Recommended

More Related Content

Similar to William blair report on dvax

Similar to William blair report on dvax (20)

Recently uploaded

Recently uploaded (14)

William blair report on dvax

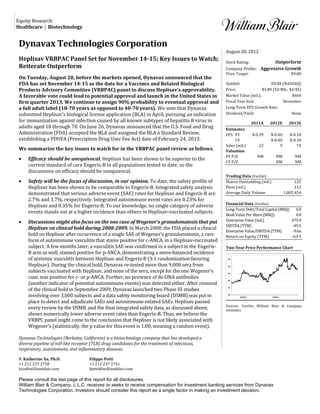

- 1. Equity Research Healthcare | Biotechnology Dynavax Technologies Corporation August 28, 2012 Heplisav VRBPAC Panel Set for November 14-15; Key Issues to Watch; Stock Rating: Outperform Reiterate Outperform Company Profile: Aggressive Growth Price Target: $9.00 On Tuesday, August 28, before the markets opened, Dynavax announced that the FDA has set November 14-15 as the date for a Vaccines and Related Biological Symbol: DVAX (NASDAQ) Products Advisory Committee (VRBPAC) panel to discuss Heplisav’s approvability. Price: $3.89 (52-Wk.: $2-$5) A favorable vote could lead to potential approval and launch in the United States in Market Value (mil.): $660 first quarter 2013. We continue to assign 90% probability to eventual approval and Fiscal Year End: December a full adult label (18-70 years as opposed to 40-70 years). We note that Dynavax Long-Term EPS Growth Rate: submitted Heplisav’s biological license application (BLA) in April, pursuing an indication Dividend/Yield: None for immunization against infection caused by all known subtypes of hepatitis B virus in 2011A 2012E 2013E adults aged 18 through 70. On June 26, Dynavax announced that the U.S. Food and Drug Estimates Administration (FDA) accepted the BLA and assigned the BLA a Standard Review, EPS FY $-0.39 $-0.40 $-0.18 establishing a PDUFA (Prescription Drug User Fee Act) date of February 24, 2013. CY $-0.40 $-0.18 Sales (mil.) 22 9 74 We summarize the key issues to watch for in the VRBPAC panel review as follows. Valuation FY P/E NM NM NM • Efficacy should be unequivocal. Heplisav has been shown to be superior to the CY P/E NM NM current standard of care Engerix-B in all populations tested to date, so the discussions on efficacy should be unequivocal. Trading Data (FactSet) • Safety will be the focus of discussion, in our opinion. To date, the safety profile of Shares Outstanding (mil.) 125 Heplisav has been shown to be comparable to Engerix-B. Integrated safety analysis Float (mil.) 112 demonstrated that serious adverse event (SAE) rates for Heplisav and Engerix-B are Average Daily Volume 1,805,454 2.7% and 3.7%, respectively. Integrated autoimmune event rates are 0.23% for Financial Data (FactSet) Heplisav and 0.35% for Engerix-B. To our knowledge, no single category of adverse Long-Term Debt/Total Capital (MRQ) 0.0 events stands out at a higher incidence than others in Heplisav-vaccinated subjects. Book Value Per Share (MRQ) 0.8 • Discussions might also focus on the one case of Wegener’s granulomatosis that put Enterprise Value (mil.) 475.9 EBITDA (TTM) -49.5 Heplisav on clinical hold during 2008-2009. In March 2008, the FDA placed a clinical Enterprise Value/EBITDA (TTM) -9.6x hold on Heplisav after occurrence of a single SAE of Wegener’s granulomatosis, a rare Return on Equity (TTM) -63.9 form of autoimmune vasculitis that stains positive for c-ANCA, in a Heplisav-vaccinated subject. A few months later, a vasculitis SAE was confirmed in a subject in the Engerix- Two-Year Price Performance Chart B arm as well, stained positive for p-ANCA, demonstrating a more-balanced incidence of systemic vasculitis between Heplisav and Engerix-B (3:1 randomization favoring $5 Heplisav). During the clinical hold, Dynavax re-tested more than 9,000 sera from $4 subjects vaccinated with Heplisav, and none of the sera, except for the one Wegener’s $3 case, was positive for c- or p-ANCA. Further, no presence of ds-DNA antibodies (another indicator of potential autoimmune events) was detected either. After removal $2 of the clinical hold in September 2009, Dynavax launched two Phase III studies $1 involving over 3,000 subjects and a data safety monitoring board (DSMB) was put in $0 12/31/10 12/30/11 place to detect and adjudicate SAEs and autoimmune-related SAEs. Heplisav passed Sources: FactSet, William Blair & Company every review by the DSMB, and the final integrated safety data, as discussed above, estimates shows numerically lower adverse event rates than Engerix-B. Thus, we believe the VRBPC panel might come to the conclusion that Heplisav is not likely associated with Wegener’s (statistically, the p value for this event is 1.00, meaning a random event). Dynavax Technologies (Berkeley, California) is a biotechnology company that has developed a diverse pipeline of toll-like receptor (TLR) drug candidates for the treatment of infectious, respiratory, autoimmune, and inflammatory diseases. Y. Katherine Xu, Ph.D. Filippo Petti +1 212 237 2758 +1 212 237 2741 kxu@williamblair.com fpetti@williamblair.com Please consult the last page of this report for all disclosures. William Blair & Company, L.L.C. receives or seeks to receive compensation for investment banking services from Dynavax Technologies Corporation. Investors should consider this report as a single factor in making an investment decision.

- 2. William Blair & Company, L.L.C. • The mechanism of the novel adjuvant in Heplisav, a TLR9 agonist, might be discussed as well. Heplisav is the first product containing the novel adjuvant TLR9 agonist that is up for approval. We note that GlaxoSmithKline’s (GSK $45.79) Cervarix was the first vaccine approved in the United States that contained a novel adjuvant (a TLR4 agonist) other than alum. The FDA approved Cervarix for preventing human papillomavirus (HPV) infection in October 2009, two and a half years after the first submission of the BLA and one month after removing the clinical hold on Heplisav. We understand the traditional cautious stance from the FDA on the safety profile of novel vaccine adjuvants, but believe that should the Heplisav package demonstrate a satisfactory safety profile, it is highly likely that the FDA will approve the vaccine, as it did Cervarix. We believe the FDA recognizes the high unmet need in the hyporesponsive populations and desires to have these subjects adequately protected against potential HBV infection. • The extent of the label: for adults over 40 or over 18. After the removal of the clinical hold, the FDA instructed that further studies should be conducted in older adults who are less responsive to the currently licensed vaccines, including adults over 40 years of age, and individuals with chronic kidney disease. In February 2012, the FDA agreed in the pre-BLA meeting that Heplisav’s label could be expanded to include healthy adults between the age of 18 and 70, which is the full adult label. We believe the VRBPAC panel could discuss this topic as well and vote on it. We maintain our Outperform rating and $9 price target. We continue to believe that if approved, Heplisav will become the standard-of-care hepatitis B vaccine in six years after launch; we continue to assume 90% probability for Heplisav to reach the market. We forecast peak sales of $330 million for Heplisav in 2018 for the CKD population and the HIV/HCV/liver disease population, and Dynavax has a commercial organization of 150 people in total for the U.S. market. For the U.S. diabetic opportunity, although Dynavax could cover this market itself, we continue to model a bell-shaped curve peaking at about $475 million in revenue, with 35% royalties (net of COGS) to Dynavax on total U.S. sales from a partner with an established diabetes franchise, to be conservative. With such assumptions, we derive the fair value of the stock at $9 per share. We believe Dynavax shares continue to represent a compelling risk/reward opportunity. Risks to our Outperform thesis include regulatory risks and intellectual property risks associated with Dynavax’s lead candidate Heplisav, as well as risks related to business development and clinical development activities. 2 | Y. Katherine Xu, Ph.D. +1 212 237 2758

- 3. William Blair & Company, L.L.C. William Blair & Company, L.L.C. was a manager or co-manager of a public offering of equity securities for Dynavax Technologies Corporation within the prior 12 months. William Blair & Company, L.L.C. and its affiliates beneficially own or control (either directly or through its managed accounts) 1% or more of the equity securities of Dynavax Technologies Corporation as of the end of the month ending not more than 40 days from the date herein. William Blair & Company, L.L.C. is a market maker in the security of Dynavax Technologies Corporation and may have a long or short position. Additional information is available upon request. Dynavax Technologies Corp. (DVAX) Current Rating: Outperform Aug 27, 2009 - Aug 27, 2012 Previous Close: $3.71 6/2/11 - I-O $5 11/14/11 - O - PT:$8 $4 11/18/11 - PT:$10 $3 5/9/12 - PT:$9 $2 6/15/11 - PT:$8 $1 11/3/11 - R - PT:$8 $0 12/31/09 12/31/10 12/30/11 Source: William Blair & Company, L.L.C. and FactSet Initiation, RI = Reinitiated, @ = Analyst Change PT = Price Target Legend: I = Current Rating Distribution (as of 07/31/12) Coverage Universe Percent Inv. Banking Relationships* Percent Outperform (Buy) 61 Outperform (Buy) 7 Market Perform (Hold) 34 Market Perform (Hold) 2 Underperform (Sell) 1 Underperform (Sell) 0 *Percentage of companies in each rating category that are investment banking clients, defined as companies for which William Blair has received compensation for investment banking services within the past 12 months. Y. Katherine Xu attests that 1) all of the views expressed in this research report accurately reflect his/her personal views about any and all of the securities and companies covered by this report, and 2) no part of his/her compensation was, is, or will be related, directly or indirectly, to the specific recommendations or views expressed by him/her in this report. We seek to update our research as appropriate, but various regulations may prohibit us from doing so. Other than certain periodical industry reports, the majority of reports are published at irregular intervals as deemed appropriate by the analyst. Stock ratings, price targets, and valuation methodologies: William Blair & Company, L.L.C. uses a three-point system to rate stocks. Individual ratings and price targets (where used) reflect the expected performance of the stock relative to the broader market (generally the S&P 500, unless otherwise indicated) over the next 12 months. The assessment of expected performance is a function of near-, intermediate-, and long-term company fundamentals, industry outlook, confidence in earnings estimates, valuation (and our valuation methodology), and other factors. Outperform (O) – stock expected to outperform the broader market over the next 12 months; Market Perform (M) – stock expected to perform approximately in line with the broader market over the next 12 months; Underperform (U) – stock expected to underperform the broader market over the next 12 months; not rated (NR) – the stock is not currently rated. The valuation methodologies used to determine price targets (where used) include (but are not limited to) price-to-earnings multiple (P/E), relative P/E (compared with the relevant market), P/E-to-growth-rate (PEG) ratio, market capitalization/revenue multiple, enterprise value/EBITDA ratio, discounted cash flow, and others. Company Profile: The William Blair research philosophy is focused on quality growth companies. Growth companies by their nature tend to be more volatile than the overall stock market. Company profile is a fundamental assessment, over a longer-term horizon, of the business risk of the company relative to the broader William Blair universe. Factors assessed include: 1) durability and strength of franchise (management strength and track record, market leadership, distinctive capabilities); 2) financial profile (earnings growth rate/consistency, cash flow generation, return on 3 | Y. Katherine Xu, Ph.D. +1 212 237 2758

- 4. William Blair & Company, L.L.C. investment, balance sheet, accounting); 3) other factors such as sector or industry conditions, economic environment, confidence in long-term growth prospects, etc. Established Growth (E) – Fundamental risk is lower relative to the broader William Blair universe; Core Growth (C) – Fundamental risk is approximately in line with the broader William Blair universe; Aggressive Growth (A) – Fundamental risk is higher relative to the broader William Blair universe. The ratings, price targets (where used), valuation methodologies, and company profile assessments reflect the opinion of the individual analyst and are subject to change at any time. The compensation of the research analyst is based on a variety of factors, including performance of his or her stock recommendations; contributions to all of the firm’s departments, including asset management, corporate finance, institutional sales, and retail brokerage; firm profitability; and competitive factors. Our salespeople, traders, and other professionals may provide oral or written market commentary or trading strategies—to our clients and our trading desks—that are contrary to opinions expressed in this research. Our asset management and trading desks may make investment decisions that are inconsistent with recommendations or views expressed in this report. We will from time to time have long or short positions in, act as principal in, and buy or sell the securities referred to in this report. Our research is disseminated primarily electronically, and in some instances in printed form. Electronic research is simultaneously available to all clients. This research is for our clients only. No part of this material may be copied or duplicated in any form by any means or redistributed without the prior written consent of William Blair & Company, L.L.C. THIS IS NOT IN ANY SENSE A SOLICITATION OR OFFER OF THE PURCHASE OR SALE OF SECURITIES. THE FACTUAL STATEMENTS HEREIN HAVE BEEN TAKEN FROM SOURCES WE BELIEVE TO BE RELIABLE, BUT SUCH STATEMENTS ARE MADE WITHOUT ANY REPRESENTATION AS TO ACCURACY OR COMPLETENESS OR OTHERWISE. OPINIONS EXPRESSED ARE OUR OWN UNLESS OTHERWISE STATED. PRICES SHOWN ARE APPROXIMATE. THIS MATERIAL HAS BEEN APPROVED FOR DISTRIBUTION IN THE UNITED KINGDOM BY WILLIAM BLAIR INTERNATIONAL, LIMITED, REGULATED BY THE FINANCIAL SERVICES AUTHORITY (FSA), AND IS DIRECTED ONLY AT, AND IS ONLY MADE AVAILABLE TO, PERSONS FALLING WITHIN COB 3.5 AND 3.6 OF THE FSA HANDBOOK (BEING “ELIGIBLE COUNTERPARTIES” AND “PROFESSIONAL CLIENTS”). THIS DOCUMENT IS NOT TO BE DISTRIBUTED OR PASSED ON TO ANY “RETAIL CLIENTS.” NO PERSONS OTHER THAN PERSONS TO WHOM THIS DOCUMENT IS DIRECTED SHOULD RELY ON IT OR ITS CONTENTS OR USE IT AS THE BASIS TO MAKE AN INVESTMENT DECISION. “William Blair” and “R*Docs” are registered trademarks of William Blair & Company, L.L.C. Copyright 2012, William Blair & Company, L.L.C. 4 | Y. Katherine Xu, Ph.D. +1 212 237 2758