trend for the past

decade due to fierce competition and short product life cycle. The company

sold 18.9M units of Mac computer at an average price of $1,273 in FY14.

iPad

Since its debut in CY11, the iPad business had grown rapidly to become the

second largest revenue generator which contributes 16.6% of sales in FY14.

However, iPad’s market share dropped dramatically from 70% to 30%.

Furthermore, after three years of rapid growth, this segment faced a 4% sales

decline in FY14. The pale result of iPad is due to lack of innovation and

increasing competition. In addition, iPad mini could also be negatively

Figure 1: Revenue Breakdown by Region

Figure 3: Revenue Breakdown by Product

Figure 2: Revenue & Net Income/Growth

Figure 4: Tablet v.s. Phablet

Source: Company Data

Source: Company Data

Source: Company Data

Source: IDC, Company Data

4. OSU Student Investment Management July 26, 2015

4

impacted by the large iPhone 6+, which is similar to the mini tablet (Figure

4). In addition, the ASP declined constantly after its appearance. Unless the

company develop new function, iPad will stay as an accessory rather than a

necessity.

2010 2011 2012 2013 2014

ASP iPhone 629.6 636.3 629.3 607.5 602.7

ASP Mac 1279.4 1301.6 1278.8 1314.7 1273.6

ASP iPad 664.8 628.4 530.7 450.2 445.5

Services

Due to the well-established ecosystem the company built and the

comprehensive compliment application, Apple has a 13.1% sales from

services, which cannot be seen in other handset providers. The revenue of

this segment come from sales on iTunes, commission from application

developers and most recently, the fee from Apple Pay.

iPod

The portable digital music device Apple created was once a disruptive

innovation that, along with the iTunes platform, has shaken the music

industry. However, iPhone is now replacing iPod in every aspect; therefore,

this segment only contribute 1.3% of sales and experienced 48% and 21%

sales decline for FY14 and FY13. The company sold 14M units of iPod at

an average price of $159 during FY14.

Business Model

Apple achieves today’s success through constant innovation. However, the

fact that it needs to continuously bring in groundbreaking products also

shows the company’s dependent on unpredictable innovation to maintain

current size. For the growing segment such as iPhone, this drawback has not

affected current performance since the company only needs to upgrade and

add in more features to sell the product at a higher price. However, the short

product life cycle is hurting the mature businesses such as Mac and even

iPad. The company saw constant price drop and decline in units sold even

when it upgraded those products every year (Figure 6 & 8). This very

phenomenon is also due to pricing strategy, the premium consumer

electronic device providers usually set higher price on the debut of new

products to attract heavy users, lower the price when the product has become

less trendy, phase out the products when they cannot meet the new functions

that other products serve. Therefore, the assumption that the revenue or free

cash flow can grow in line with the economy is not suitable for this industry.

Figure 5: Product ASP (M)

Figure 6: Mac ASP

Source: Company Data

Source: Company Data

5. OSU Student Investment Management July 26, 2015

5

Although facing harsh environment, Apple is the best among its peers to

widen the moat. The self-built operating system not only differentiates itself

from its peers by delivering first class user experience but also increases the

switching cost and network externality. Users are inclined to stick with the

same operating system which they are familiar with to save time.

Furthermore, consumers are likely to choose the platform with more

applications. Currently, there are 1.2M applications for iOS and 1.3M for

Android. In contrast, there are only 0.3M application for the third largest

Window operating system’s users to download (Figure 7). Without many

popular applications in other operating systems, the current duopoly

situation in mobile OS is very likely to stay intact. Apple Watch is another

way to increase the network effect among devices; moreover, services such

as Apple Pay also aim at increasing customers’ stickiness through

memorizing users’ personal information.

Unlike many other mega-size corporations, Apple achieves today’s scale

through organic growth and in-house development of most of its important

products. The company has seldom acquired other companies to seek

growth. Figure 9 lists all the acquisitions larger than $100M Apple made

since 1997. The only large acquisition the company made is the $3B deal to

purchase Beats Audio to enhance Apple’s audio quality.

Industry Overview and Competitive Positioning

Personal Computer

An ally among Microsoft, Intel and their downstream customers such as HP,

Dell, Asus is the primary competitor of Apple in the personal computer

industry. The user base of Apple’s OS is still significantly lower than that of

the Window’s system – as of February 2014 the OS X market share is a mere

7.69% compare to Windows’ 90.62% (Figure 10); however, the ASP for

Mac is twice as much as that of its competitors. Mac has grown faster than

its peers and has reached its highest market share record of 13.4% in Q3

FY14 in the U.S. market.

Date Company

Price

(Millions)

Apple

Product

28-May-14

Beats Music &

Beats Electronics

$3,000 iTunes

2-Dec-13 Topsy $200

22-Nov-13 PrimeSense $345

26-Jul-12 AuthenTec $356 Touch ID

20-Dec-11 Anobit $500

14-Apr-10 Siri Inc $200 Siri

27-Apr-10 Intrinisty $121 A5

5-Jan-10 Quattro $275 iAds

7-Jul-08 PA Semi $270 A4, A5

2-Sep-97

Power Computing

Company

$110

7-Feb-97 NeXT $404 OS X

Figure 7: No. of App on each OS

Figure 9: Acquisition Larger than $100M

Figure 8: iPad Units Sold and ASP

Figure 10: PC OS Market Share

Source: Statisita

Source: Company Data, Wells Fargo Security

Source: Company Data

Source: Ars Technica

6. OSU Student Investment Management July 26, 2015

6

Smartphone

The competition landscape is similar for the smartphone business. Google

and Qualcomm provide the operating system and chips for Apple’s

competitors such as Samsung, HTC and LG, etc. Apple loses its ground in

terms of OS user base market share to Android for the past three years,

which has grown from 50% to 80%. However, Apple maintains a significant

higher ASP than it peers, which is around $600 compared to $300.

Samsung is the only significant threat of Apple in high end smartphone

business. Those two companies together have captured more than 93%

market share of high end (price > $500) smartphone market (Figure 13). The

high end market is growing faster than the low end market (Figure 15).

Those two companies have filed over 40 patent lawsuits against each other

in many major countries for the past 4 years. However, they dropped patent

disputes outside of the U.S. as of last August. The fact that Samsung

produces and sometimes controls the market of several key components

such as CPU manufacturing, memory chips, LCD panel, and AMOLED

panel, makes the Korean conglomerate a real threat of Apple. Apple and

Samsung are the only two companies that can turn sales into profit – Apple

dominates 81% of operating income of the whole smartphone industry while

Samsung takes the rest.

iPad

As the pioneer of tablet business, Apple once dominated this market;

however, without meaningful ways to bundle iPad with iPhone or Mac

together through exclusive function and low switching cost, the tablet

market has gradually become fragmented with many players fighting for the

market. Samsung is again the chief competitor in this field with other

traditional PC players such as Asus, Lenovo, and Hewlett Packard trying to

gain market share (Figure 14). However, the overall tablet market did not

see growth during CY14; moreover, with the market leader Apple setting its

iPad’s price in the range between $400 to $600, which is even lower than

that of its iPhone, this line of business is not lucrative for most players.

Figure 11: Mobile OS Market Share

Figure 12: Smartphone ASP

Figure 13: High End Phone Market Share

(>$500)

Figure 14: Tablet Market Share

Figure 15: Smartphone Growth Rate

Source: IDC

Source: BMO Capital Market, Company Data

Source: IDC, Credit Suisse

Source: Gartner, UBS

Source: IDC, Credit Suisse

7. OSU Student Investment Management July 26, 2015

7

Current Issues

Apple Pay

Apple announced its plan to penetrate into payment industry by providing

Apple Pay service through its iPhone 6/6+, Apple Watch-compatible devices

(iPhone 5 and later models), iPad Air 2, and iPad Mini 3. This service

enables users to make payment in both retail stores and online checkout.

Apple Pay adopts the near field communication (NFC) technology.

Different from Apple’s previous strategy of vertical integration and

unwillingness to collaborate, Apple Pay will join force with Visa's PayWave,

MasterCard's PayPass, and American Express's ExpressPay system. The

service was exclusive to the United States market initially with international

expansion plan in the future. Apple has entered into Canada in March 2015.

There was an estimated amount of 220,000 vendors participating in Apple

Pay at the service’s debut. Macy’s, Bloomingdale, Walgreen, Subway,

McDonald’s, Uber, Groupon, Panera Bread, Target, and Wholefoods are the

initial vendors to team up with Apple while Walmart and Best Buy stated

they will not accept Apple Pay. The need to upgrade the Point of Sale (POS

system) in order to accept Apple Pay and the fact that there are many

alternative ways of payment might lower some vendors’ interest to join.

Unlike the traditional credit card transaction, Apple Pay does not require

users to transfer personal information; instead, Apple borrowed Bitcoin’s

idea of creating a single-used token and transfer the token to finish the

transaction. The information of the token (or dynamic security code) will

stay between the customers, banks and the vendors, Apple stated that they

would not track the usage to gather customers’purchase habits. This method

is said to be safer than the tradition credit card.

Apple Watch

Apple Watch is the smart watch created by Apple, and announced by CEO

Tim Cook in September 2014. The main features that have been revealed

are health monitoring and fitness tracking. The smart watch is integrated

with iOS and other Apple’s services and products. Customers can perform

services such as Apple Pay, receiving phone call, sending iMessages and

SMS texts, map services and run third-party applications. Siri, the personal

assistant is also embedded on Apple Watch.

However, Apple Watch also depends on iPhone to conduct significant

functions. For instance, the Watch needs to pair up with iPhone to play the

music.

The screen of the watch is a pressure-sensitive touch screen that can detect

the difference between a tap and a press; only two buttons are designed on

the Watch. According to CEO Tim Cook, the Watch will be shower proof to

prevent water damage but water submersion is not recommended. All

versions of Apple Watch have 8GB of storage to store up to 2GB of music

and 75MB of photos. The device is also Wi-Fi and Bluetooth 4.0 connectible.

8. OSU Student Investment Management July 26, 2015

8

There are three collections for Apple Watch – Apple Watch Sport ($349 and

$399), Apple Watch ($549 and $1,049), and the 18-karat gold version Apple

Watch Edition ($10,000 and $17,000), each of them has two sizes (38mm

and 42mm) and two colors. Each collection has three to six bands for

customers to choose. The main problem for this product is the short battery

life, which is estimated to last for only 18 hours due to it needs to constantly

connect to iPhone and leading to battery drainage. Apple Watch is available

for sales online on April 24 in nine markets, including the United States,

Australia, Canada, China, France, Germany, Hong Kong, Japan and the

United Kingdom. This product is an indication to see whether the current

management team can take on revolution rather than evolution after the long

gone of its charismatic founder.

Several competitors, such as HTC, LG, Pebble and Huawei have also been

working on the smart watch product to compete with Apple (Appendix 1).

Without revolutionary functions (or even functions that could not be found

on iPhones), the future of the Watch is far from promising. Apple did not

disclose the shipment information during the latest earning release but since

CEO Tim Cook mentioned more than 100% of the growth in “Other”

segment is contributed by Apple Watch during Q3 FY15, we can estimate

the revenue from Apple Watch is somewhere above $900 million.

Apple TV

Apple TV is the unsuccessful product Apple has spent several years working

on. The first release of Apple TV was back in 2007; the company continued

on developing this product and launched the latest TV – Apple TV Rev A in

January 2013; the company attempted to connect consumers’ TVs and

enables them to access iTunes content for Streaming video and all online

services that was accessible on personal computers, such as Netflix,

YouTube, Flickr, Disney Channel, Hulu, HBO GO and WatchESPN.

However, the idea to revolutionize the TV industry as a cornerstone of the

company’s Internet of Things has not yet been realized.

Apple Auto

“Apple is said to have hired hundreds of engineers specializing in Human

Machine Interface, EV batteries and autonomous driving” from major auto

producers “including former head of Mercedes Benz’s R&D division”

(Financial Times, 14, Feb). Although this news has not been confirmed by

the company, it is reasonable for the largest public company to seek growth

in the $1.6 trillion automobile market, which dwarfs the smartphone

industry at $400B and PC industry at $266B. Without legitimate information,

this part of information is not included in the valuation; however, it is

important to note that Apple’s ability to continue innovation is the key to

future success.

9. OSU Student Investment Management July 26, 2015

9

Business Trend

Bring Your Own Devices (BYOD)

The rapid growth of cloud computing and the transformation to more

intellectual and information based working environment have made BYOD

possible. With the increase of cross devices interaction and more

personalized devices and software, employees are more inclined to use their

own devices. A survey done by Mckinsey shows that 44% of job seekers

view an organization more positively if it allows them to bring their own

device. According to industry estimates, the global market for BYOD

created $72B in revenue in 2013. This market is expected to have a 26%

CAGR during 2013 to 2019, which implies a $284B by 2019 (Figure 16).

This on-going trend is beneficial to Apple since the company has low

penetration rate in the corporate market, especially when massive purchases

from big corporation will probably hurt Apple’s high margins. The

popularity and the ecosystem of Apple’s products in consumers area is likely

to spill over into business world if the BYOD remains robust. Furthermore,

if the BYOD becomes a phenomenon, learning Windows system and related

products may no longer be required skills. This can lower PC’s network

effect that prevents Apple from getting more market share. To enhance its

corporate footprint, the company announced an exclusive partnership with

IBM to take advantage of IBM’s big data and analytics capabilities to

implement to iPhone and iPad.

Figure 16: BYOD Market Size and Growth

Rate

Source: Marketandmarket.com

10. OSU Student Investment Management July 26, 2015

10

Investment Thesis

Economy Analysis

Apple’s premium products are considered more luxurious than that of its

peers. As a result, Apple’s performance should be highly cyclical and

depends on the well-being of consumers.

The Consumer Confident Index (CCI) is the indicator to see how likely the

consumers are going to spend more in the future. Figure 18 shows the CCI

has raised dramatically from 20 to 90 from CY08 to CY14. This is a positive

sign for Apple since consumer are now more willing to pay for superior

products.

Another indicator is the U.S. unemployment rate, which has dropped from

10% to 5.5% from CY09 to CY14 (Figure 19). Since 46% of Apple’s

revenue are generated from the Americas, the improvement of the job

market in the United States will have positive impact on Apple’s customer

base. The macro economic factors send positive signal which provide a

tailwind for Apple.

Nevertheless, since Apple is still in its growth stage (for its main product

and future products), and involved in an ever-changing industry, the

innovation is still the single most important driver of growth. For instance,

during the financial crisis in CY08, Apple still grew its revenue thanks to

the launch of its iPhone. R&D is a barometer to see the company’s

willingness to innovate. Figure 17 shows the company has increased its

R&D over revenue from 1.5% to 2.6% from FY12 to FY14. It’s a signal that

even after giving back shareholders tremendous amount of cash, the

company still invested a lot on innovation.

Figure 17: R&D/Revenue

Figure 18: Consumer Confidence Index Figure 19: U.S. Unemployment Rate

Source: Company Data

Source: Conference Board Source: Conference Board

11. OSU Student Investment Management July 26, 2015

11

Financial Analysis

Superior Gross Margin

Apple created significantly higher gross margin through its popular products.

The company’s average gross margin of 40% is twice as high as that of

competitors’ average of 23% (Figure 20). There is also a trend that the

company earn a slightly lower margin on an “s” year, which the company

only upgrades the previous product and has less new product launches

(iPhone 4S, 5C).

Du Pont Analysis

The company keeps a trailing twelve months ROE of 33.61%, compared to

peers’ 11.64%. The astonishing return to equity could be contributed to its

six-time-higher-than-average net income margin, which is at 21.61%. On

the other hand, the company’s leverage remains low – the asset over equity

ratio is a healthy 2.078 times whereas its peers have an average of 3.06 times.

Increasing Leverage and Cash Payback

Through its premium products and rapid sales growth, the company now

possesses $32B of cash and equivalent and $110B of net financial assets by

the end of Q2 FY15. On top of that, as current management took over, the

company has been more willing to increase its leverage and payback the

cash to shareholders. As Figure 22 shows, the company has increased its

debt over asset ratio from 36.4% to 51.9% during the past five years. Apple

is planning to sell another $6.5B corporate bond for FY15. The company

has already paid back $33B and $56B to shareholders in CY13 and CY14

and has started paying dividend since FY12. In April 2014, the management

team decided to increase the company’s cash return program. The company

expects to return over $130B of its cash by the end of CY15 under the

expanded program, with $40B in dividend and $90B in share repurchases.

The company started payback shareholder since CY12. Figure 23 shows

Apple is returning 73% and 112% of its free cash flow to shareholders

mainly through share buyback in CY13 and CY14.

One concern for Apple’s ability to payback shareholders is the repatriation

taxes, which is 30% by now. Since only 11% of the company’s cash are in

the United States, the company will face the huge tax bill if they send the

money back.

AAPL Peers

ROE 35.34% 11.64%

ROA 18.01% 4.11%

Asset/Equity 2.078 3.06

Turnover 0.788 1.45

NI Margin 21.61% 3.41%

Figure 20: Gross Margin Comparison

Figure 21: Du Pont Analysis

Figure 22: Debt/Asset Ratio

Figure 23: Cash Distribution

Source: Bloomberg

Source: Bloomberg

Source: Capital IQ

($ in millions) 2011 2012 2013 2014 2015 2016E

Net Income $25,922 $41,733 $37,037 $39,510 $49,064 $52,149

FCF $33,269 $42,561 $45,501 $50,142 $66,567 $72,999

FCF% of NI 128% 102% 123% 127% 136% 140%

Buybacks $0 $0 $22,860 $45,000 $49,925 $54,749

% FCF for Buybacks 0% 0% 50% 90% 75% 75%

Dividends $0 $2,488 $10,564 $11,126 $16,642 $18,250

% FCF for Dividends 0% 6% 23% 22% 25% 25%

Total FCF Returned $0 $2,488 $33,424 $56,126 $66,567 $72,999

% of Total FCF Returned 0% 6% 73% 112% 100% 100%

Source: RBC Capital Market and Company Data

12. OSU Student Investment Management July 26, 2015

12

Risk

Supply Chain Risk

Apple outsources most of its components and manufacturing process to third

party Asian suppliers. For instance, four Taiwanese companies namely Hon

Hai Precision, Pegaton, Compal and Quanta together assemble most of

Apple’s products. For the company’s state-of-art CPU, only Taiwan

Semiconductor Manufacturing Corporation and Samsung Electronic are

capable of producing the cutting-edge chips. The high definition camera lens

is largely provided by Largen, yet another Taiwanese company. The flash

and other memory chips are mainly from its main competitors Samsung. The

concentration on few providers in same region and the reliance on certain

competitor to provide key components can lead to supply chain risk if any

political or economic uncertainty were to happen.

Competition Risk

Apple faces fierce competition in each product segment. The premium price

the company charges position itself in a riskier situation if an economy

downturn were to happen. The closed platform strategy also puts more risk

on Apple. For instance, if Google stops providing all the services such as

Google map, YouTube, Chrome and its search engine, Apple’s user might

find difficulties in sticking with Apple without those services.

Currency Risk

The on-going strong dollar could be a potential threat to Apple. As EU and

BoJ planning to launch massive quantitative easing, and People’s Bank of

China lowered its prime rate and is also likely to start a quantitative easing

program, the U.S. dollar becomes the strongest currency in the world.

Moreover, Fed’s intention to raise the interest rate almost promises a further

appreciation of dollar. Under this premise, Apple’s oversea revenue, which

is more than 60% of its total revenue could be hurt badly. Although Apple

is involved in currency forward to hedge the currency risk, it is hard for the

company to hedge the risk if the dollar appreciate significantly and stay at

the relatively high level for a long period of time.

Valuation

DCF Model

Although the future cash flow for Apple is more difficult to capture, the DCF

model is still the best and theoretically correct model to forecast the

company’s value. I use a five year forecast period due to the fast-changing

nature of Apple’s business and difficulty to quantify innovation that has not

taken place. Each business segment’s revenue are forecasted separately. The

followings are the assumptions behind the model.

Revenue

Mac: The CAGR of this segment is 8.3% for the past five years, given that

personal computer is a more mature market and competitors keep competing

on price and features, I give this segment a 6% revenue growth for the

13. OSU Student Investment Management July 26, 2015

13

following three years and 4% for the other two.

iPad: Without significant breakthrough in developing new function, the

market size for tablet is relatively limited. The sales for iPad grew at a mere

3% in FY13 and encountered a decline of 5% in FY14. Furthermore, the

larger phone is likely to be the mainstream in the future. This might sabotage

iPad mini’s sells, which accounts for 41% of total iPad sales. Thus, I give a

sharp decline for the forecast period for this segment.

iPhone: iPhone will still be the main driver of Apple’s growth in the

foreseeable future. Based on the company’s past record to publish a new

phone every two years, and launch similar but upgraded version in between

(such as iPhone 4S and iPhone 5C), there is an obvious 2 to 2.5 year cycle.

Moreover, by adding more feature (larger screen), Apple raised its selling

price significantly and received best sales record in respond. However, I

expect its pricing power will deteriorate as the market mature. I forecast the

revenue growth will be 50%, 6%, 15% 6% and 8% for FY15 to FY19. The

huge increase in FY15 is justifiable since Apple sold 76M iPhone 6 during

Q2 FY15 yet only 10% to 15% of iPhone installed base had upgraded to

iPhone 6.Not to mention the company announced the highest additional user

in Q2 FY15. The iPhone 6/6+ is expected to have extremely high penetration

in the growing Asian market where larger screen is popular among

customers. The increase in shipment and price are both factored in to reach

the revenue growth numbers.

Apple Watch: Since the Watch has to pair with iPhone for significant

functionality, I use iPhone installed base (past two years’ shipment unit) to

estimate the Apple Watch’s unit sales. The all-in cost I used for this product

is $450, which is higher than the retail price of $350 since users will need

two wrist straps to work with the watch, which will cost $100 extra. Without

too many wow-factors from the previous product announcement, and the

idea that this product can hardly be a necessity like mobile phones, I use

only 1%, 2%, 3%, 2%, and 2% of iPhone’s forecast installment as Apple

Watch’s penetration into iPhone installed base for the forecast period.

Apple Pay: This segment plays a role to increase customers’ reliance and

would not be a major revenue driver in the near future. However, it could be

a more stable stream of revenue with extremely high margin business for

Apple. Apple charges a 15bps per transaction for interchange fee from banks.

The plastic card transaction volume (including both debit and credit card) is

estimated to be 200B and will grow to 240B by CY18. According to Cowen

and Company’s survey, over 35% of iPhone 6/6+ owners used Apple Pay

service, and among them, 65% use it several times a week. Based on the

positive number, I use a 2% increase of non-cash transaction market share

each year for Apple Pay for the forecast period (exclude online payment

system), starts from a 2% at CY15. After CY19, I assume Apple will change

to a percentage fee of 0.3% commission for each transaction and have a

stable 10% market share of the non-cash transaction.

Services: The services sector includes all the revenue from application,

software and other service excluding the payment service (in my model). As

14. OSU Student Investment Management July 26, 2015

14

a healthier stream of revenue, this segment grew by 13% and 25% for FY14

and FY13. An 8% revenue growth is expected for the following five years.

Others: This segment includes iPod and other accessories. Due to the sharp

decline of iPod’s sales has already taken place – a 48% and 25% decrease

for FY14 and FY13, this segment is forecasted to decline by 2% each year

for the forecast period.

Operating Margin

Apple has the highest customer loyalty in the industry, thus the company’s

ability to maintain margins is better than most competitors. Furthermore, the

increasing revenue from high margin segment such as Apple App store and

Apple Pay can offset the declining ASP for iPad segment. Therefore, I

estimate the company will have operating margin around 28% to 29.5%, and

maintain a 29.5% operating margin which is slightly lower than the past five

years average of 30.7%, at the end of forecast period.

Terminal Growth

As mentioned earlier, the consumer electronic products tend to have short

product life cycle and thus face price decrease; therefore the terminal growth

of these companies should be lower than average. As a result, I choose a 2%

terminal growth rate of free cash flow after the forecast period.

Net Financial Asset

Unlike most other firms which have to borrow money to sustain their

operation, Apple possessed an astonishing $110B net financial asset as of

Q2 FY15. The company can keep running without most of those financial

assets; furthermore, the management team is willing to pay back the excess

cash to shareholders. Therefore, I take $100B of net financial asset into

consideration and reduce the interest income the company will have going

forward.

Discount Rate

The industry Apple is involved in has less durable competitive advantage

and the players face rapid change constantly, which leads to higher business

risk. Companies such as, Nokia, Motorola, Sony and even Apple itself, have

once dominated the market but failed nevertheless; therefore, I believe the

discount rate for most companies in this industry should be higher than

average. Therefore, I use an 11.0% discount rate for Apple.